Wilko job fears deepen as Poundland owner eyes swoop on 100 stores

The United States and European Union have agreed a trade deal, says Donald Trump.

The announcement was made as the US president met European Commission chief Ursula von der Leyen at one of his golf resorts in Scotland.

Speaking after talks in Turnberry, Mr Trump said the EU deal was the “biggest deal ever made” and it will be “great for cars”.

The US will impose 15% tariffs on EU goods into America, after Mr Trump had threatened a 30% levy.

He said there will be an EU investment of $600bn in the US, the bloc will buy $750bn in US energy and will also purchase US military equipment.

Mr Trump had earlier said the main sticking point was “fairness”, citing barriers to US exports of cars and agriculture.

He went into the talks demanding fairer trade with the 27-member EU and threatening steep tariffs to achieve that, while insisting the US will not go below 15% import taxes.

For months, Mr Trump has threatened most of the world with large tariffs in the hope of shrinking major US trade deficits with many key trading partners, including the EU.

Ms von der Leyen said the agreement would include 15% tariffs across the board, saying it would help rebalance trade between the two large trading partners.

In case there was no deal and the US had imposed 30% tariffs from 1 August, the EU has prepared counter-tariffs on €93bn (£81bn) of US goods.

Ahead of their meeting on Sunday, Ms von der Leyen described Mr Trump as a “tough negotiator and dealmaker”.

Listen to The World with Richard Engel and Yalda Hakim every Wednesday

This breaking news story is being updated and more details will be published shortly.

Please refresh the page for the latest version.

You can receive breaking news alerts on a smartphone or tablet via the Sky News app. You can also follow us on WhatsApp and subscribe to our YouTube channel to keep up with the latest news.

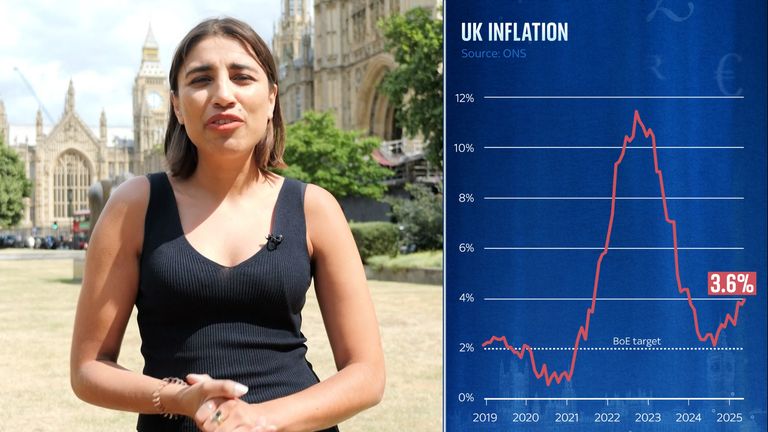

Retail sales grew in June as warm weather boosted spending and day trips, official figures show.

Spending on goods such as food, clothes and household items rose 0.9%, the Office for National Statistics (ONS) said.

It’s a bounce back from the 2.8% dip in May, but last month’s figure was below economists’ forecast 1.2% uplift as consumers dealt with higher prices from increased inflation.

Money blog: The odd rules that could land you with a big fine on holiday

Also weighing on spending was reduced consumer confidence amid talk of higher taxes, according to a closely watched indicator from market research firm GfK.

Retail sales figures are significant as they measure household consumption, the largest expenditure in the UK economy.

Growing retail sales can mean economic growth, which the government has repeatedly said is its top priority.

What does ‘inflation is rising’ mean?

Where have people been shopping?

June’s retail sales rise came as people bought more in supermarkets, and retailers said drinks sales were up.

While hot and sunny weather boosted some brick-and-mortar shops, the heat led some to head online.

Read more from Money:

Satellite tracker Spaceflux reaches lift-off with £5m funding boost

Trade war uncertainty prompts halt to eurozone rate cuts

Non-store retailers, which include mainly online shops, but also market stalls, had sold the most in more than three years.

Not since February 2022 had sales been so high as the Met Office said England had its warmest ever June, and the second warmest for the UK as a whole.

The June increases suggest that the May drop was a bump in the road. When looked at as a whole, the first six months of the year saw retail sales up 1.7%.

Filling up the car for day trips to take advantage of the sun played an important role in the retail sales growth.

When fuel is excluded, the rise was smaller, just 0.6%.

Welcome news

Despite lower consumer sentiment and more expensive goods, consumers are benefitting from rising wages and are cutting back on savings.

The ONS lifestyle survey – backed up by hard data like the Bank of England’s money and credit figures – shows that households have rebuilt their rainy day savings and are cutting back on the amount of money they squirrel away each month.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike