Multiple buyers consider purchase and relaunch of ‘irreparable’ FTX

Lawyers handling the FTX bankruptcy case are considering offers that could eventually lead to a relaunch of the troubled exchange.

At an Oct. 24 hearing of the United States Bankruptcy Court in the District of Delaware, Kevin Cofsky of Perella Weinberg Partners revealed he is negotiating with several parties interested in purchasing the company.

Cofsky, an attorney specializing in restructuring and liability management, told Judge John Dorsey that an initial 70 inquiries have been reduced to just three final buyers. But the exact structure of the sale and what kind of exchange might emerge thereafter is unclear.

Any potential relaunch of the company would have to contend with the severe reputational damage done to it. For that reason, industry experts are skeptical that a simple reboot of FTX is even possible.

Debra Nita, senior crypto public relations strategist at YAP Global — an international PR agency specializing in crypto, Web3 and decentralized finance — believes the FTX brand is too far gone to recover.

“The reputation and viability of FTX as a business is likely irreparable at this stage,” Nita told Cointelegraph. “The ability for a brand to recover comes down to several factors, primarily due to the nature and extent of the scandal. Secondary factors include the stability and strength of business operations when it failed, and the kind of response delivered after the initial downfall.”

With millions of customers out of pocket and former CEO Sam Bankman-Fried recently found guilty of seven counts of fraud, the damage to FTX is considerable. Past examples of financial misconduct or carelessness illustrate how difficult it is for exchanges to regain investor trust.

Damaged beyond repair

In January 2019, New Zealand exchange Cryptopia suffered a series of hacks to the tune of $30 million.

Cryptopia was down for two months as its founders formulated a rescue plan. Even as they sifted through the ashes, executives assured customers the damage was minimal. According to Cryptopia, the lost money amounted to a “worst case” of only 9.4% of its total funds.

Through March and April of that year, the exchange carried on, bringing various services back online in a staggered relaunch. By May, it was all over. The damage to Cryptopia’s systems, as well as its reputation, was simply too much to overcome.

Cryptopia is far from an isolated case. Enron, MF Global and Mt. Gox are further examples of companies so utterly compromised by their respective failures that there was never any real hope of rehabilitation.

“Due to the extent of the damage caused, the companies never could recover, regardless of how positively they may have responded after the scandal,” noted Nita.

Miraculous recoveries

On the other hand, there are examples of firms that managed to recover from significant setbacks.

Wells Fargo, an American multinational bank, is one such case. In 2016, the company was embroiled in a significant cross-selling credit card scandal. The bank issued credit cards and other lines of credit to its existing customers without seeking approval.

Executives initially tried to blame middle managers and entry-level workers, but it later transpired that the catalyst for the malpractice was unreasonable expectations of senior management, which created extreme top-down pressure.

Recent: Help or hindrance: Is Web3 really improving mainstream industry and products?

“Following the scandal, they reimbursed affected customers and introduced internal ethics procedures, and their stock price and reputation recovered,” said Nita. “The strength of their business and their responsible responses were then able to see [Wells Fargo] recover in reputation.”

The Consumer Financial Protection Bureau fined Wells Fargo $185 million, and CEO John Stumpf resigned. The company also settled a class-action lawsuit for $575 million.

In the same year as the Wells Fargo scandal, a major crypto exchange suffered a security breach. In August 2016, Bitfinex lost 119,756 Bitcoin (BTC) in a hack worth $72 million at the time. Bitfinex ceased all trading, and the severity of the hack wreaked havoc in the markets, with the price of Bitcoin falling by 20%.

To deal with the matter, Bitfinex decided that all customers would take a 36% haircut. This was applied to all accounts, even those unaffected by the hack. The exchange also issued the Rights Recovery Token, intending to make customers whole.

Bitfinex’s recovery was by no means guaranteed following the hack, but swift (even if unpopular) action on the part of its management helped the exchange weather the storm.

Possible options for an FTX “relaunch”

Cofsky’s testimony highlighted several potential forms a future FTX might take depending on the conditions of the sale.

“We have been engaging in an outreach process with a number of interested parties to either acquire the legacy exchange assets and/or to partner with the debtors in connection with the launch of the exchange. We’ve been evaluating that process relative to the potential to reorganize the assets on a standalone basis.”

“I am optimistic that we will have either a plan for a reorganized exchange, or a partnership agreement, or a stalking horse for a sale on or prior to the December 16th milestone,” said Cofsky.

Not all prospective buyers would want to use the FTX brand despite relaunch discussions. Cofsky clarified that one of the most valuable FTX assets is its list of 9 million customers. One option is to simply sell the list to another exchange and dump the FTX brand entirely.

To make that sale possible, the prospective buyer must know how many FTX customers are unique for any counterparty. Cofsky said that in this instance, the database of FTX information would need to be compared with the counterparty’s database of customers without revealing the identities of anyone on either database.

Cofsky did not make clear how that process would be achieved, but the challenge sounds like a potential use case for zero-knowledge proofs.

A fly in the ointment

Cofsky has stressed the importance of preserving the anonymity of FTX customers, but the position is still being argued in the courts.

Katie Townsend, an attorney representing the Reporters Committee for Freedom of the Press, has argued that the public has a “compelling and legitimate interest” in knowing the names of those affected by the fall of FTX.

Cofsky’s argument has so far persuaded Judge Dorsey that releasing this information would jeopardize the sale, rendering its value close to zero. At each point, Cofsky has been able to extend the length of the anonymity ruling, but the matter is by no means closed.

“The value that would be provided to the estate would be conditioned on the extent to which customers transact on the future exchange or are accessible to others and therefore are not available to that counterparty,” Cofsky testified.

“I would think that the value of the customers to the exchange would remain even after the conclusion of the case,” he added.

Magazine: 6 Questions for Lugui Tillier about Bitcoin, Ordinals, and the future of crypto

In cross-examination, Townsend questioned how Cofsky could be sure that customers would even wish to trade on any future version of FTX.

“I don’t know how we would do that without contacting those customers,” replied Cofsky.

The admission highlights just how complex any sale of FTX really is.

Cautious buyers may even want to split the FTX purchase into a number of payment tranches, with the final value of the spend dependent on their ability to convert the customer database — which will have been inactive for more than a year at the time of any sale — back into active customers.

Given the lessons of history, achieving that goal will be no easy feat.

Politics

Live music venues warn of ‘devastating consequences’ of budget tax changes in letter to Sir Keir Starmer

Tax changes announced in the budget could have “devastating, unintended consequences” on live music venues, including widespread closures and job losses, trade bodies have warned.

The bodies, representing nearly 1,000 live music venues, including grassroots sites as well as arenas such as the OVO Wembley Arena, The O2, and Co-op Live, are calling for an urgent rethink on the chancellor’s changes to the business rates system.

If not, they warn that hundreds of venues could close, ticket prices could increase, and thousands could lose their jobs across the country.

Politics latest: Ex-Olympic swimmer nominated for peerages

Business rates, which are a tax on commercial properties in England and Wales, are calculated through a complex formula of the value of the property, assessed by a government agency every three years. That is then combined with a national “multiplier” set by the Treasury, giving a final cash amount.

The chancellor declared in her budget speech that although she is removing the business rates discount for small hospitality businesses, they would benefit from “permanently lower tax rates”. The burden, she said, would instead be shifted onto large companies with big spaces, such as Amazon.

But both small and large companies have seen the assessed values of their properties shoot up, which more than wipes out any discount on the tax rate for small businesses, and will see the bills of arena spaces increase dramatically.

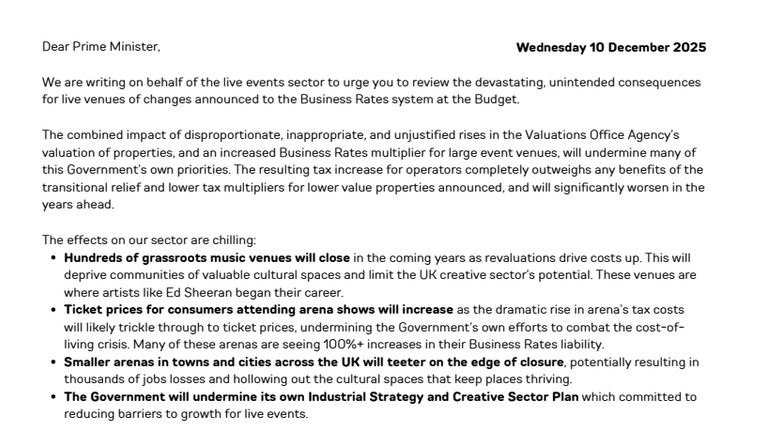

In the letter, coordinated by Live, the trade bodies write that the effect of Rachel Reeves’s changes are “chilling”, saying: “Hundreds of grassroots music venues will close in the coming years as revaluations drive costs up. This will deprive communities of valuable cultural spaces and limit the UK creative sector’s potential. These venues are where artists like Ed Sheeran began their career.

“Ticket prices for consumers attending arena shows will increase as the dramatic rise in arena’s tax costs will likely trickle through to ticket prices, undermining the government’s own efforts to combat the cost of living crisis. Many of these arenas are seeing 100%+ increases in their business rates liability.

“Smaller arenas in towns and cities across the UK will teeter on the edge of closure, potentially resulting in thousands of jobs losses and hollowing out the cultural spaces that keep places thriving.”

The full letter from trade bodies to the prime minister.

They go on to warn that the government will “undermine its own Industrial Strategy and Creative Sector Plan which committed to reducing barriers to growth for live events”, and will also reduce spending in hotels, bars, restaurants and other high street businesses across the country.

To mitigate the impact of the tax changes, they are calling for an immediate 40% discount on business rates for live venues, in line with film studios, as well as “fundamental reform” to the system used to value commercial properties in the UK, and a “rapid inquiry” into how events spaces are valued.

Sky’s Jess Sharp explains how the budget could impact your money

In response, a Treasury spokesperson told Sky News: “With Covid support ending and valuations rising, some music venues may face higher costs – so we have stepped in to cap bills with a £4.3bn support package and by keeping corporation tax at 25% – the lowest rate in the G7.

“For the music sector, we are also relaxing temporary admission rules to cut the cost of bringing in equipment for gigs, providing 40% orchestra tax relief for live concerts, and investing up to £10m to support venues and live music.”

The warning from the live music industry comes after small retail, hospitality and leisure businesses warned of the potential for widespread closures due to the changes to the business rates system.

Sky’s political editor Beth Rigby challenged Prime Minister Sir Keir Starmer on the tax rises in the budget.

Sky News reported after the budget that the increase in business rates over the next three years following vast increases in the assessed values of commercial properties has left small retail, hospitality and leisure businesses questioning whether their businesses will be viable beyond April next year.

Analysis by UK Hospitality, the trade body that represents hospitality businesses, has found that over the next three years, the average pub will pay an extra £12,900 in business rates, even with the transitional arrangements, while an average hotel will see its bill soar by £205,200.

Read more: Hospitality pleads for ‘lifeline’

A Treasury spokesperson said their cap for small businesses will see “a typical independent pub pay around £4,800 less next year than they otherwise would have”.

“This comes on top of cutting licensing costs to help more venues offer pavement drinks and al fresco dining, maintaining our cut to alcohol duty on draught pints, and capping corporation tax,” they added.

The Chancellor Rachel Reeves has acknowledged there were “too many leaks” in the run-up to last month’s budget.

The flow of budget content to news organisations was “very damaging”, Ms Reeves told MPs on the Treasury select committee on Wednesday.

“Leaks are unacceptable. The budget had too much speculation. There were too many leaks, and much of those leaks and speculation were inaccurate, very damaging”, she said.

Money blog: Nine-year-old set up Christmas tree business to pay for university

The cost of UK government borrowing briefly spiked after news reports that income taxes would not rise as first expected and Labour would not break its manifesto pledge.

An inquiry into the leaks from the Treasury to members of the media is to take place. But James Bowler, the Treasury’s top official, who was also giving evidence to MPs, would not say the results of it would be published.

Committee chair Dame Meg Hillier asked if the group of MPs could see the full inquiry.

“I’d have to engage with the people in the inquiry about the views on that”, replied Mr Bowler, permanent secretary to the Treasury.

OBR leak ‘a mistake of such gravity’

The entire contents of the budget ended up being released 40 minutes early via independent forecasters, the Office for Budget Responsibility (OBR).

A report into this error found the OBR had uploaded documents containing their calculations of budget numbers to a link on the watchdog’s website it had mistakenly believed was inaccessible to the public.

Tax rises ruled out

The chancellor ruled out future revenue-raising measures, including applying capital gains tax to primary residences and changing the state pension triple.

Committee member and former chair Dame Harriet Baldwin had noted that the chancellor’s previous statement to the MPs when she said she would not overhaul council tax and look at road pricing, turned out to be inaccurate.

During the budget, an electric vehicle charge per mile was introduced, as was an additional council tax for those with properties worth £2m or more.

Strategy, the largest Bitcoin treasury company, submitted feedback to index company MSCI on Wednesday about the proposed policy change that would exclude digital asset treasury companies holding 50% or more in crypto on their balance sheets from stock market index inclusion.

Digital asset treasury companies are operating companies that can actively adjust their businesses, according to the letter, which cited Strategy’s Bitcoin-backed credit instruments as an example.

The proposed policy change would bias the MSCI against crypto as an asset class, instead of the index company acting as a neutral arbiter, the letter said.

The MSCI does not exclude other types of businesses that invest in a single asset class, including real estate investment trusts (REITs), oil companies and media portfolios, according to Strategy. The letter said:

“Many financial institutions primarily hold certain types of assets and then package and sell derivatives backed by those assets, like residential mortgage-backed securities.”

The letter also said implementing the change “undermines” US President Donald Trump’s goal of making the United States the global leader in crypto. However, critics argue that including crypto treasury companies in global indexes poses several risks.

Related: Strive calls on MSCI to rethink its ‘unworkable’ Bitcoin blacklist

Crypto treasury companies can create systemic risks and spillover effects

Crypto treasury companies exhibit characteristics of investment funds, rather than operating companies that produce goods and services, according to MSCI.

MSCI noted that companies capitalized on cryptocurrencies lack clear and uniform valuation methods, making proper accounting a challenging task and potentially skewing index values.

Strategy held 660,624 BTC on its balance sheet at the time of this writing. The stock has lost over 50% of its value over the last year, according to Yahoo Finance.

Bitcoin (BTC) is also 15% below its value at the beginning of 2025, when it was trading over $109,000, meaning that the underlying asset has outperformed the equity wrapper.

The high volatility of cryptocurrencies may heighten the volatility of the indexes tracking these companies or create correlation risks, where the index performance would mirror crypto market performance, according to a paper from the Federal Reserve.

The “common use” of leverage by crypto traders amplifies volatility and lends to crypto’s fragility as an asset class, the Federal Reserve wrote.

MSCI’s proposed policy change, set to take effect in January, could also prompt treasury companies to divest their crypto holdings to meet the new eligibility criteria for index inclusion, creating additional selling pressure for digital asset markets.

Magazine: The one thing these 6 global crypto hubs all have in common…

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024