Why September will be a momentous month for US industry

It is one of the great set-piece moments in the US industrial calendar.

At the start of pay negotiations, which take place every four years ahead of the expiry of existing contracts in September, the leaders of the big three US carmakers traditionally shake hands in front of the cameras with the leader of the United Auto Workers (UAW) union.

The tradition goes back almost a century: Wayne State University in Detroit, America’s car-making capital, has unearthed photographs dating back to the 1930s showing the UAW leaders of the time shaking hands with a leader from Ford, Chrysler or General Motors.

The then UAW president Ron Gettelfinger and Ford president Alan Mulally take part in the ceremonial handshake in 2007

This was the precursor to another established tradition under which the UAW would select a lead company with which to negotiate. Then, once a deal had been struck, the other carmakers would follow the first company’s lead in a process known as ‘pattern bargaining’.

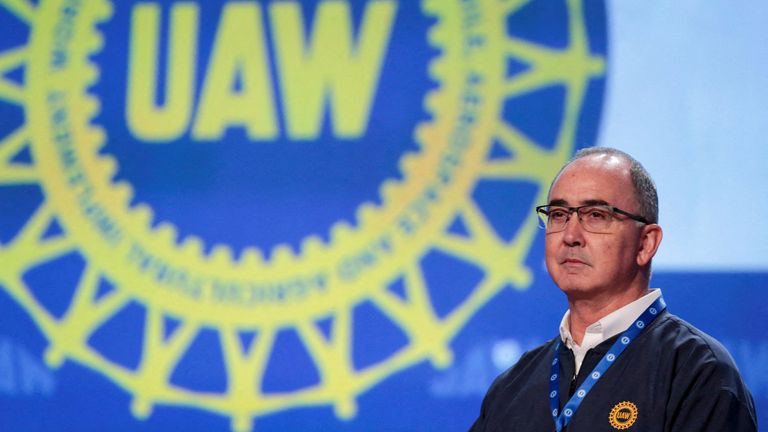

So it was a seismic moment when, in July this year, the UAW’s new president, Shawn Fain, declined to take part in the handshake.

Instead, he held what were described as a “member’s handshake”, during which he met with workers at the big three (Chrysler is now owned by Stellantis, also the parent company of European carmakers Peugeot and Fiat) as they came off their shifts.

It was intended to lay down a marker to the carmakers that this was a very different UAW leadership.

Mr Fain, 54, was narrowly elected president of the UAW in March this year on a platform of promising a tougher approach to pay negotiations.

His victory, over the existing president Ray Curry, was historic in that it was the first in which the president, and other leading officials, were chosen by a direct ballot of members rather than in a proverbial smoke-filled room in which delegates chose the leadership.

Shawn Fain, pictured in July, shaking hands with members outside a Ford assembly plant in Michigan

Mr Fain, in winning, toppled a faction of the union that had controlled it for decades.

On being elected, Mr Fain – who began his career as an electrician with Chrysler – immediately served notice on the carmakers that he did not intend this to be business as usual, declaring: “We’re here to come together to ready ourselves for the war against our one and only true enemy: multibillion corporations and employers that refuse to give our members their fair share. It’s a new day in the UAW.”

If that didn’t make the carmakers sit up and take note, Mr Fain’s refusal to take part in the traditional handshake did, as he told the union’s 389,000 members on his social media feed: “I’m not shaking hands with any CEOs until they do right by our members, and we fix the broken status quo with the big three. The members have to come first.”

For good measure, he very publicly threw a Stellantis pay offer in a bin.

Mr Fain’s approach is making waves on Wall Street.

There are real concerns that Mr Fain – who carries around with him one of his grandfather’s payslips from Chrysler in 1940 – will bring out his members at all three carmakers if a deal is not reached by the time the existing contracts expire on 14 September. Such action would be unprecedented.

Read more business news:

Bank of England’s ‘regrettable mistakes fuelled inflation’

B&M to snap up 51 Wilko stores

Birmingham City Council effectively declares bankruptcy

Members at the three have voted for strike action in the event of negotiations breaking down, by an average of 97%.

Strikes would cause immense disruption at a time when the carmakers are having to invest billions in electrification while trying to cut their costs in response to inflation.

Yet, with Wall Street putting the odds of strike action at the big three as better than events, the two sides look set for collision.

The UAW is not only seeking to restore past benefits lost in previous pay negotiations, but also to cut the working week to 32 hours.

It is also seeking a significant pay rise, the extent of which it has not made public, but which has been reported by the Wall Street Journal as 46%.

That would severely hobble the big three’s competitiveness against foreign rivals, from Germany and Japan – which tend to have less union representation in their workforces, as well as the likes of non-unionised Tesla.

Some 150,000 of the UAW’s members work for Ford, GM and Stellantis but strikes at all three would be huge because the union has traditionally singled out an individual carmaker for strike action rather than attacking several targets at once. It would also be a risk.

The union has a strike fund of $900m (£716m) – half of which would be eaten by a six-week stoppage in which striking members at the big three were each paid $500 (£398) a week.

That is why it has been suggested that Mr Fain may adopt another tactic, bringing out its members at the car parts makers instead, in time depriving the big three of components and forcing them to temporarily close plants while still having to pay workers.

UAW President Shawn Fain

That, though, would also be a risk for the UAW, as it is not nearly as well represented among the parts makers.

Mr Fain’s election is not just rattling Wall Street – but also in Washington. Mr Fain has refused to say whether the union will endorse and provide support to Joe Biden as he seeks re-election to the White House next year.

He told the Boston Globe at the weekend: “I’ve tried to be clear with people: The days of us just freely giving endorsements are over. Our endorsements have to be earned.”

Those comments speak to his unease that, as the Biden administration offers huge subsidies to businesses involved in the transition to net zero, it is not doing so with sufficient protection for carmakers.

He was particularly unhappy at a $9.2bn (£7.3bn) loan awarded by the Biden administration in June to a joint venture between Ford and a South Korean company to build three battery factories in Kentucky and Tennessee.

Mr Fain felt the loan should have come with strings attached on wages and working conditions.

He told the Globe: “We support a green economy. We have to have clean air, clean water, but this transition has to be a just transition. Workers can’t be left behind.”

Mr Fain’s election must also be seen in the context of changing circumstances in America’s unions.

The powerful Teamsters union, like the UAW, has also jettisoned the ruling faction that has run it for decades in favour of more radical leadership. Its aggressive stance is credited with having won it a pay deal with United Parcel Services reckoned to be the most generous in the company’s history.

Part-time workers at UPS were awarded a reported 50% pay rise while other concessions agreed by the company included a promise to instal air conditioning in all of its trucks.

Mr Fain is clearly optimistic that he has the wind to his back and can secure similar wins for his members. If he succeeds, other union leaders will be taking note.

It is why the month of September promises to be a momentous one for US industry.

Business

Budget 2025: Rachel Reeves vows to ‘take fair and necessary choices’ and ‘action on cost of living’

The chancellor is vowing to “take the fair and necessary choices” in today’s budget, as she seeks to grow the economy while keeping the public finances under control.

Rachel Reeves said she will not take Britain “back to austerity” – and promised to “take action to help families with the cost of living”.

She said she will “push ahead with the biggest drive for growth in a generation”, promising investment in infrastructure, housing, security, defence, education and skills.

But following a downgrade in the productivity growth forecast – combined with the U-turns on the winter fuel allowance and benefits cuts as well as “heightened global uncertainty” – the chancellor is expected to announce a series of tax rises as she tries to plug an estimated £30bn black hole in the public finances.

Conservative shadow chancellor Sir Mel Stride has said Ms Reeves is “trying to pull the wool over your eyes”, having promised last year she would not need to raise taxes again. Liberal Democrat deputy leader Daisy Cooper has accused her and the prime minister of “yet more betrayals”.

10 times the government promised not to increase taxes

‘Smorgasbord’ of tax rises

A headline tax-raising measure tomorrow is expected to be an extension of the freeze on income tax thresholds for another two years beyond 2028, which should raise about £8bn.

This move will be seized upon by opposition parties, given that the chancellor said at last year’s budget that extending the freeze, first brought in by the Tories in April 2021 to raise revenue amid vast spending during the pandemic, “would hurt working people” and “take more money out of their payslips”.

Watch our special programme for Budget 2025 live on Sky News from 11am.

What is being described as a “smorgasbord” of tax rises is also expected to be announced, having backed away from a manifesto-breaching income tax rise.

Some of the measures already confirmed by the government include:

• Allowing local authorities to impose a levy on tourists staying in their areas

• Expanding the sugar tax levy to packaged milkshakes and lattes

• Imposing extra taxes on higher-value properties

It is being reported that the chancellor will also put a cap on the tax-free allowance for salary sacrifice schemes, raise taxes on gambling firms, and bring in a pay-per-mile scheme for electric vehicles.

What could her key spending announcements be?

As well as filling the black hole in the public finances, these measures could allow the chancellor to spend money on a key demand of Labour MPs – partially or fully lifting the two-child benefits cap, which they say will have an immediate impact on reducing child poverty.

Benefits more broadly will be uprated in line with inflation, at a cost of £6bn, The Times reports.

In an attempt to help households with the cost of the living, the paper also reports that the chancellor will seek to cut energy bills by removing some green levies, which could see funding for some energy efficiency measures reduced.

Other measures The Times says she will announce include retaining the 5p cut in fuel duty, and extending the Electric Car Grant by an extra year, which gives consumers a £3,750 discount at purchase.

The government has already confirmed a number of key announcements, including:

• An above-inflation £550 a year increase in the state pension for 13 million eligible pensioners

• A freeze in prescription prices and rail fares

• £5m to refresh libraries in secondary schools

What the budget will mean for you

Extra funding for the NHS will also be announced in a bid to slash waiting lists, including the expansion of the “Neighbourhood Health Service” across the country to bring together GP, nursing, dentistry and pharmacy services – as well as £300m of investment into upgrading technology in the health service.

And although the cost of this is borne by businesses, the chancellor will confirm a 4.1% rise to the national living wage – taking it to £12.71 an hour for eligible workers aged 21 and over.

For a full-time worker over the age of 21, that means a pay increase of £900 a year.

Read more from Sky News:

Reeves issues ‘pick ‘n’ mix’ warning ahead of budget

Are we set for another astoundingly complex budget?

Sky News goes inside the room where the budget happens

Britons facing ‘cost of living permacrisis’

However, the Tories have hit out at the chancellor for the impending tax rises, with shadow chancellor Sir Mel Stride saying in a statement: “Having already raised taxes by £40bn, Reeves said she had wiped the slate clean, she wouldn’t be coming back for more and it was now on her. A year later and she is set to break that promise.”

He described her choices as “political weakness” = choosing “higher welfare and higher taxes”, and “hardworking families are being handed the bill”.

The Liberal Democrat deputy leader Daisy Cooper is also not impressed, and warned last night: “The economy is at a standstill. Despite years of promises from the Conservatives and now Labour to kickstart growth and clamp down on crushing household bills, the British people are facing a cost-of-living permacrisis and yet more betrayals from those in charge.”

She called on the government to negotiate a new customs union with the EU, which she argues would “grow our economy and bring in tens of billions for the Exchequer”.

Green Party leader Zack Polanski has demanded “bold policies and bold choices that make a real difference to ordinary people”.

Business

Budget 2025: Three things Rachel Reeves’s speech boils down to – and two tricks the chancellor will fall back on

This is going to be a big budget – not to mention a complex budget.

It could, depending on how it lands, determine the fate of this government. And it’s hard to think of many other budgets that have been preceded by quite so much speculation, briefing, and rumour.

All of which is to say, you could be forgiven for feeling rather overwhelmed.

But in practice, what’s happening this week can really be boiled down to three things.

1. Not enough growth

The first is that the economy is not growing as fast as many people had hoped. Or, to put it another way, Britain’s productivity growth is much weaker than it once used to be.

The upshot of that is that there’s less money flowing into the exchequer in the form of tax revenues.

2. Not enough cuts

The second factor is that last year and this, the chancellor promised to make certain cuts to welfare – cuts that would have saved the government billions of pounds of spending a year.

But it has failed to implement those cuts. Put those extra billions together with the shortfall from that weaker productivity, and it’s pretty clear there is a looming hole in the public finances.

3. Not enough levers

The third thing to bear in mind is that Rachel Reeves has pledged to tie her hands in the way she responds to this fiscal hole.

She has fiscal rules that mean she can’t ignore it. She has a manifesto pledge which means she is somewhat limited in the levers she can pull to fill it.

Put it all together, and it adds up to a momentous headache for the chancellor. She needs to raise quite a lot of money and all the “easy” ways of doing it (like raising income tax rates or VAT) seem to be off the table.

The Budget Explained – in 60 seconds

So… what will she do?

Quite how she responds remains to be seen – as does the precise size of the fiscal hole. But if the rumours in Westminster are to be believed, she will fall back upon two tricks most of her predecessors have tried at various points.

First, she will deploy “fiscal drag” to squeeze extra income tax and national insurance payments out of families for the coming five years.

What this means in practice is that even though the headline rate of income tax might not go up, the amount of income we end up being taxed on will grow ever higher in the coming years.

Second, the chancellor is expected to squeeze government spending in the distant years for which she doesn’t yet need to provide detailed plans.

Together, these measures may raise somewhere in the region of £10bn. But Reeves’s big problem is that in practice she needs to raise two or three times this amount. So, how will she do that?

Most likely is that she implements a grab-bag of other tax measures: more expensive council tax for high value properties; new CGT rules; new gambling taxes and more.

No return to austerity, but an Osborne-like predicament…

If this summons up a particular memory from history, it’s precisely the same problem George Osborne faced back in 2012. He wanted to raise quite a lot of money but due to agreements with his coalition partners, he was limited in how many big taxes he could raise.

The resulting budget was, at the time at least, the single most complex budget in history. Consider: in the years between 1970 and 2010 the average UK budget contained 14 tax measures. Osborne’s 2012 budget contained a whopping 61 of them.

And not long after he delivered it, the budget started to unravel. You probably recall the pasty tax, and maybe the granny tax and the charity tax. Essentially, he was forced into a series of embarrassing U-turns. If there was a lesson, it was that trying to wodge so many money-raising measures into a single fiscal event was an accident waiting to happen.

Can the budget fix economic woes?

Except that… here’s the interesting thing. In the following years, the complexity of budgets didn’t fall – it rose. Osborne broke his own complexity record the next year with the 2013 budget (73 tax measures), and then again in 2016 (86 measures). By 2020 the budget contained a staggering 103 measures. And Reeves’s own first budget, last autumn, very nearly broke this record with 94 measures.

In short, budgets have become more and more complex, chock-full of even more (often microscopic) tax measures.

Read more from Sky News:

What tax measures are expected in budget?

The political jeopardy facing Rachel Reeves in budget

In part, this is a consequence of the fact that, long ago, chancellors seem to have agreed that it would be political suicide to raise the basic rate of income tax or VAT. The consequence is that they have been forced to resort to ever smaller and fiddlier measures to make their numbers add up.

The question is whether this pattern continues this week. Do we end up with yet another astoundingly complex budget? Will that slew of measures backfire as they did for Osborne in 2012? And, more to the point, will they actually benefit the UK economy?

Business

Budget 2025: Three things Rachel Reeves’s speech boils down to – and two tricks the chancellor will fall back on

This is going to be a big budget – not to mention a complex budget.

It could, depending on how it lands, determine the fate of this government. And it’s hard to think of many other budgets that have been preceded by quite so much speculation, briefing, and rumour.

All of which is to say, you could be forgiven for feeling rather overwhelmed.

But in practice, what’s happening this week can really be boiled down to three things.

1. Not enough growth

The first is that the economy is not growing as fast as many people had hoped. Or, to put it another way, Britain’s productivity growth is much weaker than it once used to be.

The upshot of that is that there’s less money flowing into the exchequer in the form of tax revenues.

2. Not enough cuts

The second factor is that last year and this, the chancellor promised to make certain cuts to welfare – cuts that would have saved the government billions of pounds of spending a year.

But it has failed to implement those cuts. Put those extra billions together with the shortfall from that weaker productivity, and it’s pretty clear there is a looming hole in the public finances.

3. Not enough levers

The third thing to bear in mind is that Rachel Reeves has pledged to tie her hands in the way she responds to this fiscal hole.

She has fiscal rules that mean she can’t ignore it. She has a manifesto pledge which means she is somewhat limited in the levers she can pull to fill it.

Put it all together, and it adds up to a momentous headache for the chancellor. She needs to raise quite a lot of money and all the “easy” ways of doing it (like raising income tax rates or VAT) seem to be off the table.

The Budget Explained – in 60 seconds

So… what will she do?

Quite how she responds remains to be seen – as does the precise size of the fiscal hole. But if the rumours in Westminster are to be believed, she will fall back upon two tricks most of her predecessors have tried at various points.

First, she will deploy “fiscal drag” to squeeze extra income tax and national insurance payments out of families for the coming five years.

What this means in practice is that even though the headline rate of income tax might not go up, the amount of income we end up being taxed on will grow ever higher in the coming years.

Second, the chancellor is expected to squeeze government spending in the distant years for which she doesn’t yet need to provide detailed plans.

Together, these measures may raise somewhere in the region of £10bn. But Reeves’s big problem is that in practice she needs to raise two or three times this amount. So, how will she do that?

Most likely is that she implements a grab-bag of other tax measures: more expensive council tax for high value properties; new CGT rules; new gambling taxes and more.

No return to austerity, but an Osborne-like predicament…

If this summons up a particular memory from history, it’s precisely the same problem George Osborne faced back in 2012. He wanted to raise quite a lot of money but due to agreements with his coalition partners, he was limited in how many big taxes he could raise.

The resulting budget was, at the time at least, the single most complex budget in history. Consider: in the years between 1970 and 2010 the average UK budget contained 14 tax measures. Osborne’s 2012 budget contained a whopping 61 of them.

And not long after he delivered it, the budget started to unravel. You probably recall the pasty tax, and maybe the granny tax and the charity tax. Essentially, he was forced into a series of embarrassing U-turns. If there was a lesson, it was that trying to wodge so many money-raising measures into a single fiscal event was an accident waiting to happen.

Can the budget fix economic woes?

Except that… here’s the interesting thing. In the following years, the complexity of budgets didn’t fall – it rose. Osborne broke his own complexity record the next year with the 2013 budget (73 tax measures), and then again in 2016 (86 measures). By 2020 the budget contained a staggering 103 measures. And Reeves’s own first budget, last autumn, very nearly broke this record with 94 measures.

In short, budgets have become more and more complex, chock-full of even more (often microscopic) tax measures.

Read more from Sky News:

What tax measures are expected in budget?

The political jeopardy facing Rachel Reeves in budget

In part, this is a consequence of the fact that, long ago, chancellors seem to have agreed that it would be political suicide to raise the basic rate of income tax or VAT. The consequence is that they have been forced to resort to ever smaller and fiddlier measures to make their numbers add up.

The question is whether this pattern continues this week. Do we end up with yet another astoundingly complex budget? Will that slew of measures backfire as they did for Osborne in 2012? And, more to the point, will they actually benefit the UK economy?

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024