Interest rate hikes ‘net positive’ for economy but not everyone

Here’s a sentence which might sound a little odd: higher interest rates have been good news for the UK economy.

For the first time in many decades, the pain faced by borrowers from higher interest rates has been more than balanced out by the benefit experienced by savers from those interest rates.

If this sounds a little odd it’s partly because invariably, when people – the media, politicians and economists – talk about interest rates they focus unduly on one side of the equation: the plight of the borrower. And there’s an understandable reason for that: in previous “hiking cycles”, when the Bank of England raises interest rates, that pain has invariably outweighed the windfall.

Money latest: Mortgage price war ‘likely’ as 3% interest rates predicted

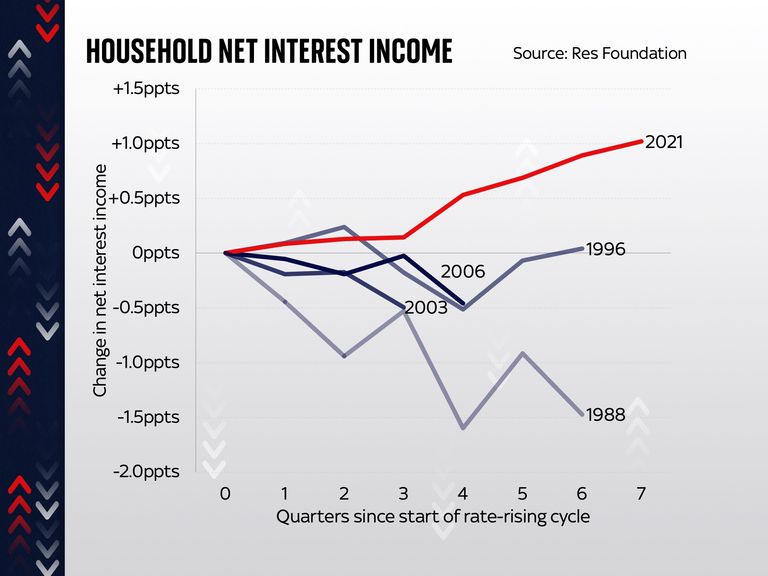

That was the case when borrowing rates were lifted in 1988; it was the case in 1996, in 2003 and in 2006.

In each case the overall impact, across the economy, on households’ balance sheets was negative.

But not so this time around.

According to the Resolution Foundation, the net income we’ve earned, across the economy, as a result of interest rates, has actually risen rather than fallen – up by a percentage point since rates started going up.

To put that into perspective, the “interest rate effect” on incomes in the late 1980s was -1.5 percentage points.

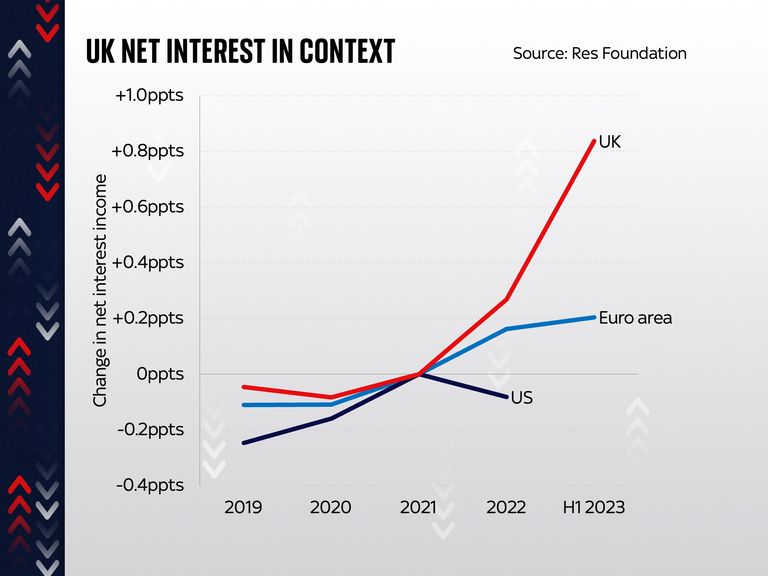

And what’s striking, when you compare the UK to the euro area and the US, is that we are a bit of an outlier: the interest rate effect, across the economy, was much more positive than it was in those two other areas.

This, says the Resolution Foundation, is at least part of the explanation for how the UK hasn’t yet slipped into the recession a lot of people anticipated this time last year.

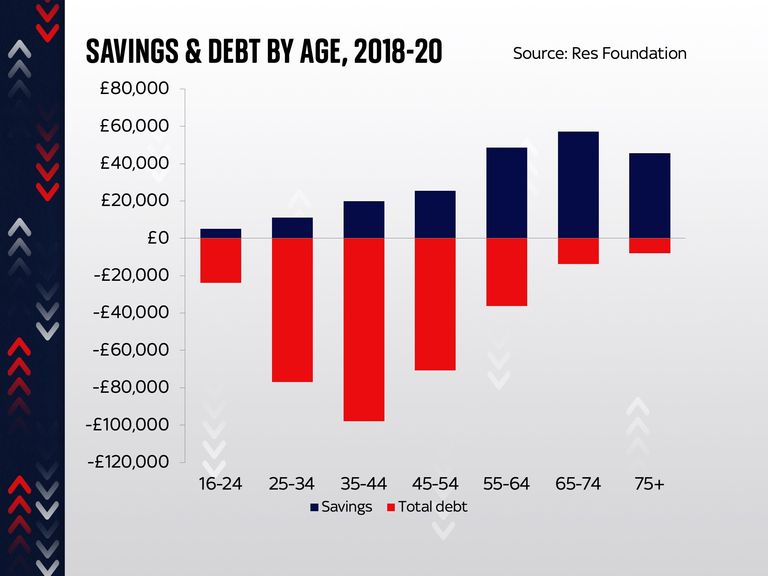

Part of the explanation for this is that it so happened, in large part because of the pandemic lockdowns, that people began this hiking cycle with a lot of savings in their bank accounts – far more than usual.

Read more:

Mortgage approvals up as more lenders cut rates

First-time buyers fall to ‘lowest level in a decade’

FTSE 100 bosses ‘earn typical UK annual salary in three days’

The upshot was that, across the economy, the benefit from those savings (and savings rates went up very quickly – albeit not to the levels of borrowing rates) was greater than the impact on mortgages and loans. Another part of the explanation is that so far only around half of those with fixed-rate mortgages have re-fixed their loans.

But there are a few very important provisos here. The first and perhaps most important is that while the above is certainly true across the whole economy, there’s a dramatic difference of experience for different categories of people.

Those whose debts outweigh their savings (which in this case mostly means younger people) will certainly see a negative impact from higher rates. Those with far more savings than debts – the older segments of the population – will see a benefit. In other words, the pain and the dividends are not being equally shared out. The old are doing much better; the young are doing worse.

And there are two other provisos. The first is that this positive impact will begin to wear off as more and more people re-fix their mortgages and go up from low-interest rates to higher rates. Even though the typical fixed-rate deal has been coming down recently, it’s still far higher than it was two or five years ago.

Click to subscribe to The Ian King Business Podcast wherever you get your podcasts

The final proviso is that none of the above takes into account the broader impact of the cost of living crisis.

Everyone is having to pay higher prices for nearly everything. And while the annual rate at which those prices are increasing (inflation) has decelerated, the level of prices remains more than 15% above where it was a couple of years ago.

That’s a painful adjustment for everyone. The good news is that the impact of rates – across the economy as a whole – has actually been positive rather than negative. But not everyone will be seeing the benefits.

The Marks & Spencer (M&S) executive responsible for its technology function is leaving the retailer months after a devastating cyber attack which disrupted its systems at a cost of hundreds of millions of pounds.

Sky News has learnt that Rachel Higham, M&S‘s chief digital and technology officer, is leaving the company.

A former WPP and BT Group executive, Ms Higham was hired by M&S early last year.

Money latest: How to give your child a financial head start

Her departure was announced in an internal memo circulated on Thursday.

In it, the company said she was “stepping back from her role”.

“Rachel has been a steady hand and calm head at an extraordinary time for the business, and we wish her well for the future”.

July: Four arrested over cyber attacks

The April cyber attack on M&S, which was conducted by a group called Scattered Spider, brought its online operations to a halt, underlining the growing threat posed by such incidents.

Its click-and-collect service is now back up and running, and the retailer expects part of its costs to be covered by insurance.

M&S said early last month that it was not looking to replace Ms Higham following an enquiry from Sky News.

It was unclear who would succeed her in the role or whether she would be eligible for a payoff.

An M&S spokeswoman confirmed on Thursday that the memo was genuine but refused to comment further.

The John Lewis Partnership (JLP) has blamed budget tax hikes for a deeper half-year loss.

The UK’s largest employee-owned business, which owns John Lewis department stores and Waitrose supermarkets, reported a headline loss before tax and exceptional items of £34m for the six months to 26 July.

That compared to a £5m loss in the same period last year. The higher figure was reached despite a 4% rise in group sales to £6.2bn.

Money latest: How to give your child a financial head start

“This result was significantly impacted by costs not present in the equivalent prior period”, the partnership explained, “including £29m of costs for the new Extended Producer Responsibility (EPR) packaging levy (where we took the full annual cost in our first half results), alongside higher National Insurance Contributions (NICs)”.

JLP said the loss figure also reflected additional investment in its systems and growth-led teams.

On a bottom line basis, the losses stood at £88m – up from £30m – as some exceptional costs associated with the group’s turnaround and some non-cash impairments were included.

JLP insisted it was on track to grow profitability in the core second half of its financial year, despite a “challenging” macroeconomic environment, as both operations were outperforming in their respective markets.

August: ‘We’ve got to get the balance right on tax’

The company cited benefits from its investment, which hit £191m over the six months, have been prioritised over partner bonuses during several years of recovery for the group that have seen underperforming department stores closed and jobs lost.

Jason Tarry, the former Tesco executive who has chaired the partnership for a year, said the outlook was positive despite consumer confidence remaining subdued.

“Our clear focus on accelerating investment in our customers and our brands is working: more customers are shopping with us, driving sales, and helping Waitrose and John Lewis outperform their markets”, he said.

“We achieved our highest recorded levels of positive customer satisfaction, a testament to the great service of our partners.

“The investments we are making, combined with our plans for peak trading, provide a strong foundation for the remainder of the year.

“While we are reporting a loss in the first half, we’re well positioned to deliver full-year profit growth, which we’ll continue to invest in our customers and partners.”

Market analysts have cautioned that the sales figures are likely to have been flattered by the disruption to trading at rival M&S, which suffered a cyber attack in April.

But Robyn Duffy, consumer markets senior analyst at RSM UK, said of the sales uplift: “Waitrose’s performance has been a key driver, benefiting from a renewed focus on its food proposition, including a greater emphasis on lower prices and a more effective adoption of technology to improve the customer experience.

“Meanwhile, the John Lewis retail arm is successfully drawing in customers through a combination of revitalised physical stores, a focus on meaningful brand partnerships, and the reintroduction of its Never Knowingly Undersold price matching strategy.”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment11 months ago

Environment11 months agoHere are the best electric bikes you can buy at every price level in October 2024