Bitcoin’s 2023 rally drove some of the stock market’s biggest gains this year

Monitors display Coinbase signage during the company’s initial public offering at the Nasdaq MarketSite in New York on April 14, 2021.

Michael Nagle | Bloomberg | Getty Images

For crypto bulls, the most lucrative bets in 2023 were in the stock market.

While bitcoin rallied over 150% for the year, shares of Coinbase, MicroStrategy and the Grayscale Bitcoin Trust, which are all tied closely to the digital currency, did substantially better, rising more than 300% in value. Bitcoin miner Marathon Digital soared 688%.

Not only have those stocks outperformed the primary cryptocurrency, but they’ve been among the biggest gainers across the whole U.S. market. In the universe of publicly traded U.S. businesses with a market value of at least $5 billion, the four bitcoin-tied stocks were among the eight best performers, according to FactSet.

The crypto boom represents a major bounce back from 2022, when coin prices plummeted, taking related equities down with them. A year highlighted by hedge fund collapses, crypto lender failures and crippling losses at miners was punctuated in November 2022, when crypto exchange FTX spiraled into bankruptcy, leading to the arrest of founder Sam Bankman-Fried on fraud charges.

Last month, a jury in New York convicted Bankman-Fried on seven criminal counts, setting the 31-year-old former billionaire up for a possible life behind bars. Weeks later, Changpeng Zhao, founder of crypto exchange Binance, pleaded guilty and stepped down as the company’s CEO as part of a $4.3 billion settlement with the Department of Justice. He faces a possible prison sentence of 18 months or longer.

By the time of Bankman-Fried’s conviction and Zhao’s plea deal, the damage to the broader crypto market had mostly been realized, and investors were looking to the future. One of the biggest drivers for bitcoin this year was an easing of the Federal Reserve’s interest rate hikes, which created a more attractive case for riskier assets.

Prices were also bolstered by the upcoming bitcoin halving, which takes place every four years and is scheduled for May 2024. In the halving process, the reward for mining is cut in half, capping the supply of bitcoin.

Additional buying was sparked by the potential for a flurry of bitcoin exchange-traded funds popping up in the new year.

“It’s just more fuel for a fire,” said Galaxy Digital CEO Michael Novogratz, in an interview on CNBC’s “Squawk Box” last week. “Crypto stocks are trading almost like a mania.”

Bitcoin has climbed to $42,683 as of Tuesday, a massive win for investors who got in at the beginning of the year, when the price was around $16,500. But the leading cryptocurrency is still 38% below its record high of nearly $69,000 in November 2021.

Among companies closely tied to bitcoin and valued at $5 billion or more, the best-performing stock this year was Marathon, a mining firm that just eclipsed that market cap level last week thanks to a 125% surge in December as of Tuesday’s close. On Wednesday, the shares surged another 15%.

Last year at this time, Marathon was hanging on by a thread. The company was in the midst of a quarter that ended with a loss of almost $400 million on sales of just $28.4 million because of tumbling bitcoin prices, a power outage at its facility in Montana and Marathon’s financial exposure to bankrupt miner Compute North.

“It was pretty dire times,” Marathon CEO Fred Thiel said in an interview last week.

Bitcoin mining is an expensive operation because of the high energy costs required to operate the supercomputers. A drop in bitcoin prices means a sharp reduction in the money producers make selling the coins they mine, even as their energy bills get little relief.

Thiel said the company was able to sell equity and was in the fortunate position of not having debt other than a convertible note.

The picture has brightened dramatically in 2023. Last month, Marathon reported third-quarter net income of $64.1 million, as revenue jumped from a year earlier to $97.8 million. Now the company is in expansion mode, and last week announced the purchase of its first two fully owned bitcoin mining sites — one in Texas and one in Nebraska — for $178.6 million.

The acquisitions increased the size of Marathon’s mining portfolio by 56% to 910 megawatts of capacity.

“By vertically integrating, we take the profit margin for the third party out and we can run the site the way we want to run it,” Thiel said. Much of the technology Marathon has been developing, he said, is focused on increased efficiency, “which in an up market people will ignore” because high prices lead to high margins.

Thiel is trying to make sure the company is on sound financial footing the next time there’s a downturn in bitcoin prices. That means bringing down production costs and creating more ways to sell energy back to the grid. He’s also optimistic that through energy harvesting — taking methane gas and converting it to sellable electricity — Marathon will eventually have much more diverse revenue streams.

One of the company’s goals by 2028, Thiel said, is to bring bitcoin mining down to 50% of revenue.

Brian Armstrong, co-founder and chief executive officer of Coinbase Inc., speaks during the Singapore Fintech Festival, in Singapore, Nov. 4, 2022.

Bryan van der Beek | Bloomberg | Getty Images

‘Multiple sources of revenue’

Outside of the mining universe, the best-performing crypto stock in the U.S. this year is Coinbase, which has soared 386% as of Tuesday’s close. It rose 7.7% on Wednesday.

As the only major publicly traded crypto exchange in the U.S., Coinbase has long been a popular way to buy and trade cryptocurrencies in its home market. But with the struggles at Binance, the largest exchange in the world, Coinbase picked up market share during non-U.S. trading hours, according to a report from research firm Kaiko in late November.

Shortly after Zhao’s plea deal, Coinbase CEO Brian Armstrong told CNBC that the news amounted to “a vindication of the long-term strategy that we’ve taken to focus on compliance, make sure we were building a trusted company.”

Coinbase’s revenue and stock price are still way below where they were during the heyday of crypto trading in 2021, when retail investors were jumping into the market to buy all sorts of digital currencies, including gimmicks like Dogecoin. But the business has stabilized following drastic cost-cutting measures starting last year and extending into early 2023.

Coinbase also offers investors a bit of diversity outside of bitcoin. In the third quarter, bitcoin accounted for only 37% of transaction revenue at Coinbase, while ethereum made up 18% and other crypto assets amounted to 46%. Additionally, the combination of interest income and stablecoin revenue (earned through USDC reserves) more than doubled in the latest quarter to $212 million due to higher interest rates.

Transaction revenue now accounts for less than half of Coinbase’s net revenue, down from 96% at the time of the company’s public market debut in 2021.

“We made a big effort around the time we went public to start diversifying our revenue,” Armstrong said in an interview last week with CNBC. “Now we have multiple sources of revenue, some of them in a high interest rate environment go up, some of them in a low interest environment go up. That means revenue has started to become more predictable.”

The other top stock performers in crypto are much more closely tied to bitcoin.

The Grayscale Bitcoin Trust is up 330% this year. GBTC hit the over-the-counter market in 2015 as the first publicly traded bitcoin fund in the U.S., offering investors a way to passively own bitcoin. The challenge for investors in the past has been that GBTC is a closed-end fund, which makes it less liquid than an ETF.

Late last year, in the darkest days of crypto, GBTC’s discount to its net asset value approached 50%, meaning its market cap was about half the value of the bitcoin it owned. As of Dec. 22, that discount had narrowed to 5.6%, the lowest since early 2021. The fund currently owns about $26.6 billion worth of bitcoin and has a market cap of $24.7 billion.

In addition to the rally in bitcoin this year, GBTC is getting a boost from the prospects that it will get regulatory clearance next year to convert to an ETF, a move that would allow it to trade through a traditional stock exchange and gain liquidity measures that would bring its market value more in alignment with its NAV.

Grayscale said in a regulatory filing Tuesday that Barry Silbert, CEO of parent company Digital Currency Group, is resigning as chairman of Grayscale Investments and exiting the board, effective Jan. 1. No reason for his departure was provided. He’s being succeeded as chairman by Mark Shifke, DCG’s finance chief.

Big investors join the party

The Securities and Exchange Commission met with Grayscale in November and has been formally engaging with other asset managers about the issuance of bitcoin ETFs.

Those meetings began after an appeals court sided in August with Grayscale in a lawsuit against the regulator, which had opposed the firm’s efforts on concern that investors would lack sufficient protections. Other large money managers, such as BlackRock, Fidelity Investments and Invesco, have taken steps to create their own funds.

Grayscale CEO Michael Sonnenshein told CNBC’s “Squawk Box” last week that the “hopeful approval” for ETFs will bring in new participants, most notably investment advisors who oversee roughly $30 trillion in the U.S. but have restrictions on what they can buy.

“When my team had our court victory, I think that certainly unlocked a lot of optimism amongst investors about GBTC and the prospects for it to uplist as a spot bitcoin ETF,” Sonnenshein said. “As we turn the corner into the new year, I know there’s a lot of focus on that from the investment community.”

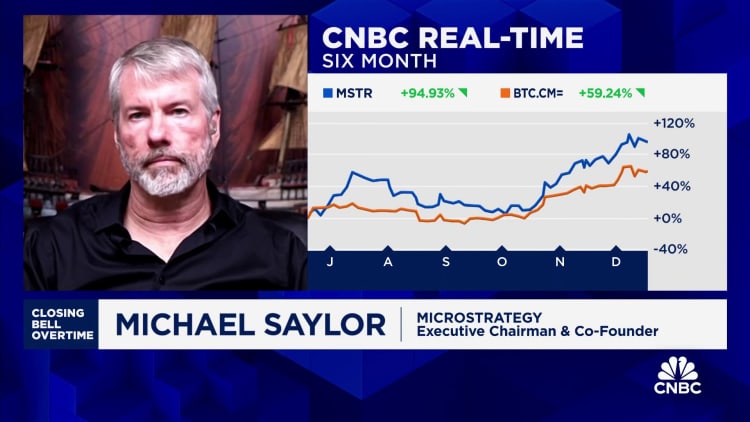

In the absence of an accessible ETF to date, many investors have flocked to MicroStrategy as a way to buy bitcoin.

Founded in 1989 as a business intelligence software company, MicroStrategy now gets the vast majority of its value from the 174,530 bitcoins it owned as of the end of November, currently worth $7.4 billion. The stock’s 327% jump this year has lifted the company’s market cap to $8.3 billion. Its software and services business generated about $130 million in sales in the third quarter.

The company said in a regulatory filing on Wednesday that it purchased an addition 14,620 bitcoins from Nov. 30 to Dec. 26 for $615.7 million, bringing its total to 189,150 bitcoins. The stock jumped 11%.

MicroStrategy announced its plan to invest in bitcoin in mid-2020, disclosing in an earnings call that it would commit $250 million over the next 12 months to “one or more alternative assets,” which could include digital currencies like bitcoin. At the time, the company’s market cap was about $1.1 billion.

In the third quarter of 2020, MicroStrategy acquired 38,250 bitcoins for a total of $425 million.

Phong Le, who was elevated to CEO from CFO last year, said on the October 2020 earnings call that MicroStrategy’s investment in bitcoin allowed it to “tap into the passion of the broader crypto market,” adding that, “We’ve seen a notable and unexpected benefit from our investment in bitcoin in elevating the profile of the company.”

Since then, MicroStrategy has come to be known as a bitcoin proxy. Co-founder and ex-CEO Michael Saylor is one of the cryptocurrency’s principal evangelists, even co-authoring a book on the subject last year called “What is Money?”

“The one thing that we can count on is that bitcoin goes forward in the year 2024 and a strategy built around bitcoin is generally a pretty safe one for institutions,” Saylor said in an interview Dec. 18 on CNBC’s “Closing Bell.” “Education makes a difference. Institutional adoption makes a difference. The spot ETF news is good news. Loosening of monetary policy is good news.”

Saylor is also optimistic about a mark-to-market accounting rule set to go into effect in 2025 (though companies can choose to adopt it earlier) that changes how companies record crypto assets. Instead of being classified as intangible assets that have to be marked down if the value drops below the purchase price, crypto will be in a separate category and companies will mark it up or down based on where it’s trading.

Saylor says the new measure provides an incentive for companies with billions of dollars of cash sitting on their balance sheets to put some of that money to work in bitcoin.

As good of a year as it’s been for the bitcoin bulls, it’s been equally painful for the bears.

Short sellers, or investors who bet on a drop in stock prices, have lost a combined $6.3 billion on their positions against Coinbase, MicroStrategy and Marathon, according to data supplied by S3 Partners last week. In the first three quarters of the year, crypto shorts spent $2.19 billion buying the stocks to reduce their exposure, the firm said.

There’s still a hefty dose of skepticism. More than 23% of Marathon’s shares available for trading are sold short, while MicroStrategy’s short interest-to-float ratio is about 21% and Coinbase’s sits at 14%. The average among U.S. stocks is 5%, according to S3.

Dimon vs. the evangelists

But risk remains for the bitcoin believers.

While enthusiasts like Saylor are betting on the long-term appreciation of the asset as a hedge against inflation and as a store of value, new investors are jumping into a historically volatile market.

When bitcoin fell by more than 60% in 2022, Coinbase, GBTC and MicroStrategy each dropped by at least 74%. Marathon lost 90% of its value and some of its peers went out of business.

Even with a more stable environment in 2023, crypto still has high-profile detractors like JPMorgan Chase CEO Jamie Dimon, who told the Senate Banking Committee earlier this month that, “The only true use case for it is criminals, drug traffickers … money laundering, tax avoidance.”

“If I was the government, I’d close it down,” he said.

But that prospect is looking less likely than ever as more institutional money flows into bitcoin as an investment vehicle. In mid-December, analysts at BTIG lifted their price target on MicroStrategy to $690 from $560, citing improving sentiment and the approaching bitcoin halving.

“Our expectation is that the approval of a spot BTC ETF would increase regulatory clarity around bitcoin, which should give large institutional investors, such as insurance companies, greater comfort investing in bitcoin,” the analysts wrote.

Galaxy Digital’s Novogratz says that “broadly we’re still in bull market phase,” noting that there’s a constant and inherent scarcity of bitcoin supply. Novogratz expects bitcoin to eclipse its record high next year, and says that among respected investors, “I can give you 50 of them on the other side of the table from Jamie Dimon.”

In the near term, Novogratz cautions that with so much momentum coming from crypto traders, the tide could turn and cause a correction.

“I’m a little nervous because it feels so good,” he said.

— CNBC’s MacKenzie Sigalos contributed to this report

WATCH: The crypto market is going to ‘rally further, research firm says

Technology

AI was behind over 50,000 layoffs in 2025 — here are the top firms to cite it for job cuts

Josh Woodward, VP of Google Labs, addresses the crowd during Google’s annual I/O developers conference in Mountain View, California on May 20, 2025.

Camille Cohen | AFP | Getty Images

Josh Woodward may not be a household name in Silicon Valley. But inside Google, everybody knows about him.

The 42-year-old Oklahoma native, who started at Google by way of a product management internship in 2009, has spent the past eight months running the Gemini app, the centerpiece of the search giant’s artificial intelligence strategy.

Heading into 2026, Woodward’s work is more critical than ever as Google rushes to keep pace with its high-powered AI rivals, namely OpenAI, which kickstarted the generative AI boom with the launch of ChatGPT just over three years ago.

As industry experts forecast a shift in consumer behavior from traditional search to AI-powered apps, Google is fighting to make sure users stay within its ecosystem, whether it’s for chatbot services, images, videos or online shopping. Woodward is helping to spearhead that effort while also keeping his job as head of Google Labs, home to the company’s experimental AI projects.

Clay Bavor, former co-lead of Google Labs, said Woodward’s ability to move fast, break down barriers and execute “has landed him right at the center of the most important work at Google.”

CNBC spoke with more than a dozen people who have worked with Woodward about his evolving profile at Google, how he got there and the pressure he faces to help Google stay ahead of the competition without losing the trust of users. Several current and former colleagues, including some who asked not to be named because they weren’t authorized to speak to the press, emphasized how seriously Woodward takes the societal concerns that come with the power of AI, and about Google’s role in shaping the future.

In April, when Woodward was promoted to run the Gemini app, Google’s position in AI was tenuous. Alphabet shares plunged 18% in the first quarter, their worst performance for any period since 2022, and concerns were building that the company was losing its long-held position as the internet’s front door.

Demis Hassabis, co-founder of Google DeepMind and the person considered the top AI executive at Google, said in the memo announcing the move that Woodward would be focused on the “next evolution” of the app, according to a Semafor report.

A major turning point for Woodward’s group came in late August, with the launch of image generator Nano Banana, a Gemini feature that lets users blend multiple photos together to create personal digitized figurines.

Within days, Nano Banana had become so popular it was overloading the company’s infrastructure, forcing Google to place temporary limits on usage to ease the burden on its custom-designed chips called tensor processing units.

“Our TPUs almost melted,” said Amin Vahdat, Google’s head of AI infrastructure, at a November all-hands meeting, according to audio reviewed by CNBC.

By the end of September, the Gemini app surpassed 5 billion images and dethroned OpenAI’s ChatGPT at the top of Apple’s App Store. Nano Banana is now being rolled into other products like Google Lens and Circle to Search.

Like its top rivals, Alphabet is pouring money into AI infrastructure ahead of an expected surge of new business. The company said in its earnings report in October that capital expenditures for the full year would reach between $91 billion and $93 billion, up from a prior forecast of $85 billion.

Alphabet vs. Meta in 2025

Wall Street’s mood on the company has reversed dramatically.

Despite a brutal first quarter, Alphabet’s stock is up 62% this year, outperforming all of its megacap peers including Meta, which is up 13%.

Google said in October that the Gemini app’s monthly active users swelled to 650 million from 350 million in March. AI Overviews, which uses generative AI to summarize answers to queries, has 2 billion monthly users. OpenAI said in October that ChatGPT hit 800 million users per week.

Last month, Google introduced Gemini 3, its latest model, prompting excitement across much of the tech sector.

“I’ve never had more fun than right now,” Woodward told CNBC’s Deirdre Bosa in an interview soon after the release. “It’s partly the pace. It’s partly the abilities these models give to people who can imagine use cases and products.”

Bavor, who’s now co-founder of AI agent startup Sierra, said Woodward “was among the very earliest people in the company to see the potential in large language models for building products,” and lauded his ability to “get his mind fully around a new technology, to see around corners, to see how it might evolve and how it might be used.”

‘Change for good or bad’

Woodward now faces the challenge of not only leading two units within Google but also finding a balance between moving fast to compete with AI rivals OpenAI and Anthropic and not moving so fast that the search company’s AI products enable potential harm.

It’s a pressing issue as AI rapidly bleeds into daily life, more slop populates social media, and an onslaught of AI-generated content makes it difficult for average consumers to distinguish fact from fiction.

Woodward discussed the theme in a podcast with partners from venture firm Sequoia in March, shortly before taking over the Gemini app. AI-generated videos were rapidly getting more advanced, following the launch of OpenAI’s Sora in late 2024.

“When I’m thinking of video, for example, I’m on the side of wanting to amplify human creativity, but there are these moments that happen in our valley here where things change,” Woodward said. “And they change often for generations. And they can change for good or bad.”

The Nano Banana Pro, released in November, is so advanced that its creations blur the lines between images that are clearly AI generated and those that are real. The product has faced criticism for depicting white women surrounded by Black children in responding to a prompt about humanitarian aid in Africa.

The intensity of the job is hardly reflected in Woodward’s persona. Colleagues harp on his disarming, goofy laugh that often comes out mid-conversation and a friendliness stemming from his Midwestern upbringing.

Caesar Sengupta, who worked with Woodward on one of his earliest projects at Google, said, “I’ve never seen him get angry with anyone.” Sengupta, who’s now founder of AI finance platform Arta, added that he used to tease Woodward, suggesting he would be Google’s next CEO.

Clay Bavor, VP of Virtual Reality for Google, introduces the Daydream View VR headset during the presentation of new Google hardware in San Francisco, California, U.S. October 4, 2016.

Beck Diefenbach | Reuters

Woodward joined Google Labs in 2022. Bavor said Woodward was his first choice to help lead the effort.

One of the team’s first breakout products was known as Project Tailwind, an AI notebook that senior product manager Raiza Martin thought up in her 20% time, Google’s longstanding practice of letting employees dedicate one day a week to a project of personal interest.

Woodward helped shepherd the project through several iterations to what morphed into NotebookLM, a popular product that analyze articles, PDFs or videos a user uploads, and provides summaries or offers insights. Martin stayed on as a senior product manager until December 2024, when she left to co-found AI startup Huxe.

To help build NotebookLM, Woodward turned to an unsuspecting hire.

Steven Johnson had never had a full-time boss and had no connection to Google. Living in New York, he’d spent his career up to that point as an author, writing books about the history of science and technology.

Woodward was an admirer of his work.

“We hatched plans for him to join us as a visiting scholar,” Bavor said.

Johnson joined on a part-time basis in 2022. When he went full time in May 2023, Woodward put him to work immediately.

With Google’s annual I/O developer conference a week away, Woodward had the idea to demo an audio feature for what would become NotebookLM, viewing it as a way to test the evolving capabilities of Google’s AI models. The group worked overtime to get it done in time for Woodward’s presentation.

Leading up to the event, Martin wanted to collect user feedback on communication app Discord even though Google preferred that staffers use homegrown products for such efforts. Woodward intervened to make sure Martin could keep using Discord, employees told CNBC.

“In true Google fashion, everyone was like ‘What is Discord?'” Martin said in October 2024, on Lenny’s Podcast, hosted by tech investor and researcher Lenny Rachitsky. She recalled being asked by Google administration, “Why not use Google Meet, why not Google Groups, why not this and that, and I was like, ‘The server is the way to go.'”

Johnson, who spoke with CNBC on a video call, said Woodward’s approach was, “Let them cook.” The discord server now has more than 200,000 members, a company spokesperson told CNBC.

The screen displays the inscription ”NotebookLM” during a meeting between Alphabet and Google CEO Sundar Pichai and Polish Prime Minister Donald Tusk at Google for Startups in Warsaw, Poland, on Feb. 13, 2025.

Klaudia Radecka | Nurphoto | Getty Images

At I/O, Woodward took the stage after Google Cloud CEO Thomas Kurian’s keynote. He opened by talking about Project Tailwind, a concept that “five engineers at Google put together over the last few weeks.”

“We’ve been developing this idea with authors like Steven Johnson and testing it at universities like University of Oklahoma, where I went to school,” said Woodward, as he walked across the stage to a laptop. “You want to see how it works?”

He began his demo, uploading documents into the app. In a side panel, Tailwind instantly began showing key concepts and questions based on the materials in each document. He hovered his mouse over a button that said citations, saying “My favorite part is it shows its work.”

NotebookLM was initially released in July 2023, followed by a broader rollout in the ensuing months. It was an instant hit, and has since been updated to include podcasting, audio and video features.

Recommended reading

Woodward graduated from Oklahoma with an economics degree in 2006, and then headed to graduate school at University of Oxford in the U.K., where he studied the effects of the U.S. military and economic foreign aid on democracy.

He kicked off his career at Google in 2009 with a product management internship, and went on to hold a number of product management roles.

When Sengupta was tapped by CEO Sundar Pichai to start the Next Billion Users (NBU) project, an initiative to understand users in emerging markets like India, Woodward was “one of the first people I asked to join,” he told CNBC.

At NBU, Woodward wrote a weekly newsletter that was concise and thought-provoking, and became so popular that people would email the author asking to be added to the newsletter, Sengupta said.

Woodward still writes a newsletter — now it’s quarterly — about matters of interest to him and what he’s been reading. Woodward reads so much that he’s often the first person Google executives go to for book recommendations, colleagues said.

He also assigns reading. Martin said on the podcast last year that Woodward had given her an article to read that dissected whether users should trust AI chatbots.

One of Woodward’s best-known attributes, employees said, is his ability to circumvent Google’s massive bureaucracy. He helped set up a system called “block,” where workers can file a note if they see a perceived roadblock, and a team within Labs will handle it, they said. When NotebookLM launched, the product needed more TPUs, and Woodward was able to get them.

“It’s been very cool that we have someone who can take care of the annoying stuff, and we’re able to just get to the users,” said Usama Bin Shafqat, a Google Labs software engineer.

Woodward also came up with a process called “Papercuts” to address minor issues that create friction in a particular product. In October, Woodward posted on X, “Papercut fixed: You can now change models mid-conversations on GeminiApp without having to start over.” The post got more than 100 replies, including many from users thanking him.

Woodward is known for responding directly to users on X and Reddit, and brings feedback to employees so they can address complaints, said Jason Spielman, a former designer at NotebookLM.

“It’s that level of commitment to the end user I hadn’t seen in other leaders,” said Spielman, who left Google in January to join Martin at Huxe.

At a Google all-hands meeting last December, Woodward took the microphone as the Zombie Nation song “Kernkraft 400” blared in the background.

“I’m going to try to do six demos in eight minutes,” Woodward told the audience, according to audio obtained by CNBC.

He started with Jules, a coding assistant. He showed off NotebookLM, which had received several updates. He then moved to Project Mariner, an AI-powered multitasking Chrome extension, and demoed AI video generator Veo and experimental AI tool Whisk. He also showed project Maya, an image generation tool built in collaboration with the Google Shopping team.

Attendees erupted in applause after seeing all of the demos work in real time.

Ahead of last year’s I/O event, Woodward suggested Google host a second show tailored to staffers, according to two employees.

Pichai quickly greenlit the proposal and dispatched Woodward’s Labs teams to make it a reality. The result was Demo Slam, where employees showed off rapid demos to an audience of their peers, who could also try the products. It was such a hit that Google hosted a second Demo Slam in May, the same week as I/O.

Expectations are high for Woodward, and Google broadly, to continue delivering new AI features in 2026. But with 2025 wrapping up, Pichai sees the company riding high.

“The momentum has been incredible to see,” Pichai said at a recent all-hands meeting. “We’ve been shipping at a pretty fast pace across the company”

WATCH: Battle of the chatbots

Medianews Group/boston Herald Via Getty Images | Medianews Group | Getty Images

Los Angeles resident Ruth Horne, 76, enticed by a bargain, bought what she thought was a Roomba to vacuum her house, but the experience ended in frustration.

“It kept getting stuck somewhere and would then just go around in circles,” Horne said. She realized it was a cheaper knock-off.

Meanwhile, Marcy Lewis, 75, of Madeira, Ohio, had been wanting a robot vacuum cleaner and deliberately chose a knock-off.

“I’m pretty low tech, but it just seemed like a good idea — cleaner house, less work,” Lewis said.

She was watching Prime Day sales and got a good deal on a Eufy robot vacuum cleaner. “I really liked it and it did a good job, but didn’t last long,” Lewis said.

Product quality was one of the advantages for the Roomba in a flood of less expensive knock-offs, but that didn’t save it from the corporate bankruptcy its maker iRobot announced earlier this week. And cheap Chinese competition was not the only factor in its failure. An attempted 2022 acquisition of iRobot by Amazon, thwarted by regulators, and the changing dynamics around mergers and acquisitions, represent an ongoing concern for struggling tech companies that in the past have turned to M&A as not just an exit ramp, but savior.

The company, which Amazon agreed to pay $1.7 billion to acquire in August 2022, reported in a court filing last Sunday that it had between $100 million-$500 million in assets and liabilities, and owed roughly $100 million to its largest creditor, Shenzhen Picea Robotics Co., the contract manufacturer, located in China and Vietnam, which now owns it. In all, Reuters reported the company has $190 million in debt.

“Today’s outcome is profoundly disappointing — and it was avoidable,” Colin Angle, co-founder and CEO of iRobot, told CNBC in a statement earlier this week. “This is nothing short of a tragedy for consumers, the robotics industry and America’s innovation economy.”

In early 2024, Amazon CEO Andy Jassy told CNBC that regulators’ efforts to block the deal were a “sad story” and said it would’ve given iRobot a competitive boost against rivals.

Some M&A experts agree with the view of both the would-be acquirer and bankrupt company.

“The iRobot case demonstrates that when regulators prioritize hypothetical future harms over present-day financial realities, they don’t protect competition; they destroy the target company,” said Kristina Minnick is a professor of finance at Bentley University. “The bankruptcy of iRobot serves as a definitive cautionary tale for the current M&A environment, underscoring fears that regulators are dismantling the traditional safety net for struggling companies,” she said.

Acquisitions are an integral part of recycling assets and growing the economy, but regulators in the U.S. and in Europe have taken a stance in recent years which Minnick says “distorts this natural cycle.”

She added that by blocking Amazon’s white knight acquisition of iRobot, regulators removed the only viable exit ramp for a struggling American robotics pioneer.

“The tragic irony is that instead of remaining an independent competitor, iRobot was forced into bankruptcy and is now being sold to one of its Chinese manufacturing partners. In their zeal to prevent Big

Tech expansion, regulators effectively handed valuable IP and market share to the very foreign competitors that were crushing the company in the first place,” Minnick said.

After Amazon abandoned the deal in early 2024 citing the likelihood that European regulators would block it, newer issues emerged for the already vulnerable company.

“Roomba didn’t just run out of battery, it got shoved into Chapter 11 after European regulators kicked out Amazon’s $1.4 billion escape hatch and left it bleeding cash on the living-room floor,” said Eric Schiffer, chairman at Reputation Management Consultants. “Amazon walked, tariffs hit, cheap rivals swarmed, and suddenly the king of robo-vacs is begging its own manufacturer to save its plastic rear end,” Schiffer said. “This is a cautionary tale that if your business model is to get bought by Big Tech, one hostile regulator in Europe can turn your dream exit into a Caligula-level catastrophic implosion.”

Jay Jung, managing partner at Embarc Advisors, a San Francisco-based corporate finance advisory firm, says that iRobot’s bankruptcy is ominous for future similar deals if regulators don’t learn the lessons of the past few years. “European regulators are within their rights to block these deals,” he said. But he added that “their stance is too tilted towards anti-big tech. When a Chinese company like this takes over, they will preserve the brand but everything moves to China — lost jobs, and any other economic benefit other than the brand is gone.”

At least publicly, the Trump administration’s Federal Trade Commission seems to be taking a more hands-off approach to M&A than its Biden era predecessors led by FTC Chair Lina Khan, who had a hawkish antitrust stance. It has vowed to take a dual approach on mergers: vigorously pursue ones deemed anti-competitive and stand out of the way one of ones that don’t meet that criteria. “If we’ve got a merger or conduct that violates the antitrust laws, and I think I can prove it in court, I’m going to take you to court. And if we don’t, I’m going to get the hell out of the way,” FTC Chair Andrew Ferguson told CNBC’s Squawk Box earlier this year.

But in Europe, the view towards tech M&A remains tilted to scrutiny. EU antitrust chief Teresa Ribera telegraphed that there could be more to come in comments earlier this month when announcing an anti-trust probe against Meta’s plans to block AI rivals from Whatsapp, which it owns. The action she said was to prevent dominant tech players from “abusing their power to crowd out innovative competitors”

That is cold comfort for a struggling tech company, and Minnick said big tech is already finding workarounds to avoid antitrust scrutiny. As a direct result of these blocked exit ramps, the tech giants are now attempting to circumvent regulators through asset purchases rather than full company acquisitions.

“In deals like Microsoft’s arrangement with Inflection AI or Amazon’s deal with Adept, the acquirer hires the target’s founders and key engineering talent while licensing their intellectual property, leaving the corporate shell behind,” Minnick said, adding that this “reverse acqui-hire” structure is designed specifically as a loophole to bypass antitrust review.

The FTC did in fact issue a report on these types of deals in the final days of Lina Khan’s tenure, after it had targeted the Amazon-Adept deal for scrutiny.

Minnick says even if the deal tweaks are successful, they remain imperfect solutions for a broader M&A problem. “While this allows the technology to survive, it is a sub-optimal outcome that often leaves regular shareholders and non-essential employees stranded in a hollowed-out zombie company, proving that regulatory friction is forcing the market into increasingly complex and inefficient contortions to survive,” she said.

The iRobot headquarters in Bedford, Massachusetts, US, on Friday, June 16, 2023.

Bloomberg | Bloomberg | Getty Images

Minnick believes that if things don’t change, we are likely to see more of these zombie scenarios, where struggling tech and media companies find their exit ramps blocked by regulators overseas or at home. “The refusal to allow organic consolidation means that instead of orderly acquisitions that preserve jobs and innovation, we may see more disorderly bankruptcies,” Minnick said. “If potential acquirers are genuinely concerned about overpaying or regulatory hurdles, they will choose not to engage. But when regulators preemptively block these lifelines to make a philosophical point, they are not saving the market; instead, they are breaking the machinery that allows the economy to heal and grow,” she added.

Roomba did face more than just M&A headwinds, including financial problems accelerated by the Trump administration’s trade policy.

Ragini Bhalla, head of brand at Creditsafe, has been watching iRobot’s deteriorating finances for a while. The company began paying vendors three to four weeks late beginning in May, Bhalla said, and that volatility in paying vendors and suppliers is usually an early warning sign of emerging liquidity pressure. She also said that iRobot’s credit score steadily dropped over a period of five months until it was rated “Very High Risk” in June 2025, where it stayed until the bankruptcy filing.

Bhalla also noted that revenue declined amid intensifying competition from lower-priced Chinese rivals and that tariffs emerged as a direct and material accelerant. Trade policy was the final blow. “Most Roombas are manufactured in Vietnam, exposing iRobot to new U.S. import levies that added millions in costs and disrupted forward planning,” Bhalla said.

Ultimately, the combination of elevated debt, eroding demand, and tariff-driven cost pressure pushed iRobot into a manufacturer-led buyout through bankruptcy. “This illustrates how trade policy shocks can quickly turn underlying operational stress into a solvency event for hardware-dependent businesses,” Bhalla said.

There is no going back from an antitrust regime that has gone global, according to Schiffer, and Roomba may merely be the most high-profile casualty of 2025.

“Your suitor can live in Seattle, your stock on Nasdaq, and some wacky commission in Brussels holds the shotgun to your wedding,” Schiffer said, adding that for founders, “Roomba is the billboard warning that if you rely on one mega-deal to save you, you’re not running a strategy, you’re rehearsing for disaster.”

Meanwhile, Lewis in Ohio just wants a working Roomba.

“I am surprised about the bankruptcy, but I don’t feel that it affects me. I’m also disappointed that a Chinese company is buying Roomba — sadly that seems to be the way things go now. It’s nice to buy American, but it gets harder and harder.”

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024