Interest rate hikes ‘net positive’ for economy but not everyone

Here’s a sentence which might sound a little odd: higher interest rates have been good news for the UK economy.

For the first time in many decades, the pain faced by borrowers from higher interest rates has been more than balanced out by the benefit experienced by savers from those interest rates.

If this sounds a little odd it’s partly because invariably, when people – the media, politicians and economists – talk about interest rates, they focus unduly on one side of the equation: the plight of the borrower. And there’s an understandable reason for that: in previous “hiking cycles”, when the Bank of England raises interest rates, that pain has invariably outweighed the windfall.

Money latest: Mortgage price war ‘likely’ as 3% rates predicted

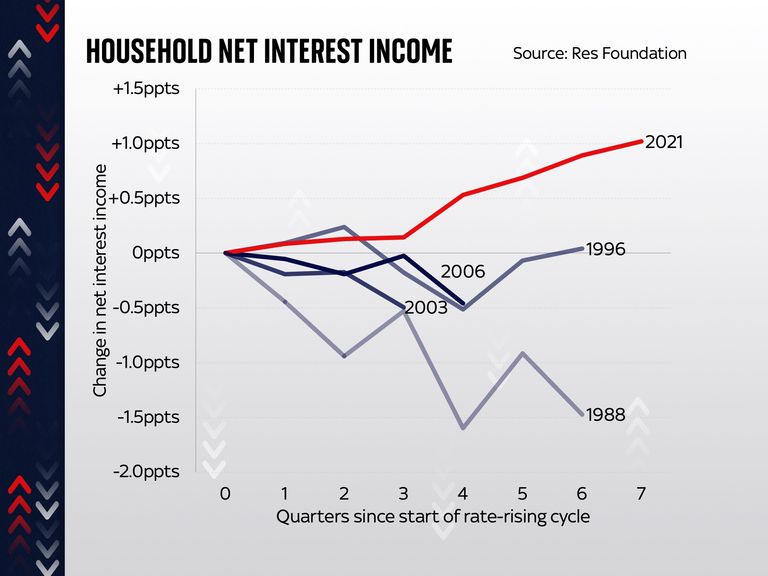

That was the case when borrowing rates were lifted in 1988; it was the case in 1996, in 2003 and in 2006.

In each case the overall impact, across the economy, on households’ balance sheets, was negative.

But not so this time around.

According to the Resolution Foundation, the net income we’ve earned, across the economy, as a result of interest rates, has actually risen rather than fallen – up by a percentage point since rates started going up.

To put that into perspective, the “interest rate effect” on incomes in the late 1980s was -1.5 percentage points.

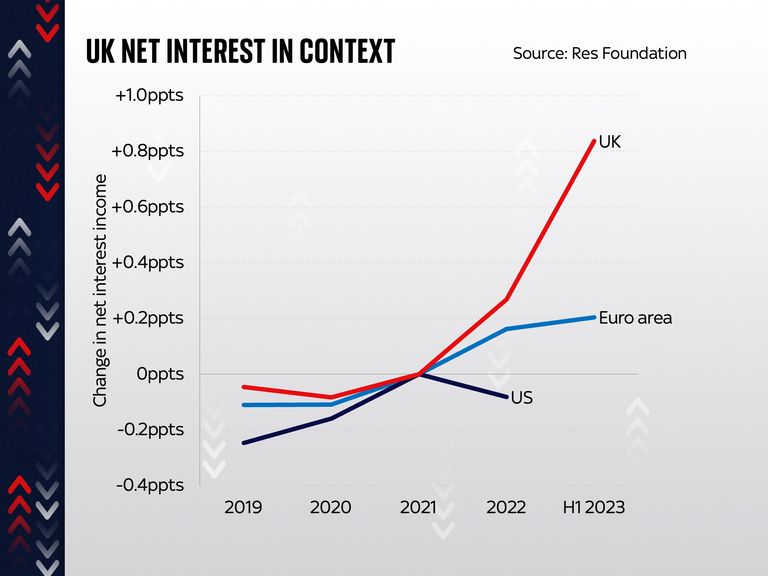

And what’s striking, when you compare the UK to the euro area and the US, is that we are a bit of an outlier: the interest rate effect, across the economy, was much more positive than it was in those two other areas.

This, says the Resolution Foundation, is at least part of the explanation for how the UK hasn’t yet slipped into the recession a lot of people anticipated this time last year.

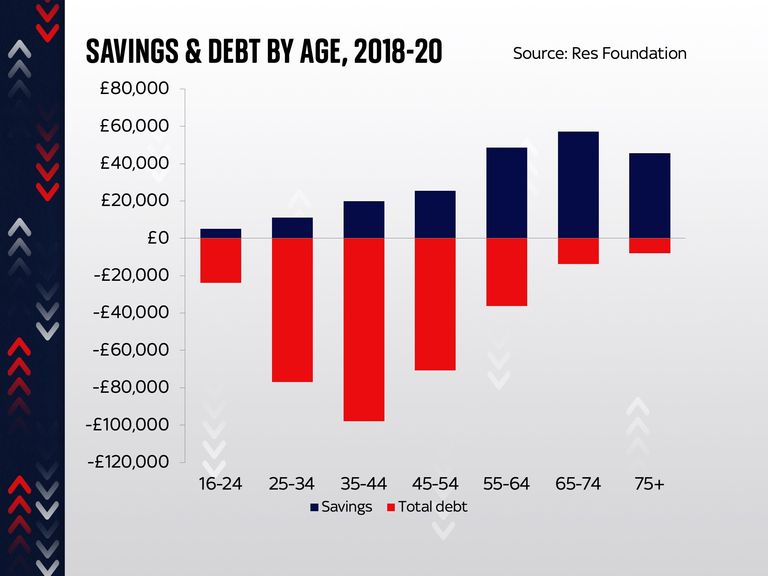

Part of the explanation for this is that it so happened, in large part because of the pandemic lockdowns, that people began this hiking cycle with a lot of savings in their bank accounts – far more than usual.

Read more:

Mortgage approvals up as more lenders cut rates

First-time buyers fall to ‘lowest level in a decade’

FTSE 100 bosses ‘earn typical UK annual salary in three days’

The upshot was that, across the economy, the benefit from those savings (and savings rates went up very quickly – albeit not to the levels of borrowing rates) was greater than the impact on mortgages and loans. Another part of the explanation is that so far only around half of those with fixed-rate mortgages have re-fixed their loans.

But there are a few very important provisos here. The first and perhaps most important is that while the above is certainly true across the whole economy, there’s a dramatic difference in experience for different categories of people.

Those whose debts outweigh their savings (which in this case mostly means younger people) will certainly see a negative impact from higher rates. Those with far more savings than debts – the older segments of the population – will see a benefit. In other words, the pain and the dividends are not being equally shared out. The old are doing much better; the young are doing worse.

And there are two other provisos. The first is that this positive impact will begin to wear off as more and more people re-fix their mortgages and go up from low interest rates to higher rates. Even though the typical fixed-rate deal has been coming down recently, it’s still far higher than it was two or five years ago.

Click to subscribe to The Ian King Business Podcast wherever you get your podcasts

The final proviso is that none of the above takes into account the broader impact of the cost of living crisis.

Everyone is having to pay higher prices for nearly everything. And while the annual rate at which those prices are increasing (inflation) has decelerated, the level of prices remains more than 15% above where it was a couple of years ago.

That’s a painful adjustment for everyone. The good news is that the impact of rates – across the economy as a whole – has actually been positive rather than negative. But not everyone will be seeing the benefits.

Donald Trump has said he will sue the BBC for between $1bn and $5bn over the editing of his speech on Panorama.

The US president confirmed he would be taking legal action against the broadcaster while on Air Force One overnight on Saturday.

“We’ll sue them. We’ll sue them for anywhere between a billion (£792m) and five billion dollars (£3.79bn), probably sometime next week,” he told reporters.

“We have to do it, they’ve even admitted that they cheated. Not that they couldn’t have not done that. They cheated. They changed the words coming out of my mouth.”

Mr Trump then told reporters he would discuss the matter with Prime Minister Sir Keir Starmer over the weekend, and claimed “the people of the UK are very angry about what happened… because it shows the BBC is fake news”.

The Daily Telegraph reported earlier this month that an internal memo raised concerns about the BBC’s editing of a speech made by Mr Trump on 6 January 2021, just before a mob rioted at the US Capitol building, on its flagship late-night news programme.

BBC crisis: How did it happen?

The concerns regard clips spliced together from sections of the president’s speech to make it appear he told supporters he was going to walk to the US Capitol with them to “fight like hell” in the documentary Trump: A Second Chance?, which was broadcast by the BBC the week before last year’s US election.

Following a backlash, both BBC director-general Tim Davie and BBC News chief executive Deborah Turness resigned from their roles.

‘No basis for defamation claim’

On Thursday, the broadcaster officially apologised to the president and added that it was an “error of judgement” and the programme will “not be broadcast again in this form on any BBC platforms”.

A spokesperson said that “the BBC sincerely regrets the manner in which the video clip was edited,” but they also added that “we strongly disagree there is a basis for a defamation claim”.

Earlier this week, Mr Trump’s lawyers threatened to sue the BBC for $1bn unless it apologised, retracted the clip, and compensated him.

The US president said he would sue the broadcaster for between $1bn and $5bn. File pic: PA

Legal challenges

But legal experts have said that Mr Trump would face challenges taking the case to court in the UK or the US.

The deadline to bring the case to UK courts, where defamation damages rarely exceed £100,000 ($132,000), has already expired because the documentary aired in October 2024, which is more than one year.

Also because the documentary was not shown in the US, it would be hard to show that Americans thought less of the president because of a programme they could not watch.

Read more from Sky News:

Key findings in 20,000 pages of documents in the Epstein files

Banksy art theft lands burglar with 13-month prison sentence

Sky’s Katie Spencer on what BBC bosses told staff on call over Trump row

Newsnight allegations

The BBC has said it was looking into fresh allegations, published in The Telegraph, that its Newsnight show also selectively edited footage of the same speech in a report broadcast in June 2022.

A BBC spokesperson said: “The BBC holds itself to the highest editorial standards. This matter has been brought to our attention and we are now looking into it.”

This breaking news story is being updated and more details will be published shortly.

Please refresh the page for the latest version.

You can receive breaking news alerts on a smartphone or tablet via the Sky News app. You can also follow us on WhatsApp and subscribe to our YouTube channel to keep up with the latest news.

A man has been given a 13-month prison sentence for stealing Banksy’s famous Girl With Balloon print from a London gallery.

Larry Fraser, 49, of Beckton, east London, was sentenced on Friday after pleading guilty to one count of non-residential burglary at Kingston Crown Court on 9 October.

The print, one of the street artist‘s most famous, was stolen from a gallery in New Cavendish Street in London at around 11pm on 8 September last year.

The recovered artwork back in the gallery. Pic: Metropolitan Police

Fraser used a hammer to smash his way through a glass entrance door at the Grove Gallery before stealing the artwork, which was valued at £270,000.

He concealed his identity with a mask, hooded jacket and gloves, but the Metropolitan Police’s Flying Squad was able to identify him and track him to a location streets away.

He was also caught on CCTV loading the artwork into a van before fleeing the scene.

A second man, 54-year-old James Love, was accused of being the getaway driver in the burglary, but cleared of stealing the print.

Larry Fraser. Pic: Metropolitan Police

Damage to the Grove Gallery after the theft. Pic: Metropolitan Police

Fraser was arrested at his home address on 10 September, within 48 hours of the burglary, and charged the next day.

Officers were able to recover the artwork after executing a warrant on the Isle of Dogs. It has now been returned to the gallery.

Fraser pleaded to the court that he was struggling with a historic drug debt and agreed to steal the work “under a degree of pressure and fear”.

He said he did not know what he would be stealing, nor its value, until the day of the offence.

Fraser was caught on CCTV taking the artwork away from the gallery. Pic: Metropolitan Police

Jeffrey Israel, defending, said Fraser lived with his mother as her principal carer, and had only managed to “break his cycle of drug addiction” after his last prison sentence.

He added that it “would take a bold advocate” to suggest that the value of the print had increased by the burglary, but insisted “that is probably the reality”.

Read more:

Banksy artwork ‘worth millions’ scrubbed off wall outside court

Blink-182 star to auction rare Banksy worth millions

Judge Anne Brown was unmoved, however, and said the offence was “simply too serious” for a suspended sentence.

“This is a brazen and serious non-domestic burglary,” she said.

“Whilst you did not know the precise value of the print, you obviously understood it to be very valuable.”

She added: “Whilst I am sure there was a high degree of planning, this was not your plan.”

However, Fraser may be eligible for immediate release due to time spent on electronic curfew.

Detective Chief Inspector Scott Mather, who led the Met’s investigation, said: “Banksy’s Girl With Balloon is known across the world – and we reacted immediately to not just bring Fraser to justice but also reunite the artwork with the gallery.

“The speed at which this took place is a testament to the tireless work of the flying squad officers – in total it took just four days for normality to be restored.”

The 2004 artwork was part of a £1.5m collection of 13 Banksy pieces at the gallery.

Gallery manager, Lindor Mehmetaj, said it was “remarkable” for the piece to have been recovered after the theft.

The 29-year-old said: “I was completely, completely shocked, but in a very, very positive way when the Flying Squad showed me the actual artwork.

“It’s very hard to put into words, the weight that comes off your shoulders.”

UK

‘Incredibly dangerous’ sex offender Chao Xu jailed – as police say there could be hundreds more victims

An “incredibly dangerous” sex offender who drugged his victims and installed spy cameras around his home has been jailed for life with a minimum term of 14 years – as police appeal for hundreds more potential victims to come forward.

Warning: This article contains details of sexual offences

Chinese national Chao Xu, 33, has been described by police as “one of the most prolific offenders ever uncovered” by the Metropolitan Police.

Xu, who was a law postgraduate student at the University of Greenwich in London between 2015 and 2016, ran his own recruitment business and targeted victims at networking events at his home.

He invented his “Spring of Life” cocktail, a mix of alcohols and Chinese herbal medicines, to sedate guests, and planted spy cameras in items including air fresheners, sanitary packaging and speakers.

Chao Xu setting up his camera

Pic: Met Police:

Police found thousands of pictures and videos, with some showing unconscious or incapacitated victims in his flat in Greenwich, south-east London.

Xu, who is from China but is believed to have been living in the UK since 2013, also covertly filmed women on their daily commutes at stations such as London Bridge in so-called upskirting incidents.

He pleaded guilty to 24 sex offences between 2021 and 2025 at Woolwich Crown Court in August relating to six victims, with two charges relating to a seventh woman left to lie on file.

Xu admitted four counts of rape, eight counts of assault by penetration, four counts of sexual assault, four counts of voyeurism, two counts of administering a substance with intent and two counts of operating equipment beneath the clothing of another without consent (commonly known as upskirting).

Special drink

Pic: Met Police:

An air freshener with a hidden camera.

Pic: Met Police

An air freshener with a hidden camera

Pic: Met Police

‘Incredibly dangerous man’

His Honour Judge Christopher Grout described Xu as an “incredibly dangerous man” who “took great enjoyment” from his offending.

“Your behaviour was calculated and planned, evidenced by the covert recording systems you had set up in your flats and the fact you had incapacitated a number of your victims by drugging them.

“You betrayed the trust of a number of women who you befriended in the most appalling ways imaginable,” he added.

Speaker with hidden camera

Pic: Met Police:

Hidden camera in bottom left of women’s sanitary packaging

Pic: Met Police

Could be hundreds of victims

Another 11 alleged victims have since come forward but the Metropolitan Police believe there are hundreds more in the UK and China, with offences committed in workplaces, public spaces and overseas.

Acting Detective Superintendent Lewis Sanderson described Xu as one of the “most prolific” offenders the force has ever investigated, adding that his “crimes were calculated, sustained, and devastating”.

Speaking outside the court on Friday, he said: “Chao Xu was a prolific and predatory sexual offender who committed some of the most cowardly and abhorrent crimes imaginable. His actions caused deep and lasting harm.”

“The number of victims of sexual assault, voyeurism and upskirting is believed to be in the hundreds. This includes individuals filmed without consent in Xu’s flat at his workplace and in public spaces.

“That is why today I’m making a direct appeal. If you believe you may have been a victim of Chao Xu, or if you have any information that could assist our investigation, please come forward. You will be listened to. You will be believed and you will be supported.”

Xu was ‘prolific’ sex offender

He said all of the sexual assault victims were Chinese women, aged between 18 and 30, while the voyeurism victims are also young females but of different ethnicities.

He added that there will be women who may not know they are victims of his crimes, as they may have been drugged by Xu.

Detectives were alerted to Xu’s crimes after he held a networking event in Greenwich in June.

Read more from Sky News:

Man admits to summer camp attacks

Murder investigation after girl’s death

Burglar jailed over Banksy theft

When one of the women who attended became unwell, Xu offered to let her stay, before raping her several times, the Metropolitan Police said.

They later found he had drugged her with substances known to cause drowsiness and incapacitation.

The case included six million messages on WeChat, the popular Chinese messaging app, most of them in Mandarin, which all had to be checked with the help of a translator.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024