Oracle stock is poised for its steepest drop since 2002 on weak revenue guidance

Oracle chief technology officer Larry Ellison speaks at a company event in Redwood Shores, Calif., on Aug. 7, 2018.

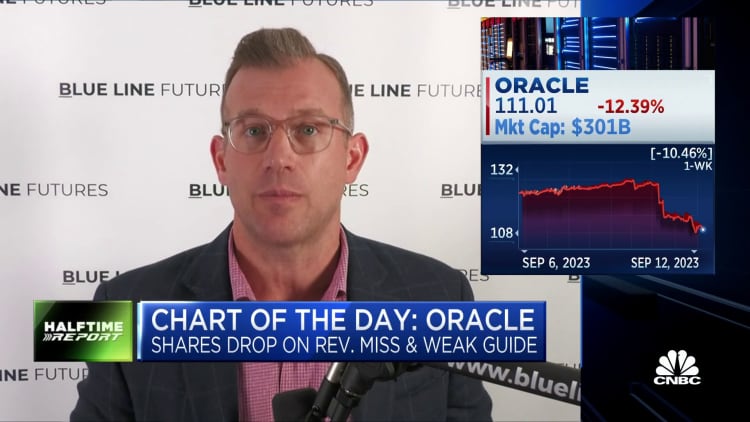

Oracle livestream screenshot

Oracle shares plummeted more than 12% on Tuesday and headed for their worst day in over two decades after the software maker reported disappointing revenue and issued weaker-than-expected guidance.

The last time it had a steeper percentage drop was a 15% decline in March 2002, at the tail end of the dot-com bust.

The plunge on Tuesday resulted in Oracle Chair Larry Ellison losing roughly $18 billion in wealth. Ellison is the world’s fourth-richest person, with a net worth of $142.5 billion, according to Forbes, just behind Amazon founder Jeff Bezos and ahead of Warren Buffett.

While Oracle’s earnings topped estimates, the company reported fiscal first-quarter revenue of $12.45 billion, falling short of the $12.47 billion average analyst estimate, according to LSEG. For the current quarter, Oracle said revenue will increase 5% to 7%, falling short of the 8% average analyst estimate.

Like big companies across the tech sector, Oracle has been selling investors on the benefits of artificial intelligence to its business. During the quarter, it added AI features in its Fusion Cloud and Human Capital Management Software, and Ellison said in the earnings statement that “as of today, AI development companies have signed contracts to purchase more than $4 billion of capacity in Oracle’s Gen2 Cloud,” double the amount it had booked at the end of the prior quarter.

However, analysts at Stifel wrote in a report after the results that “it is clear that investors were pricing in more AI and cloud-related upside.” The firm has a hold rating on the stock and a $120 price target.

Oracle CEO Safra Catz pointed to challenges at the company’s Cerner unit. In June of last year, Oracle closed the $28.2 billion purchase of the electronic health record software company, and now it’s in an “accelerated transition” to the cloud, Catz said.

“This transition is resulting in some near-term headwinds to the Cerner growth rate as customers move from licensed purchases, which are recognized upfront, to cloud subscriptions which are recognized ratably,” she said.

Revenue in Oracle’s cloud services and license support segment rose 13% from a year earlier, topping StreetAccount’s consensus of $9.44 billion. But sales in the cloud license and on-premises license segment fell 10% to $809 million, missing estimates.

Even with Tuesday’s stock drop, Oracle shares are up 36% year to date, beating the S&P 500, which is up 17%.

— CNBC’s Jordan Novet contributed to this report

WATCH: Oracle’s near-term volatility means investors should manage risk

A trader works on the floor of the New York Stock Exchange on Oct. 30, 2025 in New York.

Angela Weiss | AFP | Getty Images

This week’s equity market wobble, which saw a retreat in U.S. artificial intelligence-related stocks amid ongoing concerns over stretched valuations, has thrust contagion fears into the spotlight for global investors.

Goldman Sachs CEO David Solomon warned this week of a “likely” 10-20% drawdown in equity markets at some point within the next two years, while the International Monetary Fund and the Bank of England have both sounded the alarm bells.

Bank of England Governor Andrew Bailey highlighted the possibilities of an AI bubble in an interview with CNBC on Thursday, noting that the “very positive productivity contribution” from technology companies could be offset by uncertainty around future earning steams in the sector.

“We have to be very alert to these risks,” Bailey said.

Legrand is one of several European companies which is benefitting from the AI boom. The French company, which sells products to Alphabet, Amazon and others to help cool servers, has seen its shares surge 37% this year, roughly as much as Nvidia.

Anders Danielsson, CEO of Swedish construction group Skanska, which builds data centers and other AI infrastructure assets, shrugged off concerns about a slowdown.

“In the U.S. we have a very strong pipeline of data centers — we don’t see any slowdown there,” he told CNBC. “We are working with large international customers and they are also interested in building data centers in central Europe, and in the Nordics and the U.K. We haven’t seen any slowdown really.”

Meanwhile Kiran Ganesh, multi-asset strategist at UBS, highlighted a notable lack of volatility, adding that the broader narrative remains positive.

“We’ve had a remarkably smooth rally given the scale of investment that’s taken place, given the uncertainty about future cash flows, and given some of those concerns about valuation,” Ganesh told CNBC’s “Europe Early Edition” on Friday.

“As we’ve gone through earnings season, I think it’s reasonable to have expected some volatility, but actually when we look at the results, and they have been reassuring, we’re still up over the course of earnings season and they have been beating expectations. So although some volatility has been materializing this week, we think that’s to be expected and the bigger picture still remains positive.”

Still, many investors appear to be souring on the increasingly-stretched valuations.

In Asia, shares of SoftBank Group — which is active across AI infrastructure, semiconductor and application companies — have fallen sharply, with the Japanese group suffering almost $50 billion in weekly losses. SoftBank resumed its downward trajectory on Friday, after dropping about 10% on Wednesday.

On Tuesday, it emerged that Scion Asset Management, the hedge fund led by “The Big Short” investor Michael Burry, had built short positions against both Palantir Technologies and Nvidia, drawing the ire of Palantir CEO Alex Karp.

“Some big tech stocks are on sale, and are presenting buying opportunities for investors, especially for investors who have missed out on the market’s strength over the past two months,” said Glen Smith, chief investment officer at GDS Wealth Management.

Other investors have flagged concentration risk in U.S. equities, and advocate looking further afield.

Luca Paolini, chief strategist at Pictet Asset Management, said stretched valuations mean the firm is neutral on U.S. names. “Emerging markets are preferred, with diversified exposure across India, Brazil, and broader EM benefiting from AI-driven investment and monetary easing,” Paolini said in a market commentary.

Technology

CEO of Southeast Asia’s largest bank warns investors: ‘Buckle up, we’re in for a volatile ride’

Tan Su Shan is the CEO and director of DBS Group.

Bloomberg | Bloomberg | Getty Images

With valuations in the U.S. stock market becoming increasingly stretched, the chief executive of Southeast Asia’s largest bank is warning investors to expect turbulence ahead.

“We’ve seen a lot of volatility in the markets. It could be equities, it could be rates, it could be foreign exchange,” DBS CEO Tan Su Shan told CNBC, adding that she expects that volatility to continue.

Tan, who took over the helm of DBS from longtime CEO Piyush Gupta in March, said that investors were particularly worried about the lofty valuations of artificial intelligence stocks, especially the so-called “Magnificent Seven.”

The Magnificent Seven — Amazon, Alphabet, Meta, Apple, Microsoft, Nvidia and Tesla — are some of the major U.S. tech and growth stocks that have driven much of Wall Street’s gains in recent years.

“You’ve got trillions of dollars tied up in seven stocks, for example. So it’s inevitable, with that kind of concentration, that there will be a worry about. ‘You know, when will this bubble burst?'”

Earlier this week, at the Global Financial Leaders’ Investment Summit in Hong Kong, it was likely there would be a 10%-20% drawdown over the next 12 to 24 months.

Morgan Stanley CEO Ted Pick said at the same summit that investors should welcome periodic pullbacks, calling them healthy developments rather than signs of crisis.

Tan agreed. “Frankly, a correction will be healthy,” she said.

Recent examples include Advanced Micro Devices and Palantir, both of which posted stronger-than-expected quarterly results on Tuesday, yet their shares — and the wider Nasdaq — fell.

Her remarks follow similar warnings by the International Monetary Fund and central bank chiefs Jerome Powell and Andrew Bailey, who have all cautioned about inflated stock prices.

Singapore as diversification play

Tan advised investors to diversify rather than concentrate holdings in one market. “Whether it’s in your portfolio, in your supply chain, or in your demand distribution, just diversify.”

Tan, who has over 35 years of experience in banking and wealth management, noted that Asia could attract more investment from the U.S.—and that it’s not a bad thing.

Singling out Singapore and the country’s central bank’s efforts to boost interest in the local markets, Tan described the city-state as a “diversifier market.”

“We’ve got rule of law. We’re a transparent, open financial system and stable politically. We’re a good place to invest…. So I don’t think we’re a bad place to think about diversifying your investments.”

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024