UK economy finds reverse gear with surprise decline in October

The UK economy took a surprise tumble in October, according to an early official estimate that showed a contraction of 0.3%.

The Office for National Statistics (ONS) reported that output in all three main divisions – services, manufacturing and construction – was in negative territory.

Economists had expected a flat performance, following on from the 0.2% growth seen in September.

That meagre figure helped the economy to zero growth for the third quarter of the year, easing concerns over the prospect for a recession which is realised if a country records two consecutive quarters of contraction.

Nevertheless, the latest data builds on expectations of a largely flat performance ahead, despite a series of growth measures announced by the chancellor in his autumn statement last month.

Jeremy Hunt said of the ONS figures: “It is inevitable GDP (gross domestic product) will be subdued whilst interest rates are doing their job to bring down inflation.”

Action taken by the Bank of England since December 2021 to tame inflation was intended to hit demand in the economy, helping the pace of price growth ease.

While the rate of inflation has slowed considerably from the figure above 11% seen just over a year ago, prices are still rising but just at a steadier pace.

The effect of interest rate hikes imposed by the Bank has added to borrowing costs, with rising mortgage and rent bills becoming a key plank of the cost of living crisis.

How bad is the UK’s economy?

The Bank warned earlier this month that five million households were yet to feel the home loan hit because their fixed terms had not expired.

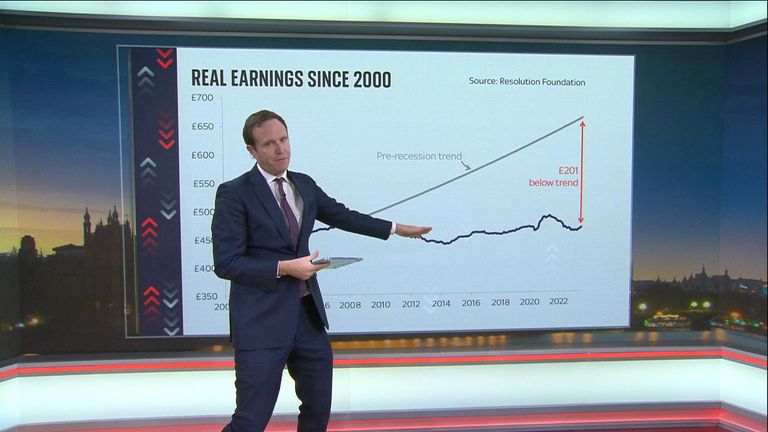

Household spending power has, to some extent, been propped up by a record pace for wage growth but data on Tuesday showed sharp falls in the levels of awards.

Consumers were still, however, enjoying the best real wage growth – when inflation is accounted for – for two years due to the steep easing in the inflation rate in October.

The Bank’s monetary policy committee has seen enough progress in bringing inflation down to have kept Bank rate at 5.25% for two consecutive meetings.

It is due to outline its next rate decision on Thursday, with financial markets and economists widely expecting a further pause.

ONS director of economic statistics, Darren Morgan, said of Wednesday’s data: “Our initial estimates suggest that GDP growth was flat across the last three months.

“Increases in services, led by engineering, film production and education – which recovered from the impact of summer strikes – were offset by falls in both manufacturing and housebuilding.

“October, however, saw contractions across all three main sectors. Services were the biggest driver of the fall with drops in IT, legal firms and film production – which fell back after a couple of strong months.

“These were also compounded by widespread falls in manufacturing and construction, which fell partly due to the poor weather.”

Shadow chancellor Rachel Reeves said: “Rishi Sunak ends the year having failed to deliver on his own promise to grow the economy.

“Economic growth is going backwards leaving working people worse off,” she said.

It’s a debate that has raged since the end of the COVID pandemic but, despite regulatory scrutiny, it’s fair to say there’s been no clear answer to accusations that UK drivers pay over the odds for fuel.

What was once a promotional loss leader for supermarkets desperate for drivers to fill their car boots with groceries, unleaded and diesel costs have been unusually high for years.

Fuel retailers say there is a simple explanation: rising costs being passed on to motorists.

But critics argue there is a reason why the Competition and Markets Authority (CMA) has consistently found that we’re paying more than we should be – and that the disparity between wholesale costs and pump prices has got worse in recent months.

So: who’s right?

What the oil data tells us

Oil prices are well down on levels seen in January (between $75 and $82 a barrel) but fuel prices are clearly not.

In recent weeks, Brent crude has traded in the range of $62 to $64 per barrel and yet drivers are currently, on average, paying £1.37 a litre for petrol and £1.46 for diesel.

The average pumps costs in January stood at £1.39 and £1.45 – despite the significantly higher oil costs seen at the time.

Prices can be affected by all sorts of factors including the value of the pound versus the oil-priced dollar, but that disparity is notable.

Trump’s ambassador tells UK to drill for oil

There is another, emerging, factor to consider

It might surprise you to learn that the UK now has only four operational refineries to produce petrol and diesel after two major sites shut this year.

The decline has sparked an industry warning of a crisis due to high UK carbon charges, imposed by the government, that have made domestic fuel producers uncompetitive versus imports.

The loss of the refinery at Grangemouth this spring has been particularly acute as it left Scotland without domestic production and at the mercy of a more complicated and expensive delivery structure.

Fuel retailers say the impact has been minimal so far, mainly due to remaining UK refineries raising production.

‘Drill baby drill’

The case for the prosecution

Quite simply, fuel price campaigners and motoring groups have long accused the industry of raising its profit margins.

Supermarkets focused price investment elsewhere as the cost of living crisis took hold but the days of Asda (before it was bought by the fuel-focused Issa brothers and private equity) leading a sector-wide fuel price war are long gone.

Reports by both the AA and RAC this week highlight price spikes despite a 5p slump in wholesale costs a fortnight ago.

The AA said: “At the height of the spike, it matched what had been seen in mid June. Then, the petrol pump average reached a maximum of 135.8p by late July.

It said that government data had since shown pump prices at levels not seen since March.

The body questioned the reasons behind that disparity and also pointed towards, what it called, a postcode lottery for pump costs with gaps of up to 9p a litre between towns only 10 miles apart.

The RAC declared on Thursday that pump prices rose at their fastest pace in 18 months during November, with diesel at a 15-month high.

The critics have also included regulators as monitoring of fuel retailers by the CMA since its original market study has consistently found that drivers have been excessively charged.

‘It’s either keep warm or eat’

What’s the fuel industry’s position?

It pleads “not guilty”.

The bodies representing retailers make the point that the CMA and its wider critics fail to take into account huge rises in costs they have faced over the past four years – costs which are being/have been passed on across the economy.

These include those for energy, business rates, minimum wage, employer national insurance costs and record sums arising from forecourt crime.

The Petrol Retailers’ Association (PRA), which represents the majority of forecourts, told Sky News that average margins across the sector are the same today as they were a year ago at between 3% to 4% after costs.

It suggests no fuel for the fire surrounding those profiteering allegations but that rising costs have been passed on in full.

Pic: iStock

What has the regulator done?

The CMA’s road fuel market study committed to monitor the market and recommended a compulsory fuel finder scheme to help bolster competition. That was two-and-a-half years ago.

Limited data has been widely available via motoring apps ahead of the start of the official scheme, expected in spring next year, which will bring real-time pricing into a driver’s view for the first time.

The CMA hopes that by forcing each retailer to divulge their prices in real time, customers will vote with their feet.

In the regulator’s defence

The CMA could argue that government has dragged its heels in implementing its fuel finder recommendation.

While the Conservatives accepted it, Labour is now pushing it through parliament.

The regulator can only act within the powers it has been given. It would say that it can’t threaten or hand out fines until its recommendations are in play and they have been clearly flouted.

What next for the UK economy?

So who’s right?

This is a debate all about transparency but we clearly don’t have a full view on the complicated, and shifting, supply chain which can influence pump prices.

The CMA hopes that postcode lotteries for pump costs will ease once more drivers are aware of the ability to compare and shop around.

But the main reason why this issue remains unresolved is that the CMA’s findings have been incomplete to date.

Its determinations that pump costs have been excessive have all been made without taking retailers’ operating costs into full account.

Pic: Reuters

Why we are closer to an answer

The CMA’s next market update is expected within weeks and will, for the first time, take more extensive cost data into account.

A spokesperson told Sky News: “We recommended the Fuel Finder scheme to help drivers avoid paying more than they should at the pump, and the government intends to launch it by spring 2026.

“The scheme will give drivers real-time price information, helping them find the cheapest fuel and putting pressure on retailers to compete.

“We looked closely at operating costs during our review of the market, and they formed a key part of our final report in 2023.

“As we confirmed in June, we’ve been examining claims that these costs have risen and will set out our assessment in our annual report later this month.”

The hope must be that both sides involved can accept the report’s findings for the first time, to bring this bitter debate to an end once and for all.”

The UK has come a “step closer” to having direct, high-speed rail connections to Germany, the Department for Transport has said.

A partnership between international train operator Eurostar and German national rail company Deutsche Bahn (DB) has “set the foundation” for a fast rail connection between Britain and Europe’s largest economy, the businesses announced on Thursday.

It means the companies are exploring options to offer direct services between London and Cologne and Frankfurt.

Money blog: Major airport increasing drop-off charge

Such direct services would mean reaching Cologne in four hours, and Frankfurt in less than five from the capital city.

At present, rail passengers have to change trains in Brussels to reach those cities. It takes at least five-and-a-half hours to reach Frankfurt, and four-and-a-quarter hours to arrive in Cologne.

Cologne Central Station could soon be served by trains from the UK. Pic: AP

The proposed services would use existing lines and infrastructure. Passengers would board a double-decker Eurostar in London, and be spared a change of trains on the continent.

The ambition to create such links had already been announced, as had a plan to allow direct rail travel from London to Geneva, but the partnership between DB and Eurostar had not.

Will it definitely happen?

Details and technicalities are yet to be worked out, with the German train company highlighting that any services are contingent upon “the necessary technical, operational, and legal prerequisites being met”.

“Implementation by individual railway companies is considered extremely difficult,” DB said.

“Joint partnerships are therefore crucial.”

What about Berlin?

Nothing was announced for a direct service to Berlin on Thursday, despite Transport Secretary Heidi Alexander singling out the benefits and prospect of journeys from London to the German capital in July.

“The Brandenburg Gate, the Berlin Wall and Checkpoint Charlie – in just a matter of years, rail passengers in the UK could be able to visit these iconic sights direct from the comfort of a train, thanks to a direct connection linking London and Berlin,” she said at the time.

A high-speed Eurostar train heading towards France. File pic: PA

Shorter journeys, like those to Frankfurt and Cologne, are seen as more commercially viable than the current 10-hour train journey time to Berlin.

Market studies conducted by Eurostar found travellers are comfortable with international rail journeys of up to six hours.

“Our research indicates that many would choose rail over air for trips within this timeframe,” Eurostar told Sky News. “This, combined with strong business and leisure demand on this route, is why we have prioritised London to Frankfurt.”

Read more from Sky News:

Petrofac administrators eye North Sea sale by Christmas

Submarine hunting pact signed by UK amid Russian threat

The Department for Transport said the focus on the two German cities was a commercial decision by Eurostar and DB, and the UK-Germany rail taskforce, established over the summer, could pave the way for further route announcements.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024