Interest rate hikes ‘net positive’ for economy but not everyone

Here’s a sentence which might sound a little odd: higher interest rates have been good news for the UK economy.

For the first time in many decades, the pain faced by borrowers from higher interest rates has been more than balanced out by the benefit experienced by savers from those interest rates.

If this sounds a little odd it’s partly because invariably, when people – the media, politicians and economists – talk about interest rates they focus unduly on one side of the equation: the plight of the borrower. And there’s an understandable reason for that: in previous “hiking cycles”, when the Bank of England raises interest rates, that pain has invariably outweighed the windfall.

Money latest: Mortgage price war ‘likely’ as 3% interest rates predicted

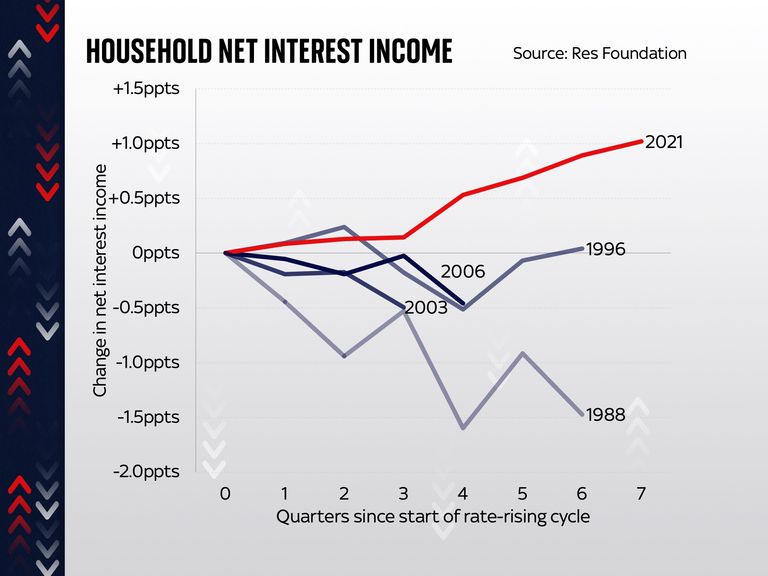

That was the case when borrowing rates were lifted in 1988; it was the case in 1996, in 2003 and in 2006.

In each case the overall impact, across the economy, on households’ balance sheets was negative.

But not so this time around.

According to the Resolution Foundation, the net income we’ve earned, across the economy, as a result of interest rates, has actually risen rather than fallen – up by a percentage point since rates started going up.

To put that into perspective, the “interest rate effect” on incomes in the late 1980s was -1.5 percentage points.

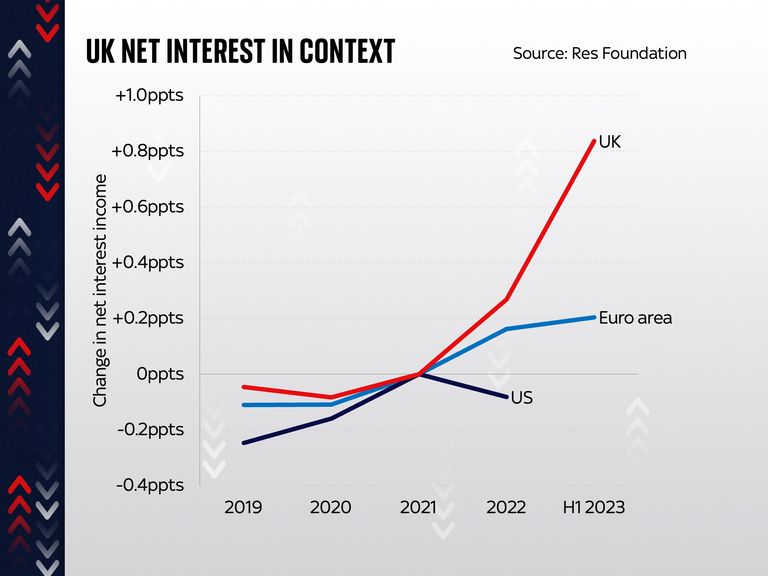

And what’s striking, when you compare the UK to the euro area and the US, is that we are a bit of an outlier: the interest rate effect, across the economy, was much more positive than it was in those two other areas.

This, says the Resolution Foundation, is at least part of the explanation for how the UK hasn’t yet slipped into the recession a lot of people anticipated this time last year.

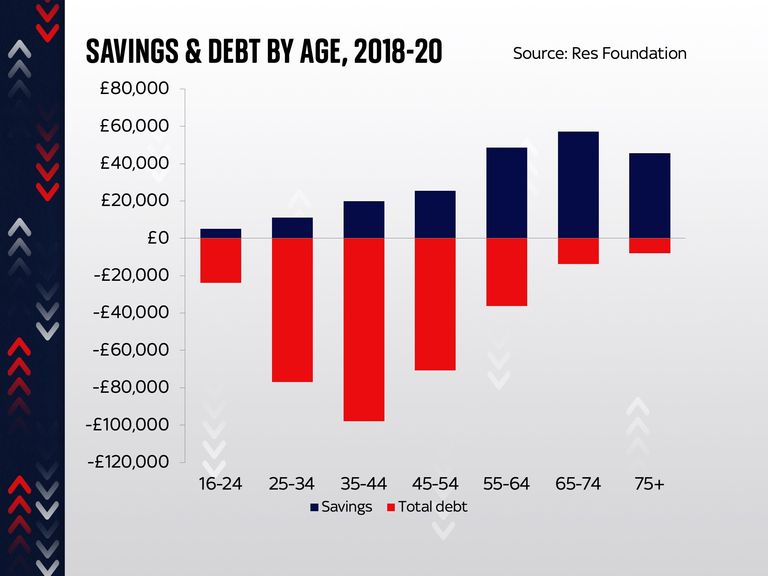

Part of the explanation for this is that it so happened, in large part because of the pandemic lockdowns, that people began this hiking cycle with a lot of savings in their bank accounts – far more than usual.

Read more:

Mortgage approvals up as more lenders cut rates

First-time buyers fall to ‘lowest level in a decade’

FTSE 100 bosses ‘earn typical UK annual salary in three days’

The upshot was that, across the economy, the benefit from those savings (and savings rates went up very quickly – albeit not to the levels of borrowing rates) was greater than the impact on mortgages and loans. Another part of the explanation is that so far only around half of those with fixed-rate mortgages have re-fixed their loans.

But there are a few very important provisos here. The first and perhaps most important is that while the above is certainly true across the whole economy, there’s a dramatic difference of experience for different categories of people.

Those whose debts outweigh their savings (which in this case mostly means younger people) will certainly see a negative impact from higher rates. Those with far more savings than debts – the older segments of the population – will see a benefit. In other words, the pain and the dividends are not being equally shared out. The old are doing much better; the young are doing worse.

And there are two other provisos. The first is that this positive impact will begin to wear off as more and more people re-fix their mortgages and go up from low-interest rates to higher rates. Even though the typical fixed-rate deal has been coming down recently, it’s still far higher than it was two or five years ago.

Click to subscribe to The Ian King Business Podcast wherever you get your podcasts

The final proviso is that none of the above takes into account the broader impact of the cost of living crisis.

Everyone is having to pay higher prices for nearly everything. And while the annual rate at which those prices are increasing (inflation) has decelerated, the level of prices remains more than 15% above where it was a couple of years ago.

That’s a painful adjustment for everyone. The good news is that the impact of rates – across the economy as a whole – has actually been positive rather than negative. But not everyone will be seeing the benefits.

Business

Facewatch: The controversial tech that retailers have deployed to tackle shoplifting and violence

The Christmas period is upon us, and goods are flying off the shelves, but for some reason, the tills are not ringing as loudly as they should be.

Across the country, the five-finger discount is being used with such frequency that retailers are taking action into their own hands.

With concerns about the police response to shoplifting, many are now resorting to controversial facial recognition technology to catch culprits before they strike.

Sainsbury’s, Asda, Budgens and Sports Direct are among the high-street businesses that have signed up to Facewatch, a cloud-based facial recognition security system that scans faces as they enter a store. Those images are then compared to a database of known offenders and, if a match is found, an alert is set off to warn the business that a shoplifter has entered the premises.

It comes as official figures show shoplifting offences rose by 13% in the year to June, reaching almost 530,000 incidents. Figures reported in August showed more than 80% result in no charge.

At the same time, retailers are reporting more than 2,000 cases of violence or abuse against their staff every day. Faced with mounting losses and safety concerns, businesses say they are being forced to take security into their own hands because stretched police forces are only able to respond to a fraction of incidents.

A Facewatch camera

At Ruxley Manor Garden Centre in south London, managing director James Evans said theft had become increasingly brazen and organised, with losses from shoplifting now accounting for around 1.5% of turnover. “That may sound small, but it represents a significant hit to the bottom line,” he said, pointing out that thousands of pounds’ worth of goods can be stolen in a single visit.

“We have had instances where the children get sent in to do it. They know that the parents will be waiting in the car park and they’ll know that there’s nothing that we can do to stop them.”

Gurpreet Narwan is seen at the garden centre while being shown how Facewatch works

Staff members here have also had their fair share of run-ins with shoplifters. In one case, employees trying to stop a suspected shoplifter were nearly struck by an accomplice in a car. “This is no longer just about stock loss,” said James, “It is about the safety of our staff.”

However, the technology is not without its critics. Civil liberties groups have warned that the expansion of this type of technology is eroding our privacy.

Silkie Carlo, director of Big Brother Watch, called it “a very dangerous kind of privatised policing industry”.

Facewatch is seen in operation as retailers look to crack down on crime.

“[It] really threatens fairness and justice for us all, because now it’s the case that just going to do your supermarket shopping, a company is quietly taking your very sensitive biometric data. That’s data that’s as sensitive as your passport, and [it’s] making a judgement about whether you’re a criminal or not.”

Silkie said the organisation was routinely receiving messages from people who said they had been mistakenly targeted. They include Rennea Nelson, who was wrongly flagged as a shoplifter at a B&M store after being mistakenly added to the facial recognition database. Nelson said she was threatened with police action and warned that her immigration status could be at risk.

Gurpreet’s profile can be seen on the Facewatch database

“He said to me, if you don’t get out, I’m going to call the police. So at that point I turned around and I was like, are you speaking to me? Then he was like yes, yes, your face set off the alarm because you’re a thief… At that point, I was around six to seven months pregnant and I was having a high-risk pregnancy. I was already going through a lot of anxiety and, so him coming over and shouting at me, it was like really triggering me.”

The retailer later acknowledged the error and apologised, describing it as a rare case of human mistake.

Read more:

Elon Musk closer to becoming first-ever trillionaire

William and George help prepare Christmas lunch for the homeless

A spokesperson for B&M said: ‘This was a simple case of human error, and we sincerely apologise to Ms Nelson for any upset caused. Reported incidents like this are rare. Facewatch services are designed to operate strictly in compliance with UK GDPR and to help protect store colleagues from incidents of aggressive shoplifting.”

The cloud-based technology has critics who argue that it amounts to a misuse of personal data and privacy

Nick Fisher, chief executive of Facewatch, said the backlash was disproportionate.

“Well, I think it’s designed to be quite alarmist, using language like ‘dystopian’, ‘orwellian’, ‘turning people into barcodes’,” he said.

“The inference of that is that we will identify people using biometric technology, hold and store their own, store their data. And that’s just, quite frankly, misleading. We only store and retain data of known repeat offenders, of which it’s been deemed to be proportionate and responsible to do so… I think in the world that we are currently operating in, as long as the technology is used and managed in a responsible, proportionate way, I can only see it being a force for good.”

Yet, there is obviously widespread unease, if not anger, at the proliferation of this technology. Businesses are obviously alert to it, but the bottom line is calling.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024