Q3 earnings preview: tough quarter")

Tesla (TSLA) Q3 earnings preview: tough quarter

Tesla (TSLA) is about to release Q3 2023 financial results on Wednesday, October 18, after the markets close. As usual, a conference call and Q&A with Tesla’s management are scheduled after the results.

Here, we’ll take a look at what both the street and retail investors are expecting for the quarterly results.

Tesla Q3 2023 deliveries

As usual, Tesla already disclosed its Q3 vehicle delivery and production numbers, which drive the vast majority of the company’s revenue.

Earlier this month, Tesla confirmed that it delivered just over 435,000 electric vehicles during the third quarter of the year.

It’s the first time in a long time that Tesla didn’t break a delivery record.

Tesla also produced fewer vehicles at just over 430,000 units.

The automaker had warned about a lower quarter in terms of deliveries and production due to planned factory shutdowns for upgrades.

Delivery and production numbers are always slightly adjusted during earning results.

Tesla Q3 2023 revenue

For revenue, analysts generally have a pretty good idea of what to expect, thanks to the delivery numbers.

However, this year has been more difficult due to constant price cuts – making it harder to track Tesla’s revenue.

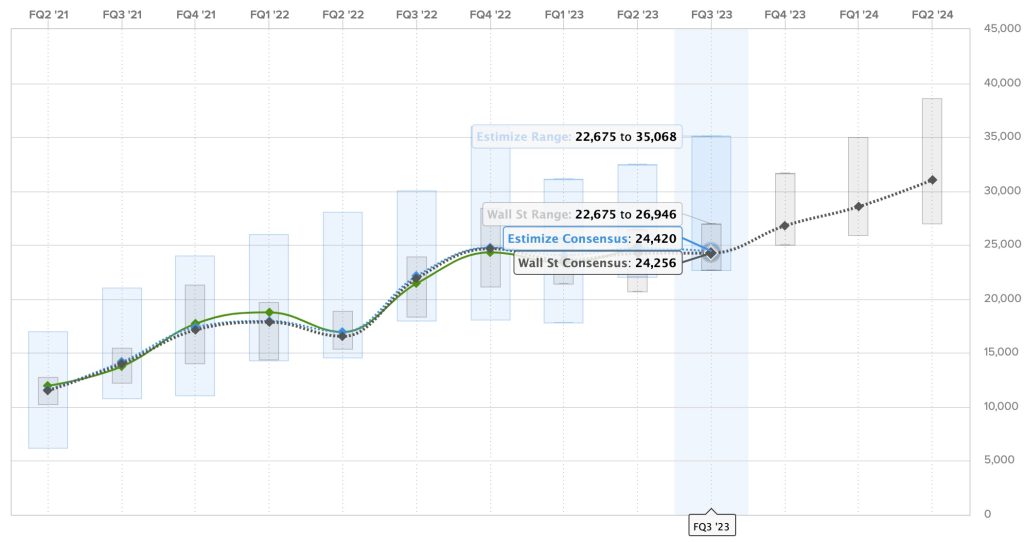

The Wall Street consensus for this quarter is $24.256 billion, and Estimize, the financial estimate crowdsourcing website, predicts a higher revenue of $24.420 billion.

Unsurprisingly, this would be significantly down from the nearly $25 billion in revenue Tesla delivered last quarter, but it is still a massive year-over-year increase from the $21.5 billion Tesla delivered during the same quarter last year.

Here are the predictions for Tesla’s revenue over the past two years, with Estimize predictions in blue, Wall Street consensus in gray, and actual results are in green:

Tesla Q3 2023 earnings

Tesla always attempts to be marginally profitable every quarter as it invests most of its money into growth, and it has been successful in doing so over the last two years now.

However, like revenues, it has been harder to estimate earnings this year with price cuts digging into Tesla’s industry-leading gross margins.

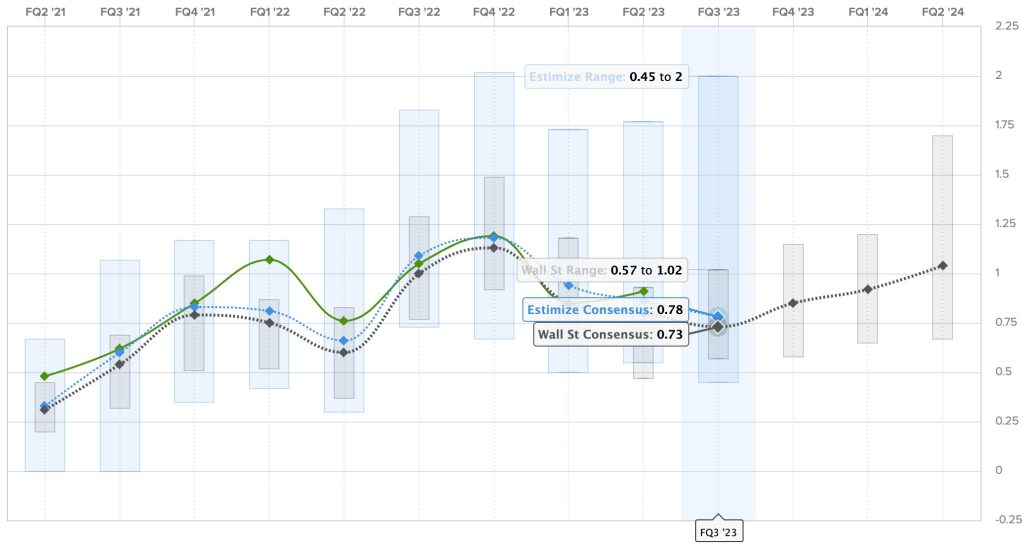

For Q3 2023, the Wall Street consensus is a gain of $0.73 per share, while Estimize’s prediction is higher with a profit of $0.78 per share.

But as you can see below, the range of Wall Street is quite broad as analysts are unsure what to expect.

Here are the earnings per share over the last two years, where Estimize predictions are in blue, Wall Street consensus is in gray, and actual results are in green:

Other expectations for the TSLA shareholder’s letter and analyst call

Amid declining prices to keep demand up, most shareholders are mostly concerned about Tesla’s ability to retain a high gross margin despite the lower prices.

It’s likely that Tesla will try to reassure shareholders on that front on Wednesday.

There’s been a growing effort among shareholders to convince Tesla to invest in advertising rather than cut prices. We have seen Tesla dip its toes in that lately. It would be interesting to see if Tesla can release some results of that effort and discuss the potential for a ramp-up.

During the conference call following the release of its earning results, Tesla takes crowdsourced questions from shareholders. Here are the top-voted ones right that are likely to be answered by management:

- How many Cybertruck deliveries do you anticipate for 2024?

- Can you provide a progress update on the 4680 Cell. Particularly progress towards performance improvements and cost savings outlined on battery day. Thank you!

- When do you expect Model 3 Highland to be available in the US?

- Could you please provide an update on (i) capacity expansion plans for the company’s factories in Berlin and Austin and (ii) the opening schedule of Gigafactory Mexico?

- Why was the price dropped on FSD if it is getting better and robotaxi is expected so soon?

In general, between the price drop and the lower deliveries, it should be a fairly top quarter for Tesla. However, the automaker has also lowered inventory during the quarter, which could make things more interesting.

We will see.

You can join us live on Electrek on Wednesday evening for intensive coverage of Tesla’s Q3 2023 financial results starting at around 4 p.m. ET for the results and through the evening for news coming out of the conference call and results.

FTC: We use income earning auto affiliate links. More.

Environment

Archer Aviation is planning an air taxi network around the Miami metro area including airports

Archer Aviation has announced partnerships in the Miami metropolitan area to establish a new air taxi network to support travelers around several key areas in Southern Florida, including local airports.

As you probably alrready know at this point. Archer Aviation ($ACHR) is a California-based developer of eVTOL and eCTOL aircraft that it continues to work toward implementing into commercial air taxi rides in the future. The plans for its network of sustainable aircraft have expanded to cities like New York and Chicago, as well as other countries like Japan and the United Arab Emirates.

In California, south of its headquarters, Archer intends to take to the skies above Los Angeles with a proposed air taxi network announced in August 2024. Building upon that network, Archer shared earlier this year that it had become the exclusive air taxi provider of the 2028 Olympic Games in Los Angeles.

On the other southern coast of the United States, Archer is planning another exciting air taxi network that includes the option of quiet, sustainable air travel around Miami, Fort Lauderdale, and several other key landmarks.

Archer partners up to establish Miami air taxi network

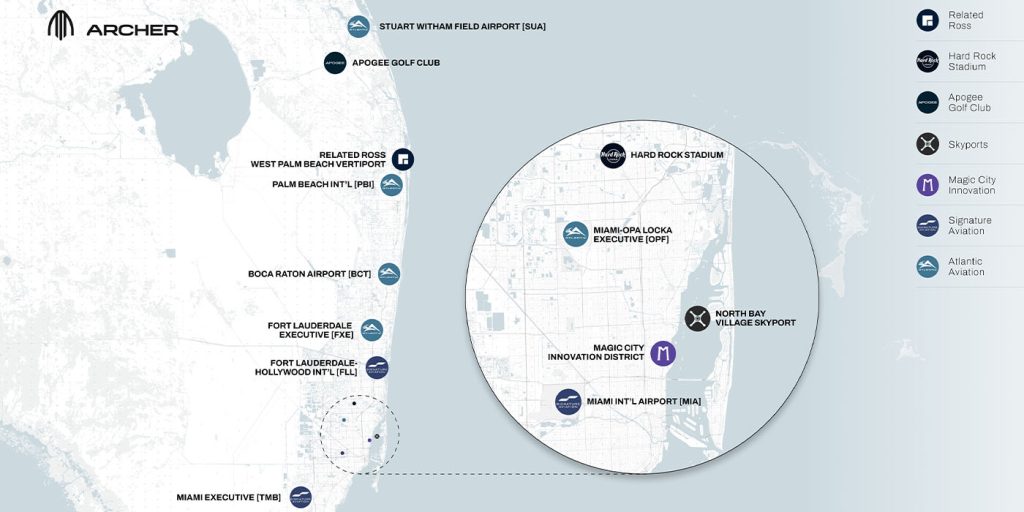

Archer Aviation shared details of its new air taxi network plans for Miami in a press release early this morning. If and when it comes to friuition, the proposed air taxi network will be a result of several new partnerships established by Archer in the Miami metropolitan area.

Some of those partnerships include real estate company Related Ross, Apogee Golf Club, Hard Rock Stadium – where existing heliports will be configured for eVTOLs and/or new air taxi vertiports will be erected. Stephen Ross, CEO and Chairman of Related Ross and Owner of the Miami Dolphins:

Our partnership with Archer marks a pivotal step in expanding South Florida’s regional connectivity through cutting-edge technology. We are integrating Archer’s electric vertical takeoff and landing aircraft into our flagship locations across South Florida, including the Hard Rock Stadium in Miami, Related Ross developments in West Palm Beach, and Apogee Club in Hobe Sound. We’re excited to embrace a forward-thinking vision that transforms how people and businesses move across the region.

According to Archer, the new air taxi network will connect passengers to populated areas around Miami Fort Lauderdale, Boca Raton and West Palm Beach, offering 10 to 20 minute flights. Plans also include easier travel to major airports around Southern Florida, including Miami International Airport (MIA), Fort Lauderdale–Hollywood International Airport (FLL), and Palm Beach International Airport (PBI), plus several general aviation airports. Miami Mayor, Francis Suarez, also spoke:

Miami has never been afraid to bet on the future. We’re a city that attracts visionaries, embraces breakthrough technology, and turns bold ideas into real impact. For years, I’ve worked with Archer as they’ve advanced a vision for an air-taxi network that will elevate Miami’s position as a global capital for innovation and mobility. What they’re building isn’t just transformational transportation, it embodies the Miami mindset: we lead, we innovate, and we redefine what’s possible.

Archer did not share a timeline on when this air taxi network may be operational around Miami, but we’d wager it’s still at least a couple of years away given the need for additional eVTOl development and FAA certifications in order to begin commercial operations in the US.

FTC: We use income earning auto affiliate links. More.

Germany’s largest offshore wind farm hit a big milestone: The first turbine at EnBW’s He Dreiht project has produced its first kilowatt-hour of electricity and sent it into the grid.

More turbines are expected to come online over the coming weeks. European energy provider EnBW has already installed 27 of the wind farm’s 64 turbines, all of which are scheduled to be commissioned by summer 2026.

Peter Heydecker, EnBW board member for Sustainable Generation Infrastructure, described the November 25 milestone as a “significant moment for EnBW.” With 960 megawatts (MW) of total capacity, He Dreiht is now Germany’s largest offshore wind farm.

Vestas supplied the 15 MW turbines, marking their world debut. Nils de Baar, president of Vestas Northern and Central Europe, said the giant turbine’s technology sets a new standard for offshore wind. “Its efficiency and performance enable a significant increase in energy yield per turbine.”

Just one rotation of the 15 MW turbine’s rotor can power the equivalent of four households for a day. The hub stands 142 meters (466 feet) tall, and the rotor’s 236-meter (774-foot) diameter sweeps a 43,742-square-meter (10.8-acre) area — roughly the size of six football fields. To put the scale into perspective, EnBW’s first offshore project, Baltic 1 in 2010, used 2.3 MW turbines.

EnBW wrapped up the wind farm’s internal cabling in August. Those lines connect all the turbines and feed into a converter platform operated by transmission system operator TenneT. That’s where the power is collected, converted from AC to DC, and sent to shore through two high-voltage DC cables.

Once complete, He Dreiht will generate enough electricity to power about 1.1 million households. The project is being built without state funding and sits roughly 85 kilometers (53 miles) northwest of Borkum and 110 kilometers (68 miles) west of Heligoland. EnBW’s offshore office in Hamburg is coordinating the build.

A partner group made up of Allianz Capital Partners, AIP, and Norges Bank Investment Management owns 49.9% of the project. Total investment comes in at around €2.4 billion.

Read more: China’s surge pushes global wind toward fastest growth ever

If you’re looking to replace your old HVAC equipment, it’s always a good idea to get quotes from a few installers. To make sure you’re finding a trusted, reliable HVAC installer near you that offers competitive pricing on heat pumps, check out EnergySage. EnergySage is a free service that makes it easy for you to get a heat pump. They have pre-vetted heat pump installers competing for your business, ensuring you get high quality solutions. Plus, it’s free to use!

Your personalized heat pump quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here. – *ad

FTC: We use income earning auto affiliate links. More.

Environment

BYD tried crushing its $180K luxury SUV with a 2-ton tree and it barely left a mark [Video]

![BYD tried crushing its $180K luxury SUV with a 2-ton tree and it barely left a mark [Video]](https://i0.wp.com/electrek.co/wp-content/uploads/sites/3/2025/07/BYD-ultra-luxury-EV-Europe.jpeg?resize=1200,628&quality=82&strip=all&ssl=1)

The Yangwang U8L is among the most expensive Chinese vehicles, starting at about $180,000. To prove it’s built for just about anything, BYD dropped a 2-ton tree on it, three times, and the ultra-luxury pretty much brushed it off.

BYD drops a tree on its ultra-luxury SUV during testing

BYD launched the Yangwang U8L in September, a long-wheelbase version of the U8 off-road SUV. The U8 was first introduced in September 2023 as the first vehicle from BYD’s ultra-luxury sub-brand, Yangwang.

Yangwang is a new energy vehicle (NEV) brand that sells high-end plug-in hybrids (PHEVs) and 100% battery electric (BEV) vehicles as BYD expands into new segments.

The U8L is Yangwang’s fourth vehicle, following the U8, U9, and U7. It’s available in China with a quad-motor extended-range electric vehicle (EREV) system, delivering a CLTC range of 200 km (124 miles) on battery power alone.

A 2.0-liter turbocharged gasoline engine serves as a generator, delivering a combined CLTC range of 1,160 km (720 miles).

Measuring 5,400 mm in length, 2,049 mm in width, and 1,921 mm in height, the Yangwang U8L is even bigger than the Rolls-Royce Cullinan and Range Rover Long Wheelbase.

BYD’s ultra-luxury SUV is priced from 1.28 million yuan ($180,000), making it one of the most expensive models from a Chinese brand.

It may look pretty, but the Yangwang U8L is built for far more than just good looks. Like the U8, the long-wheelbase version is equipped with advanced features such as emergency float mode, which allows it to float on water for up to 30 minutes, tank turns, crab walking, and more.

To prove its durability, BYD engineers put the luxury SUV through the paces, dropping a massive 2-ton tree on it, not once, but three times.

During the final drop, the company said the maximum impact energy reached 50.4 kJ, or about 37,200 lb-ft. After three consecutive drops, the Yangwang U8L barely even got a scratch. The body structure remained intact, the door still opened, the columns didn’t bend, and the vehicle could even drive like normal.

FTC: We use income earning auto affiliate links. More.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024