cuts guidance again despite hitting an 'inflection' point in Q2")

Fisker (FSR) cuts guidance again despite hitting an ‘inflection’ point in Q2

California-based Fisker Inc. (FSR) released its second-quarter earnings Friday. Despite improving profitability, Fisker lowered its annual production guidance again due to supplier constraints.

Fisker cuts 2023 EV production guidance

Fisker delivered its first Ocean electric SUV in May as the EV startup began ramping up production.

After producing 55 Ocean SUVs in the first three months of the year, well short of its goal of 300, Fisker said it planned to build between 1,400 and 1,700 vehicles in Q2.

Fisker fell short of its target again despite still producing an impressive 1,022 Ocean EVs in the second quarter. The EV maker said the production miss was due to suppliers having challenges meeting the required components.

For this reason, Fisker lowered its guidance on Friday as it expects to build between 20,000 to 23,000 vehicles this year, compared to 32,000 to 36,000 predicted earlier this year.

The EV maker pointed to a planned Magna Steyr summer shutdown to support the future volume ramp. Fisker says this will give them time to work with suppliers to ensure future component availability. Following the shutdown, Fisker will be able to resume and pick up production where it left off immediately.

Fisker hit a peak production rate of 140 units per day in July, an impressive 75% improvement from the month before. In fact, 1,009 of the 1,022 vehicles produced in Q2 were built in July.

Fisker Q2 financials and updates

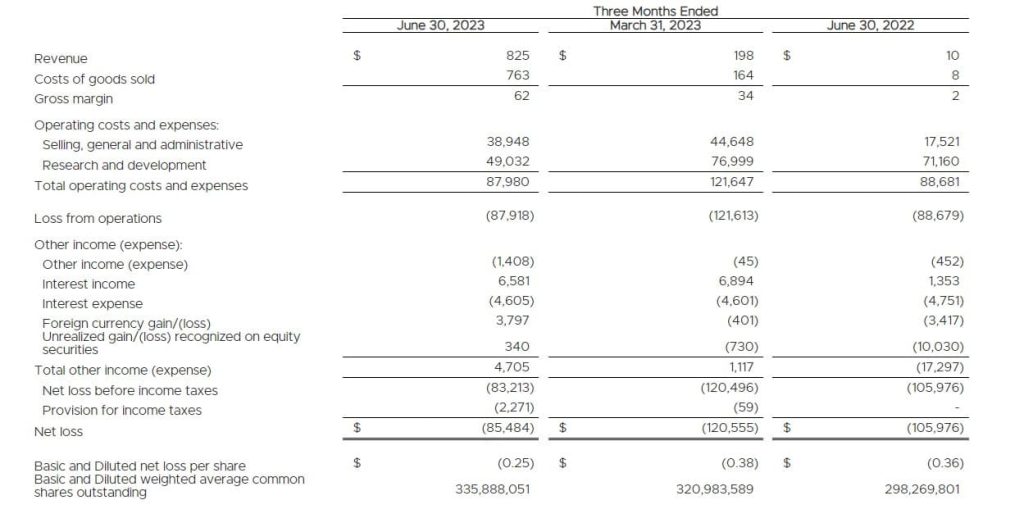

The EV maker generated $825,000 in revenue, up from $198,000 in the first quarter. Fisker highlighted that its first Ocean vehicles delivered achieved a 7.5% gross margin. Excluding early-stage investor vehicles, the gross margin was 18.5%.

Fisker’s operating expenses fell to $88K in Q2 from over $121K in the first three months of the year.

The company’s net loss was $85.5K, or 25 cents per share, compared to 35 cents per share last year, beating Wall St. estimates of around 28 cents per share.

Fisker ended the quarter with $467.5M in cash and equivalents as of June 30, compared to $736.5M at the end of 2022. The company noted it raised an additional $88M through its ATM program during the quarter.

The EV maker held its “Product Vision Day” on Thursday, showcasing several new products, including the new Fisker Ronin, Alaska small EV pickup, and the upcoming $30K Pear small SUV. It also teased the Fisker Ocean with the Force E off-road package.

Fisker believes these products will give it a unique advantage as it moves forward in differentiated segments.

The company also announced on its earnings call it had an agreement drawn up with Tesla to use its NACS connector. It’s just waiting on Tesla to sign.

FTC: We use income earning auto affiliate links. More.

![Maximizing fleet efficiency and ROI with telematics integration [update]](https://i0.wp.com/electrek.co/wp-content/uploads/sites/3/2023/11/Daimler-North-America-semi-electric-trucks.jpg?resize=1200,628&quality=82&strip=all&ssl=1)

Even without clean fleet tax credits and cash-on-the-hood incentives, fleet managers are working hard to maximize their ROI on vehicle assets and reduce their total cost of ownership – and they’re increasingly turning to data‑driven telematics solutions to help.

Telematics use data gathered from sensors embedded in a vehicle to monitor its operations. When collected and interpreted correctly, that data can be used to improve fleet safety, boost operational efficiency, and enable predictive maintenance that reduces (if not eliminates) unexpected downtime. Those are real benefits, with some analysts showing up to 30% savings in repair costs even before you factor in the fuel savings from EVs that, according to MAN CEO Alexander Vlaskamp, will cover the added cost of a BEV in less than three years.

As you can imagine, that’s a big business – and the global market for vehicle telematic platforms is projected to reach an impressive $127 billion in the next decade, and the rush is on to get OEMs like Ford (through Ford Pro) and Volvo (who has a deal with Geotab) to integrate digital solutions into their vehicles.

We originally covered these topics back in February, ahead of the ACT Expo. You can read that original article, below, and let us know what you think of the OEMs’ telematics’

Last month, Geotab signed a deal with Volvo Group to integrate the manufacturer’s vehicle data API into Geotab’s telematics platform. It’s the latest in a recent onslaught of such deals between telematics providers and OEMs that begs the question: what’s in it for the OEMs?

Almost all modern cars and trucks are “connected” in some way. Ford, for example, began fitting the FordPass Connect modem on all its vehicles in the 2020 model year, and the vehicle (and driver) data gathered powers the Ford Pro fleet management platform and enables offerings like the company’s E-Switch Assist, which enables Ford fleet managers to identify which of its ICE-powered F-150 and Transit assets are ready to make the switch to EV.

“Smart tools informed by data like E-Switch Assist are opening up many new conversations with our commercial customers large and small about EV readiness; we’re already using E-Switch Assist regularly in consultations to help organizations determine if electric trucks and vans are right for them,” says Nate McDonald, EV strategy and cross vehicle brand manager at Ford Pro. “The importance of these tools and technologies goes beyond selling a customer a new vehicle—it changes mindsets about whether electric vehicles will work for their business while potentially saving them time and money.”

So, it makes sense for manufacturers to build that connectivity into their vehicles and makes even more sense to use that data connection to populate a fleet management dashboard that makes it painless for fleet managers to monitor their assets within a trusted ecosystem. Think Android vs. iPhone, and the pain that would go into switching from one to the other after a decade or so of constant interaction – because that’s how the OEMs are looking at it.

Why, then, would an OEM open up that data stream to a third party like Geotab?

The answer, presumably, is that that data sharing is a two-way street: the manufacturer’s are opening up their APIs to Geotab, and Geotab is sharing at least some of the data from other manufacturers with their industry partners.

And Geotab has a lot of partners:

- In 2019, Geotab began working with Ford to integrate Ford’s telematics data into its fleet management platform

- In 2020, Geotab began integrating with GM and its OnStar telematics in North American markets

- In 2022, Geotab began partnering with Stellantis’ Free2move car sharing brand, providing full telematics integration into the MyGeotab platform in North America

- In April of 2024, Geotab partnered with Mobilisights to integrate data from Stellantis’ European brands, including Opel, Fiat, Alfa Romeo, Citroën, and Peugeot

- In September of 2024, Geotab announced a new partnership with VW Group Info Services aimed at improving the company’s data integration across its brands

- A deal with Rivian, VW’s partner in a $5 billion joint software venture, followed soon after

All of those players are convinced that the data coming from their vehicles can produce enough value to seriously impact fleet ROI.

Fleet managers seem convinced, too. In a recent McKinsey survey, nearly 57% of EV buyers said they were willing to switch brands in order to get better connectivity features. And, if you’ve ever worked in “a Ford shop” or “a Chevy shop” you already know what a huge that deal that number might be to an OEM.

McKinsey connectivity survey

In that point of view, working with a trusted, universal platform like Geotab who doesn’t have a dog in the vehicle sales fight makes sense. If the Ford Transit the fleet buyer is looking at plays well with their fleet auditing software and systems and the Nissan NV doesn’t – well, it doesn’t really matter if Nissan’s fleetail guy is giving you a better deal at that point. It’s just too painful to operate a second dashboard for one subset of assets.

The man-hours saved with a universal and brand agnostic fleet management platform may not be the easiest to trace all the way to the bottom line, but they’re there.

Additionally, the Geotab dashboard can be configured to collect and even analyze data that’s specifically relevant to EVs. Information like charging history, and regenerative braking efficiency, and overall battery health – data that, over thousands of vehicles, can give fleet managers real insight into how long the new electric vehicles they’re considering will last compared to the gas and diesel vehicles they have experience with.

Geotab research shows that EV batteries could last 20 years or more if they degrade at an average rate of 1.8% per year, as we have observed.

According to our data, the simple answer is that the vast majority of batteries will outlast the usable life of the vehicle and will never need to be replaced. If an average EV battery degrades at 1.8% per year, it will still have over 80% state of health after 12 years, generally beyond the usual life of a fleet vehicle.

Telematics integrations can also help optimize a fleet’s charging schedules, both by scheduling EV charging for lower priced, off-peak hours and by identifying the most dependable high-speed charging stations along regular routes to minimize down time for both vehicles and drivers.

Finally, these data-driven platforms can provide fleet managers tools for tracking and reporting things like carbon emissions and overall energy consumption, which can streamline ESG reporting processes and make it easier for the worker bees to get regulators, administrators, and managers the sort of charts, tables, and graphs they love.

Something like that, anyway.

You can check out my Quick Charge with Nate McDonald, EV strategy and cross vehicle brand manager at Ford Pro, who explores how Ford’s in-house telematics can help fleet managers decarbonize, and head over to Geotab to find out more about their brand agnostic fleet management dashboard, below. Enjoy!

EV or gas – which is right for you?

SOURCES: Fleet Europe, Ford Pro, Geotab, McKinsey; add’l links in article.

If you’re considering going solar, it’s always a good idea to get quotes from a few installers. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

Geely-backed performance EV brand Polestar has had some troubling times in recent months, but its future is looking a whole lot better after the company secured a $600 million loan facility to help it keep on keepin’ on.

Despite vehicle sales picking up in 2025 on the strengths of the Polestar EV brand’s Swedish sensibilities, cutting-edge Chinese EV tech, and Volvo-aided safety specs, the company’s financial picture has been anything but rosy, with the threat of having its stock delisted from the NASDAQ looming large at several points.

In a vote of broader confidence and better times ahead, Volvo’s parent company Geely Sweden Holdings AB is backing the brand with more than half a billion dollars of fresh funding to extend its operational runway:

Polestar, as borrower, entered into a credit agreement with a wholly owned subsidiary, as lender, of Geely Sweden Holdings AB in relation to a subordinated term loan facility of up to USD 600 million, of which the last USD 300 million would require lender consent based on Polestar’s future liquidity needs. The term loan facility is available to Polestar for general corporate purposes.

The new funds are just the most recent part of a big week for Polestar – one that saw the Polestar 4 recently begin deliveries to its first North American customers, and recent upgrades to the Polestar 3 have made that car a viable V2G/V2x offering in Europe, as well. With that in mind, it’s no wonder that Geely wants to see how this all plays out.

The company has four models in its current line-up on sale in 28 countries, along with additional planned models that include the Polestar 7 SUV (set to be introduced in 2028) and the Polestar 6 coupe/roadster.

Electrek’s Take

Product-wise, at least, it’s hard to argue that Polestar’s future appears to be anything but bright. The new Polestar 3 crossover is a viable competitor to the industry-leading Tesla Model Y, and the upcoming Polestar 4 and 5 models seem like winners, too. To drive that point home, Polestar is promoting up to $18,000 in incentives to lure in Tesla buyers.

You can find out more about Polestar’s killer EV deals on the full range of Polestar models, from the 2 to the 4, below, then let us know what you think of the three-pointed star’s latest discount dash in the comments section at the bottom of the page.

SOURCE: Polestar.

If you’re considering going solar, it’s always a good idea to get quotes from a few installers. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

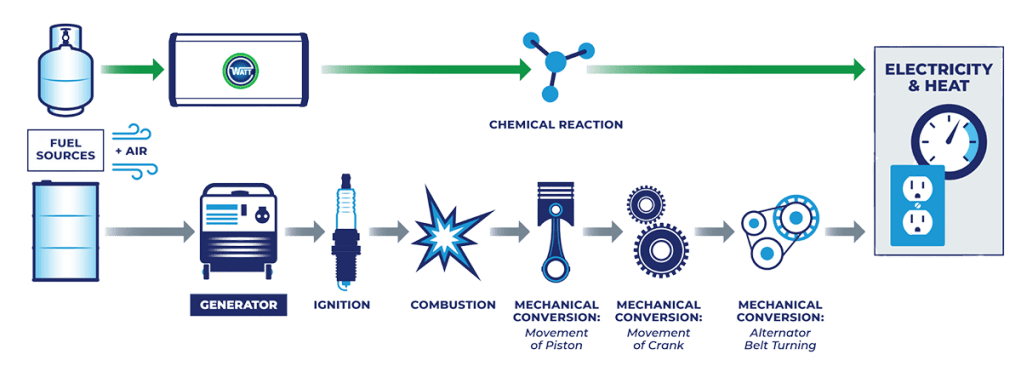

Whether it’s to keep the lights on after a natural disaster or just to avoid peak energy rates, more people than ever are adding battery energy storage to their home solar systems — but li-ion batteries aren’t the only option. The new WATT Fuel Cell uses the natural gas connection your home already has to generate power when you need it.

Technically a solid oxide fuel cell, the WATT unit turns the natural gas in your home into electricity without combustion, relying instead on a chemical reaction between the natural gas and oxygen in the air to create an electric current in a way that’s conceptually similar to a hydrogen fuel cell, but that makes use of a more readily available (and far cheaper) fuel source to generate power while producing far fewer harmful emissions than a conventional generator.

How it works

The company’s latest offering, the WATT HOME system, recently achieved certification at a 2 kW power rating, marking an important step on the company’s commercialization roadmap as it races to meet market demands for a natural-gas-powered backup solution to guarantee uptime in outage-prone regions.

This week, the company marked another major milestone by installing the of its first 2 kW WATT HOME solid oxide fuel cells (SOFC) at the Edward M. Smith National Career and Life Skills Development Center, Hope Gas’ new state-of-the-art training facility in Clarksburg, West Virginia – but the news doesn’t end there.

The company plans to take advantage of the new 30% ITC benefit (a federal tax credit that lets homeowners deduct 30% of the cost of qualifying clean energy systems, which now includes natural gas) under the One Big Beautiful Bill Act to help drive sales, with installations beginning in Hope Gas’ utility territory in Q1 of 2026.

“The WATT HOME system’s new 2 kW certification … validates the performance capabilities we’ve engineered for years and strengthens our competitive position as we move into multi-year deployment with Hope Gas,” says Caine Finnerty, WATT’s CEO and Founder. “With the ITC benefit, we anticipate accelerated adoption and substantial value for customers, utilities, and investors.”

The gas fuel cell can send power directly to the home’s panel, keeping the lights on directly, or perform the same function as a solar panel, sending power to a battery where it can be stored for later use.

Keep in mind, though – this isn’t a zero emissions option the way a solar + battery solution is. This is very much a fossil fuel-powered solution that gives off carbon and nitrous emissions, and the only reasons we’re talking about it are:

- the tech is kind of cool

- I didn’t know these existed

- it is objectively cleaner than a conventional ICE generator

That said, while solar is still the better solution in an ideal world, a WATT HOME fuel cell might be a better option in situations where rooftop space is limited (or nonexistent), such as condos or vertically-designed townhomes. In those scenarios, solar panels are unlikely to generate a meaningful amount of electricity, but a fuel cell that can tap into the buildings’ existing natural gas lines to provide reliable backup power if the grid fails.

That makes the fuel cell an attractive option for residents in multi-unit buildings, older historic neighborhoods with strict aesthetic rules, or any building where adding solar panels aren’t feasible, but a low-emission, low-noise backup solution is still needed.

The better question, then, isn’t is it better than solar – it’s is it better than solar for you? If you’re in West Virginia, you might be able to find out in just a few weeks. In the meantime, watch WATT’s own explainer video, below, then let us know what you think of the idea of a natural gas fuel cell in the comments.

Powering your home with a fuel cell

SOURCE | IMAGES: WATT, via PRNewswire.

If you’re considering going solar, it’s always a good idea to get quotes from a few installers. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024