Tesla has a well-known lead in the US electric vehicle market, but these two new charts help visualize that lead to a degree that should embarrass all other automakers in the US.

For over almost a decade now, Tesla has been the EV market in the US.

My Grammarly is asking me to correct to “in the EV market,” but no. I do mean it is the EV market.

Without Tesla, the US EV market would simply not be the same. For years, Tesla vehicles represented over 80% of the market.

Over the last few years, it has capitulated some market shares to other automakers as more models hit the market, but Tesla is still very much in the lead.

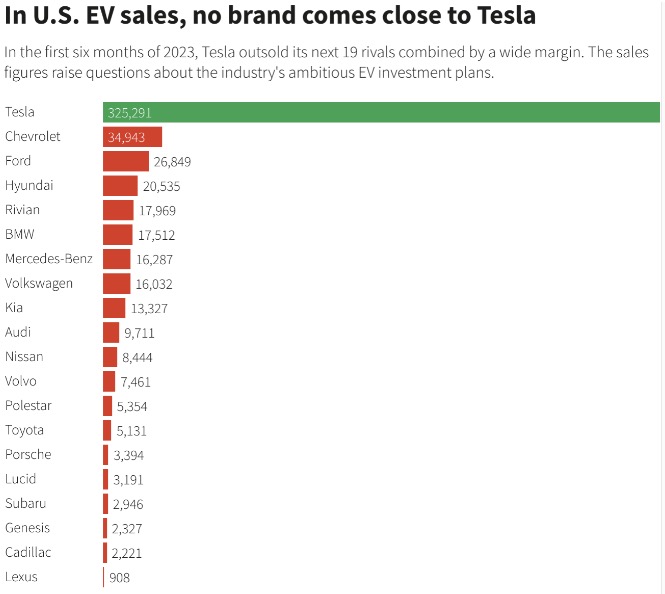

Reuters has recently released new charts based on S&P Global Mobility data about EV sales so far this year in the US.

The charts visualize well the lead that Tesla has over other automakers:

Tesla outsold the next 19 EV competitors combined during the first half of 2023.

To be fair, Tesla doesn’t break down sales per market and therefore, the 325,000 EV deliveries in the first half of the year is an estimate, but it should be accurate within at least a 20% margin and impressive even if wrong by that much.

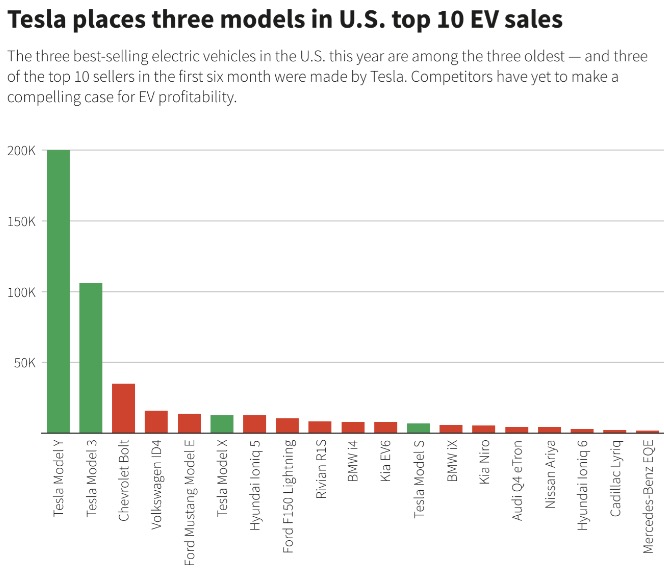

Tesla’s lead is also well illustrated in this chart that breaks down sales per EV model:

Electrek’s Take

The good news for the rest of the world is that Tesla’s lead is much less prominent in other markets like Europe and Asia.

But in the US, it is absolutely ridiculous.

Considering that electric vehicles are undoubtedly the future of the auto industry, I don’t think that’s argued anymore, it should be extremely worrying to other automakers.

Unless they can drastically change this pace amid the rapid adoption of electric vehicles, they are going to lose most of the US market – a highly profitable auto market.

The good news is that there are a few new non-Tesla EV models coming to the US that should help, and Tesla helped the rest of the market greatly by opening the Supercharger network to everyone else.

Without that, Tesla could have probably run with the whole thing. It shows that the company is still staying true to its mission of accelerating the world’s transition to electric transport and renewable energy.

If its mission was to own the electric transport market, they might have not gone through with opening the Supercharger network – government incentives or not.

FTC: We use income earning auto affiliate links.More.

Metro Detroit is about to get a big boost of fast EV chargers, with more than 40 new ChargePoint ports set to come online across multiple sites owned by the Dabaja Brothers Development Group.

The first ultra-fast charging site just opened in Canton, Michigan. It’s owned and operated by Dabaja Brothers, who plan to follow it with additional ChargePoint-equipped locations in Dearborn and Livonia.

“We started this project because we saw a gap in our community – there was almost nowhere to charge an EV in Canton, and a similar lack of charging across metro Detroit,” said Yousef Dabaja, owner/operator at Dabaja Brothers.

Each metro Detroit site will feature ChargePoint Express Plus fast charging stations, which can deliver up to 500 kW to a single port, can fast-charge two vehicles at the same time, and are compatible with all EVs. The stations feature a proprietary cooling system to deliver peak charging speeds for sustained periods, ensuring that charging speed remains consistent.

Advertisement – scroll for more content

The stations operate on the new ChargePoint Platform, which enables operators to monitor performance, adjust pricing, troubleshoot issues, and gain real-time insights to keep chargers running smoothly.

Rick Wilmer, CEO at ChargePoint, said, “This initiative will rapidly infill the ‘fast charging deserts’ across the Detroit area, allowing drivers to quickly recharge their vehicles when and where they need to.”

If you’re looking to replace your old HVAC equipment, it’s always a good idea to get quotes from a few installers. To make sure you’re finding a trusted, reliable HVAC installer near you that offers competitive pricing on heat pumps, check out EnergySage. EnergySage is a free service that makes it easy for you to get a heat pump. They have pre-vetted heat pump installers competing for your business, ensuring you get high quality solutions. Plus, it’s free to use!

Your personalized heat pump quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here. – *ad

FTC: We use income earning auto affiliate links.More.

Mercedes-Benz High-Power Charging and Starbucks have officially opened their first DC fast charging hub together, off the I-5 in Red Bluff, California.

The 400 kW Mercedes-Benz chargers are capable of adding up to 300 miles in 10 minutes, depending on the EV, and every stall has both NACS and CCS cables – they’re fully open DC fast chargers.

Mercedes-Benz HPC North America, a joint venture between subsidiaries of Mercedes-Benz Group and renewable energy producer MN8 Energy, first announced in July 2024 that it would install DC fast chargers at Starbucks stores along Interstate 5, the main 1,400-mile north-south interstate highway on the US West Coast from Canada to Mexico. Ultimately, Mercedes plans to install fast chargers at 100 Starbucks stores across the US.

Mercedes-Benz HPC opened its first North American charging site at Mercedes-Benz USA’s headquarters in Sandy Springs, Georgia, in November 2023 as part of an initial $1 billion charging network investment. As of the end of 2024, Mercedes had deployed over 150 operational fast chargers in the US, but it hasn’t disclosed an official number of how many chargers are currently online.

Advertisement – scroll for more content

Andrew Cornelia, CEO of Mercedes-Benz HPC North America, is leaving the company at the end of the month to become global head of electrification & sustainability at Uber.

If you’re looking to replace your old HVAC equipment, it’s always a good idea to get quotes from a few installers. To make sure you’re finding a trusted, reliable HVAC installer near you that offers competitive pricing on heat pumps, check out EnergySage. EnergySage is a free service that makes it easy for you to get a heat pump. They have pre-vetted heat pump installers competing for your business, ensuring you get high quality solutions. Plus, it’s free to use!

Your personalized heat pump quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here. – *ad

FTC: We use income earning auto affiliate links.More.

The race for autonomous driving has three fronts: software, hardware, and regulatory. For years, we’ve watched Tesla try to brute-force its way to “Full Self-Driving (FSD)” with its own custom hardware, while the rest of the automotive industry is increasingly lining up behind NVIDIA.

Here’s a table comparing the two chips with the best possible specs I could find. greentheonly’s teardown was particularly useful. If you find things you think are not accurate, please don’t hesitate to reach out:

Feature / Specification

Tesla AI4 (Hardware 4.0)

NVIDIA Drive Thor (AGX / Jetson)

Developer / Architect

Tesla (in-house)

NVIDIA

Manufacturing Process

Samsung 7nm (7LPP class)

TSMC 4N (custom 5nm class)

Release Status

In production (shipping since 2023)

In production since 2025

CPU Architecture

ARM Cortex-A72 (legacy)

ARM Neoverse V3AE (server-grade)

CPU Core Count

20 cores (5× clusters of 4 cores)

14 cores (Jetson T5000 configuration)

AI Performance (INT8)

~100–150 TOPS (dual-SoC system)

1,000 TOPS (per chip)

AI Performance (FP4)

Not supported / not disclosed

2,000 TFLOPS (per chip)

Neural Processing Unit

3× custom NPU cores per SoC

Blackwell Tensor Cores + Transformer Engine

Memory Type

GDDR6

LPDDR5X

Memory Bus Width

256-bit

256-bit

Memory Bandwidth

~384 GB/s

~273 GB/s

Memory Capacity

~16 GB typical system

Up to 128 GB (Jetson Thor)

Power Consumption

Est. 80–100 W (system)

40 W – 130 W (configurable)

Camera Support

5 MP proprietary Tesla cameras

Scalable, supports 8MP+ and GMSL3

Special Features

Dual-SoC redundancy on one board

Native Transformer Engine, NVLink-C2C

The most striking difference right off the bat is the manufacturing process. NVIDIA is throwing everything at Drive Thor, using TSMC’s cutting-edge 4N process (a custom 5nm-class node). This allows them to pack in the new Blackwell architecture, which is essentially the same tech powering the world’s most advanced AI data centers.

Advertisement – scroll for more content

Tesla, on the other hand, pulled a move that might surprise spec-sheet warriors. Teardowns confirm that AI4 is built on Samsung’s 7nm process. This is mature, reliable, and much cheaper than TSMC’s bleeding-edge nodes.

When you look at the compute power, NVIDIA claims a staggering 2,000 TFLOPS for Thor. But there’s a catch. That number uses FP4 (4-bit floating point) precision, a new format designed specifically for the Transformer models used in generative AI.

Tesla’s AI4 is estimated to hit around 100-150 TOPS (INT8) across its dual-SoC redundant system. On paper, it looks like a slaughter, but Tesla made a very specific engineering trade-off that tells us exactly what was bottling up their software: memory bandwidth.

Tesla switched from LPDDR4 in HW3 to GDDR6 in HW4, the same power-hungry memory you find in gaming graphics cards (GPUs). This gives AI4 a massive memory bandwidth of approximately 384 GB/s, compared to Thor’s 273 GB/s (on the single-chip Jetson config) using LPDDR5X.

This suggests Tesla’s vision-only approach, which ingests massive amounts of raw video from high-res cameras, was starving for data.

Based on Elon Musk’s comments that Tesla’s AI5 chip will have 5x the memory bandwidth, it sounds like it might still be Tesla’s bottleneck.

Here is where Tesla’s cost-cutting really shows. AI4 is still running on ARM Cortex-A72 cores, an architecture that is nearly a decade old. They bumped the core count to 20, but it’s still old tech.

NVIDIA Thor, meanwhile, uses the ARM Neoverse V3AE, a server-grade CPU explicitly designed for the modern software-defined vehicle. This allows Thor to run not just the autonomous driving stack, but the entire infotainment system, dashboard, and potentially even an in-car AI assistant, all on one chip.

Thor has found many takers, especially among Tesla EV competitors such as BYD, Zeekr, Lucid, Xiaomi, and many more.

Electrek’s Take

There’s one thing that is not in there: price. I would assume that Tesla wins on that front, and that’s a big part of the project. Tesla developed a chip that didn’t exist, and that it needed.

It was an impressive feat, but it doesn’t make Tesla an incredible leader in silicon for self-driving.

Tesla is maxing out AI4. It now uses both chips, making it less likely to achieve the redundancy levels you need to deliver level 4-5 autonomy.

Meanwhile, we don’t have a solution for HW3 yet and AI5 is apparently not coming to save the day until 2027.

By then, there will likely be millions of vehicles on the road with NVIDIA Thor processors.

FTC: We use income earning auto affiliate links.More.