NatWest boss ‘made serious error of judgement’ in discussing Farage bank accounts with BBC reporter

NatWest boss Dame Alison Rose has admitted she made a “serious error of judgement” when she discussed Nigel Farage’s Coutts bank accounts with the BBC business editor Simon Jack.

Last week Dame Alison apologised to the former UKIP leader for the closure of his accounts and ordered an immediate review of the processes followed by its Coutts subsidiary.

The NatWest board has said it retains full confidence in Ms Rose as chief executive of the bank but the events will be taken into account when deciding her remuneration.

The chairman of NatWest, Howard Davies, said there have been “serious consequences” for the bank as a result of the “unsatisfactory” handling of the closure of Mr Farage’s account.

The story first came to light when the BBC reported Mr Farage’s account was closed as he did not meet Coutt’s financial thresholds.

Documents obtained by Mr Farage subsequently showed his political beliefs and connections formed part of the rationale.

The BBC, on Monday, apologised for the report.

Nigel Farage has called on MPs to hold an inquiry into NatWest after one of the group’s banks, Coutts, closed his account.

Dame Alison said she believed it was public knowledge that Mr Farage was a Coutts customer and had been offered a NatWest account, and so confirmed these details to Mr Jack.

She said she repeated the Coutts stance – which Mr Farage had publicised – that the bank saw the account closures as a commercial decision.

“I would like to emphasise that in responding to Mr Jack’s questions I did not reveal any personal financial information about Mr Farage,” she added.

“In response to a general question about eligibility criteria required to bank with Coutts and NatWest I said that guidance on both was publicly available on their websites.

“In doing so, I recognise that I left Mr Jack with the impression that the decision to close Mr Farage’s accounts was solely a commercial one.”

Dame Alison said at the time of her conversation with Mr Jack she had not seen the material behind Coutts decision to close the accounts and was not part of the decision making process to close the accounts.

Instead, she said, Coutts told her in April Mr Farage’s account was being closed for commercial reasons.

“Put simply, I was wrong to respond to any question raised by the BBC about this case.”

The NatWest board believed it is “clearly in the interest of all the bank’s shareholders and customers” that Dame Alison continues in the role.

“She has proved, over the last 4 years to be an outstanding leader of the institution, as demonstrated by our results,” Mr Davies said.

Findings of the NatWest review into the closing of Mr Farage’s accounts will be made public and the terms of reference will be announced shortly, the NatWest announcement said.

The banking regulator said it had raised concerns with the NatWest group about the breach of customer confidentiality.

“We made clear our expectation that these issues should be independently reviewed and note today’s statement from the NatWest group board confirming this will happen,” the Financial Conduct Authority said.

“It is vital that the review is well resourced and those conducting it have access to all the necessary information and people in order to investigate what happened swiftly and fully.”

The jobs market continued to slow, with 9,000 fewer vacancies in the three months to September, official figures show.

It is the 39th consecutive period where vacancy numbers have dropped.

Having fewer job openings can mean it is harder to find work.

Money blog: Big retirement age surprise awaits 14% of Britons

There was also a surprise increase in the unemployment rate, up to 4.8% from 4.7% a month earlier, primarily driven by younger people, as a record number of people over 65 are in work, the Office for National Statistics (ONS) said.

Economists polled by Reuters anticipated no change in the jobless rate, but instead the figure is now the highest since the three months to May 2021, when the country was in lockdown due to the COVID-19 pandemic.

The ONS, however, has advised caution when interpreting changes in the monthly unemployment rate and job vacancy numbers due to concerns over the reliability of the figures.

The labour market has struggled in recent months as the cost of employing staff became more expensive due to higher employers’ national insurance contributions and an increased minimum wage.

Wage rises slowing

Further signs of a slowing labour market were seen in the fall of annual private sector wage growth to the lowest rate in nearly four years – 4.4%.

Public sector pay growth increased more quickly, at 6%, as some public sector pay rises were awarded earlier than they were last year.

Inflation up: the bad and ‘good’ news

Average weekly earnings rose more than expected by economists at 5% and also more than previously thought after a revision to last month’s figures (4.8%).

Also published by the ONS was data on industrial action, which showed August had the fewest working days lost to strike action in a single month for nearly six years.

What does it mean for interest rates?

While a tough job market is difficult for people looking for work, the slowing wage rises can mean interest rates are brought down.

Read more:

Got AirPods? There’s more to them than meets the eye and it may mean global trade war

Thousands of homes now need repairs after insulation fitted under government scheme

The rate-setters at the Bank of England had been concerned about the effect higher wages could have on inflation, which it is mandated to bring to 2% though latest figures showed it was at 3.8%.

Following today’s figures, traders expect a cut in the interest rate to 4.75% in December.

No change is anticipated at the next interest rate setter meeting in November.

Business

Got a pair of these? There’s more to them than meets the eye – and it may mean global trade war

For most of human history, no one paid all that much attention to the 17 rare earth elements.

An obscure suite of elements that sit in their own corner of the periodic table, they were mostly renowned among chemists and geologists for being tricky and fiddly – incredibly hard to refine, but with chemical facets that made them, well… interesting.

Not so much for a single thing they did by themselves, but for what they did in conjunction with other elements.

Added to alloys, rare earths can make them stronger, more ductile, more heat-resistant, and so on. Think of them as a sort of metallic condiment: a seasoning you add to other substances to make them stronger, harder, better.

A worker prepares to pour the rare earth metal Lanthanum into a mould in a workshop in Inner Mongolia. File pic: Reuters

The best example is probably neodymium. On its own, there’s nothing especially spectacular about this rare earth element. But add it to iron and boron, and you end up with the strongest magnets in the world. Neodymium iron boron magnets are everywhere.

If you have a pair of headphones or earbuds, the speakers inside them (“drivers” is the technical term) are driven by these rare earth magnets.

If you have a pair of Apple AirPods, those magnets aren’t just in the speakers; they’re what’s responsible for the satisfying “click” when the case snaps shut.

One of the many everyday products that rely on rare earth minerals. Pic: Reuters

Rare earth magnets are in your car: in the little motors that raise and lower the windows, inside the functioning of the airbag and the seat adjustment mechanism.

And not just the little things. Most electric vehicles use rare-earth magnets in their motors, enabling them to accelerate more efficiently than the old all-copper ones.

Pic: iStock

More sensitively, from the perspective of Western governments, in the military, there are tonnes of rare earths to be found in submarines, in fighter jets, in tanks and frigates. Much of this is in the form of magnets, but some is in the form of specialised alloys.

So, for instance, there is no making a modern jet engine without yttrium and zirconium, which, together, help those metallic fan blades withstand the extraordinary temperatures inside the engine. Without rare earths, the blades would simply melt.

Miners are seen at the Bayan Obo mine containing rare earth minerals, in Inner Mongolia, China. File pic: Reuters

Yet the amount of this stuff we mine from the ground each year is surprisingly small.

According to Rob West of Thunder Said Energy, the total size of the rare earth market is roughly the same as the North American avocado market. But, says West, those numbers underplay its profound importance.

“Buyers would likely pay over 10-100x more for small but essential quantities of rare earths, if supplies were ever disrupted,” he says.

“You cannot make long-distance fibre cables without erbium. You cannot make a gas turbine or jet engine without yttrium.”

China’s dominance

In short, these things matter. And that brings us to the politics.

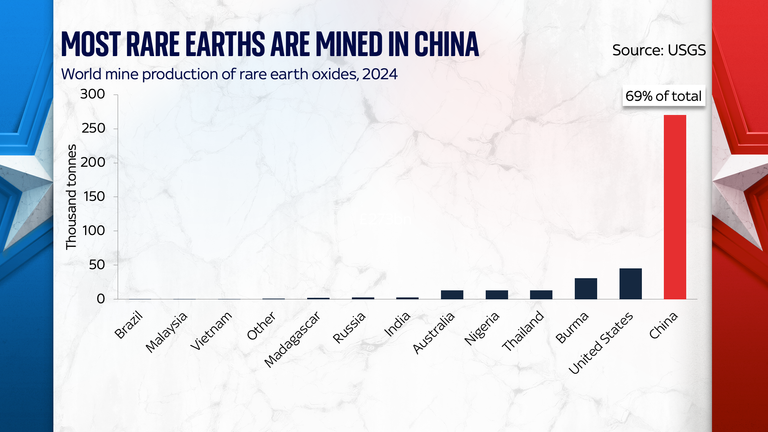

Right now, about 70% of the world’s rare earth elements are mined in China.

Roughly 90% of the finished products (in other words, those magnets) are made in China. China is dominant in this field in an extraordinary way.

This is not, it’s worth saying, for geological reasons.

Contrary to what the name suggests, rare earth elements aren’t all that rare. Pull a chunk of soil out of the ground and there will be trace amounts of most of them in there.

True: finding concentrated ores is a bit harder, but even here, it’s not as if they are all in China.

There are plenty of rich rare earth ores in Brazil, India, Australia, and even the US (indeed, the Mountain Pass mine in California is where rare earth mining really began in earnest).

Low cost of Chinese rare earths

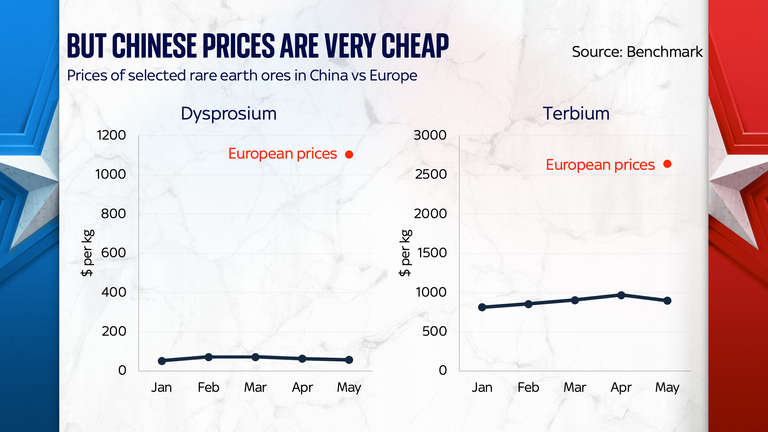

The main explanation for Chinese dominance is that China has simply become very good at extracting lots of rare earths at relatively low cost.

According to figures from Benchmark Mineral Intelligence, the prevailing cost of Chinese rare earths is at least three times lower than the cost of similar minerals refined in Europe (to the extent that such things are available).

At this point, perhaps you’re wondering how China has managed to do it – to dominate global production at such low prices.

Part of the explanation, says West, probably comes down to “transfer pricing” – in other words, China being China, refiners and producers are probably able to buy raw materials at below market prices.

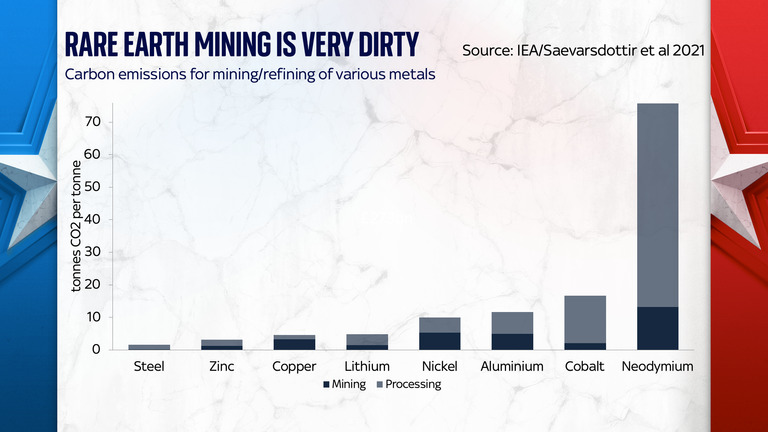

Another part of the explanation is that refining rare earth ores is phenomenally energy and carbon-intensive.

Most European and American firms have pulled out of the sector because it is hideously dirty.

A man works at the site of a rare earth metals mine at Nancheng county, Jiangxi province, China. File pic: Reuters

Such qualms are less of an issue in China, especially since most of their mines, including the biggest of all, Bayan Obo in Inner Mongolia, are hundreds if not thousands of miles from the nearest city.

Energy costs are less of a constraint in a country whose grid is still built mostly on a foundation of cheap thermal coal.

Add it all up, and you end up with the situation we have today: where the vast majority of the world’s rare earths, that go into all our devices, come from dirty mines in China, produced at such a low cost that device manufacturers are happy to put them anywhere.

Anyway, that brings us to the politics.

Global trade war flaring up again

In recent months and years, China has periodically introduced controls on rare earth exports.

Last week, it announced the most serious rule change yet, essentially insisting that anyone using Chinese rare earths would have to apply for a licence from them.

It has been seen, in Washington at least, as a declaration of economic war, and, in response, Donald Trump has announced a fresh set of tariffs on China.

In short, the global trade war seems to be flaring up all over again.

Pic: iStock

Where this ends up is anyone’s guess. Tim Worstall, a former scandium expert who has been in and out of the rare earths sector for decades, suspects China might have overplayed its hand.

“The end result here is that there can be two outcomes,” he says.

“A: The entire world’s usage of rare earths is mapped out in detail, end uses, end users, quantities, and times for the Chinese state and depends upon their bureaucracy to administer.

“B: The plentiful rare earths of elsewhere are dug up, and the supply chain is rebuilt outside China.

“My insistence is that B is going to be the outcome, and it’ll be done, intervention or no.”

Read more from Sky News:

At least 42 dead in bus crash in South Africa

Dozens injured after train crash in Slovenia

In practice, the new rules may simply represent an element in China’s trade negotiations with the US.

So it’s hard to know whether they, or for that matter America’s 100% extra tariffs, will ever really bite.

Either way, it’s yet more evidence of the rocky road the global economy remains on.

Tens of thousands of Vodafone users are reporting problems with their internet

The outages began on Monday afternoon, according to the monitoring website DownDetector, which reported more than 130,000 issues with Vodafone connections.

A spokeswoman for the company said: “We are aware of a major issue on our network currently affecting broadband, 4G and 5G services.

“We appreciate our customers’ patience while we work to resolve this as soon as possible.”

The company has more than 18 million UK customers, with nearly 700,000 of those using Vodafone’s home broadband connection.

Vodafone users vented their frustration on social media.

“It’s like Vodafone has just been wiped off the earth. Not a single thing works,” said one X user.

Vodafone users were shown an error message when trying to access the internet provider’s app

The Vodafone app also appeared to be down for users, with the company’s website briefly going down too.

The ‘network status checker’ on the website was also down, and when Sky News tried to test the customer helpline, it did not ring.

“There’s Vodafone down and then there’s Vodafone wiped off the face of the f***ing planet,” posted another X user.

Read more from Sky News:

Gaza deal latest: Drones reveal devastation

Madagascar president says coup under way

Jake Moore, global cybersecurity advisor at ESET, said the outage shows how reliant we are on modern infrastructure like mobile networks.

“Outages will always naturally raise early suspicions of a potential cyber incident, though current evidence points more towards an internal network failure than a confirmed attack,” said Mr Moore.

“The sudden outage, combined with the inability to access customer service lines, mirrors classic symptoms of a distributed denial-of-service (DDoS) attack, where attackers overwhelm the network so the site or systems collapse.

“However, malicious or not, this once again highlights our heavy reliance on digital infrastructure, especially in an age where we increasingly depend on mobile networks for everything,” he said.

“Ultimately, resilience is essential, whether the cause is a direct cyberattack, a supply chain issue or a critical internal error.”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024