Woolworths demise 15 years on: What happened at the retail giant and could it come back?

Parachuted in to turn around a failing giant of the British high street, Robert McDonald was part of Woolworths’s last roll of the dice.

The new finance director said he was excited to join an “iconic” brand when he began work in early November 2008, but just three weeks later the company would sink into administration.

And there was little the company’s last ever executive hire could do to stop the famous store – known for its pick ‘n’ mix, homeware and everything in between – from closing for good on 6 January 2009.

“Like everyone my age, I had grown up thinking its existence was a normal part of life,” Mr McDonald told Sky News.

“I was very pleased to have the opportunity to work there. I knew it was going through hard times and looked forward to being able to help.

“But, sadly, it was past that by the time I joined, and the end seemed very swift.”

Analysts blame its downfall on a toxic combination of low cash reserves, lost credit insurance and crippling debt – all exacerbated by the 2008 financial crisis.

It marked the end of Woolies’s near century-long presence on the high street, with more than 800 stores closed down and about 27,000 jobs lost.

Woolworths was popular for its pic ‘n’ mix

For many of its staff, news of Woolworths’s demise into administration came from the media, with earlier rumours confirmed in reports on 26 November 2008.

Paul Seaton, who had worked as a store manager and as part of the IT team during 25 years at the company, said his colleagues “crowded around the TV” to hear their worst fears confirmed.

“It just all fell to pieces after that,” Mr Seaton, now 61, told Sky News.

“The sad reality is Woolworths took 99 years to build, and it took 42 days from administration to the day the last door shut. 99 years of meticulous care and thought… gone.”

The board insisted administration wouldn’t detract from “business as usual”, Mr Seaton said, but that all changed when he was called to a meeting on 5 December.

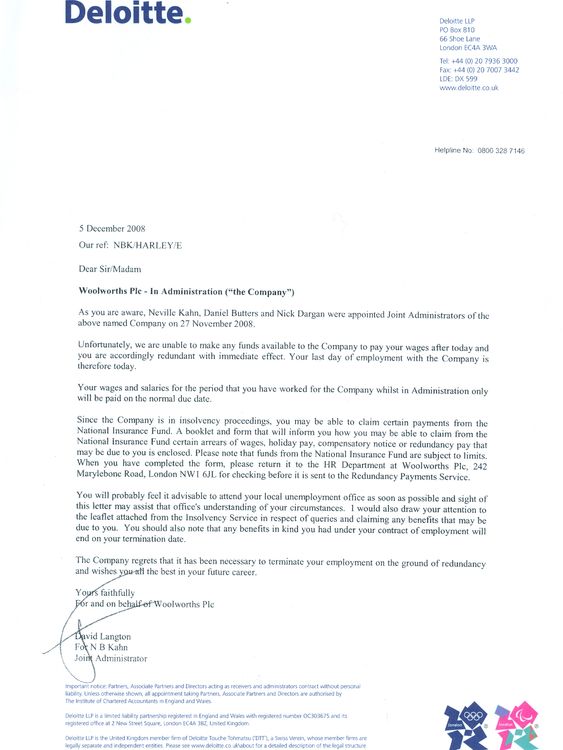

He was among 500 senior figures gathered at Woolworths HQ, where each was given a letter written by administrators Deloitte notifying none would be paid another day and all had lost their jobs with immediate effect.

The notice given by Deloitte to Paul Seaton

“We were summoned and told not to come back, all 500 of us,” Mr Seaton said, adding their passes into the building were deactivated on the spot. “The business only carried on for one month after that.”

While his time at the company came to an abrupt end, he dedicated time to creating a virtual Woolworths museum, preserving memorabilia and documenting the chain’s long history.

A store for the family

The first store opened in November 1909 in Liverpool, by New Yorker Frank Woolworth, who had already established the brand in the US.

In a prescient diary entry, he wrote during an earlier trip to Europe that “a good penny and sixpence store, run by a live Yankee, would be a sensation here”.

Such was the success of the UK counterpart, his successor Byron Miller reportedly beamed that “the child has long since outgrown the parent”.

Mr Seaton thinks the literal child-parent relationship was key to the store’s popularity.

“There used to be old adage that people need Tesco because everyone has to eat, and people trust Boots because you call the manager ‘doctor’, but they went to Woolworths because they love Woolworths,” he said.

“Have you ever heard a kid saying ‘mum I want to go to Tesco’? The whole reason I loved being a manager is kids and families loved coming to Woolworths.”

Paul Seaton with Woolworths memorabilia collected over the years

The store’s name lives on in Australia – though has no connection with US or UK equivalents – where it is the country’s largest supermarket chain and last year recorded a net profit of $1.62bn (about £87bn).

US stores closed in 1997, but the UK branches recorded a record profit topping £100m just one year later.

What went wrong?

Customers were still shopping at the UK stores, and in the firm’s final annual report the company made a slight pre-tax profit in 2007.

But even with some signs of recovery ahead of 2008, Woolworths had a terminal problem: modest cash flow and a £385m mountain of debt.

Retail expert Clare Bailey was among the consultants drafted in 2006 to tackle the mammoth task of detangling the company’s supply chain, which she says was collecting too much of some stock and too little of others.

As banks began to lose faith in Woolworths’s finances, the firm had its credit insurance withdrawn – meaning it had to pay suppliers immediately, rather than in instalments.

To make matters worse, many Woolworths stores were sold a few years before and rented back at a price that only appeared to increase over the years.

Left with fewer assets, little in way of cash reserves and no credit insurance, the retailer was not prepared for the coming shock of the 2008 financial crisis.

“Cashflow is like oxygen,” Ms Bailey told Sky News. “You can be profitable, but if you haven’t got cash to pay bills or for when something goes wrong, then that’s it – game over.”

The company reported a pre-tax loss of £90.8m over the first half of 2008 in September that year, despite launching the WorthIt range – promoting low-cost products – in 2007.

Losing sales and customers

One of the big issues Ms Bailey identified in the supply chain was a failure to keep evergreen products on shelves.

For example, she said only 20 stores out of more than 800 nationwide had the correct amount of coat hangers, a product that sells all year, while others bought far too many Christmas trees.

It meant money was “trapped in stocks”, she said, and would gradually turn customers away.

“And if you replicate that through other products, customers could find what they didn’t want, but not what they wanted,” she said.

“You might, as a customer, give them the benefit of the doubt a few times, but eventually they will turn to other places. So, they not only lost the sale – they also lost the customers.”

It’s this perceived neglect of the customer journey that small business growth expert Claire Hancott believes cost Woolworths at the turn of the century.

Footfall almost halved from 7.5 million in 2000 to around 4.5 million in 2007, she said, while the market for Woolworths’s once-popular CDs was shrinking as more consumers headed to the internet.

“Businesses can’t ignore these big trends, even if they won’t come into play for years,” Ms Hancott told Sky News.

“Blockbusters was a classic example, when they thought digital films wouldn’t take off.

“Woolworths wasn’t at the forefront of consumer technology and it’s so important to be looking 10, 20 years into the future – it takes a long time to prepare.”

Discount stores such as pound shops began to pop up on the high street, adding to growing competition that ultimately forced an attempt to sell the company in November 2008 for – ironically – just £1.

It was hoped a sale to restructuring experts Hilco would give them the job of repaying the debt, but the banks rejected the move.

The company went into administration just days later.

A false dawn, but will the sun rise on Woolworths again?

Ever since the company collapsed under the weight of its debt, rumours of a potential return to the high street have never been completely quashed.

A fake announcement – made by a social media account falsely claiming to be run by Woolworths – heralding a comeback was met with excitement in 2020, with savings platform Raisin UK reporting 44% of people discussing the store’s revival online “loved the news”.

The post turned out to be false

In August 2022, pollsters at YouGov found 49% of survey respondents said they wished they could bring back Woolies – a far higher proportion than any other defunct chain.

But for all the hopes of an encore, some of those involved with the firm rue the time that has since been lost – and believe it may have even survived.

“I came in at the end of 2006, but the work we were doing can take three or five years,” Ms Bailey said. “Maybe they started too late.”

All but a small handful of the Woolworths stores were re-let to other retailers within a decade, she added, meaning the spaces “still had merit in the local community”.

“The inner workings of a business are quite complicated,” she said.

“But I think it’s a sad situation it collapsed, because – had they been given a stay of execution – they may well have been successful in turning it around.”

Read more:

Christmas tree from 1920s Woolworths sells for ‘astonishing’ price

Next raises profit forecast but warns stock could be delayed by Red Sea attacks

Ms Hancott agrees: “In another time, would it have crumbled? That’s the million-pound question that nobody will be able to answer.

“Had it not been in the midst of a crisis, then it may have survived.”

For Mr McDonald, a chance to draw on his experience handling company finances never materialised.

It was, nonetheless, a “fascinating experience”, he said.

“It’s such a shame we didn’t have longer to turn that business around,” he said.

“I joined as part of a turnaround plan, but it was too late to change the course of history.”

The rate of inflation hit a much lower than expected 3.2% last month, according to official figures which should lock in an interest rate cut by the Bank of England on Thursday.

The Office for National Statistics (ONS) reported an easing in the pace of the main consumer prices index measure from the 3.6% annual rate seen in October.

The main downwards pressure came from food costs amid a supermarket price war to secure custom ahead of the core Christmas season.

Money latest: What the fall in inflation means for you

ONS chief economist Grant Fitzner noted decreases in the prices paid for cakes, biscuits and breakfast cereals in particular.

“Tobacco prices also helped pull the rate down, with prices easing slightly this month after a large rise a year ago”, he wrote.

“The fall in the price of women’s clothing was another downward driver.

“The increase in the cost of goods leaving factories slowed, driven by lower food inflation, while the annual cost of raw materials for businesses continued to rise.”

The data marked further downwards progress for the headline rate after a spike this year which economists have partly attributed to higher employment costs, imposed after the government’s first budget, being passed on to consumers.

This price wave has muddied the waters over the pace of interest rate reductions by the Bank, which has wanted to see more evidence that inflation is not being further stoked by factors including strong wage growth.

It will be encouraged by better than expected slowdowns in other closely-watched inflation measures which strip out volatile elements, such as food and energy, as well as services inflation.

Recent data has also shown intensifying weakness in the labour market, with the unemployment rate surging by a percentage point to 5.1% since Labour took office.

Separate ONS figures have also found that the economy contracted for two consecutive months in the run-up to Rachel Reeves’s second budget.

London Stock Exchange Group Data shows more than 90% of financial market participants are expecting the Bank to agree a rate cut to 3.75% – the lowest level in almost three years – from 4%.

The inflation data will come as a relief to the chancellor after a tough few months for her politically given the wider economic data and backlash over the Treasury’s handling of the lead up to the budget.

Ms Reeves said: “I know families across Britain who are worried about bills will welcome this fall in inflation.

“Getting bills down is my top priority. That is why I froze rail fares and prescription fees and cut £150 off average energy bills at the budget this year.

“The Bank of England agree this will help cut prices and expect inflation to fall faster next year as a result.”

You’ve doubtless heard of the National Grid, the network of pylons and electricity infrastructure ensuring the country is supplied with power. You’re probably aware that there is a similar national network of gas pipelines sending methane into millions of our boilers.

But far fewer people, even among the infrastructure cognoscenti, are even faintly familiar with the UK Ethylene Pipeline System. Yet this pipeline network, obscure as it might be, is one of the critical parts of Britain’s industrial infrastructure. And it’s also a useful clue to help explain why the government has just announced it’s spending more than £120m to bail out the chemical plant at Grangemouth in Scotland.

Ethylene is one of those precursor chemicals essential for the manufacture of all sorts of everyday products. React it with terephthalic acid and you end up with polyester. Combine it with chlorine and you end up with PVC. And when you polymerise ethylene itself you end up with polyethylene – the most important plastic in the world.

Why Grangemouth matters

Ethylene is, in short, a very big deal. Hence, why, many years ago, a pipeline was built to ensure Britain’s various chemical plants would have a reliable supply of the stuff. The pipes connected the key nodes in Britain’s chemicals infrastructure: the plants in the north of Cheshire, which derived chemicals from salt, the vast Wilton petrochemical plant in Teesside and, up in Scotland, the most important point in the network – Grangemouth.

The refinery would suck in oil and gas from the North Sea and turn it into ethane, which it would then “crack”, an energy-hungry process that involves heating it up to phenomenally high temperatures. Some of that ethylene would be used on site, but large volumes would also be sent down the pipeline. It would be pumped down to Runcorn, where the old ICI chlor-alkali plant, now owned by INEOS, would use it to make PVC. It would be sent to Wilton, where it would be turned into polyethylene and polyester.

Read more from Ed Conway:

The reality of Trump’s trade war

The reason for Trump’s Venezuela exploits

That’s the first important thing to grasp about this network – it is essential for the operation of a whole series of plants, many of them run by entirely different companies.

The second key thing to note is that, after the closure of the cracker at Wilton (now owned by Saudi company Sabic) and the ExxonMobil plant at Mossmorran in Fife, Grangemouth is the last plant standing. While the refinery no longer uses North Sea oil and gas, instead shipping in ethane from the US, it still makes its own ethylene.

So when INEOS began consulting on plans to close that ethylene cracker, officials down south in Westminster began to panic. The problem wasn’t just the 500 or so jobs that might have been lost in Grangemouth. It was the domino effect that would feed throughout the sector. All of a sudden, all those plants at the other ends of the pipeline would be affected too. In practice, the closure might have eventuated in more than a thousand job losses – maybe more.

What’s happening now?

All of which helps explain the news today – that the Department for Business and Trade is putting more than £120m of taxpayer money into the site. The bailout (it’s hard to see it as anything but) is not the first. The government has also put hundreds of millions of pounds of taxpayer money into British Steel, which it quasi-nationalised earlier this year, not to mention extra cash into Tata Steel at Port Talbot and loan guarantees to help Jaguar Land Rover after it faced an unprecedented cyber attack.

Work ground to a halt at JLR’s Wolverhampton factory after a cyber attack. Pic: PA

But while this package will undoubtedly provide Christmas cheer here in Grangemouth today, the government is left facing two distinct problems.

Reactive rather than strategic

The first is that for all that the chancellor and business secretary (who are themselves planning to visit Grangemouth today) are keen to pitch this latest move as a coherent part of their industrial strategy, it’s hard not to see it as something else. Far from appearing strategic, instead they seem reactive. To the extent that they have a coherent industrial strategy, it mostly seems to involve forking out public money when a given plant is close to closure. If they weren’t already, Britain’s industrialists will today be wondering to themselves: what would it take to get ourselves some of this money in future?

The crisis continues

The second issue is that the Grangemouth bailout is very unlikely to end the crisis spreading across Britain’s chemicals sector. A series of plants – some prominent, others less so – have closed in the past few years. The chemicals sector – once one of the most important in the economy – has seen its economic output drop by more than 20% in the past three years alone.

This is not just a UK-specific story. Something similar is happening across much of Europe. But for many chemicals companies, it simply doesn’t add up to invest and build in the UK any more – a product in part of regulations and in part of high energy costs. In short, this story isn’t over yet. There will be more twists and turns to come.

Britain loves chocolate.

We’re estimated to consume 8.2kg each every year, a good chunk of it at Christmas, but the cost of that everyday luxury habit has been rising fast.

Whitakers have been making chocolate in Skipton in north Yorkshire for 135 years, but they have never experienced price pressures as extreme as those in the last five.

“We buy liquid chocolate and since 2023, the price of our chocolate has doubled,” explains William Whitaker, the real-life Willy Wonka and the fourth generation of the family to run the business.

William Whitaker, managing director of the company

“It could have been worse. If we hadn’t been contracted [with a supplier], it would have trebled.

“That represents a £5,000 per-tonne increase, and we use a thousand tonnes a year. And we only sell £12-£13m of product, so it’s a massive effect.”

Whitakers makes 10 million pieces of chocolate a week in a factory on the much-expanded site of the original bakery where the business began.

Automated production lines snake through the site moulding, cutting, cooling, coating and wrapping a relentless procession of fondants, cremes, crisps and pure chocolate products for customers, including own-brand retail, supermarkets, and the catering trade.

Mmmmm….

Steepest inflation in the business

All of them have faced price increases as Whitakers has grappled with some of the steepest inflation in the food business.

Cocoa prices have soared in the last two years, largely because of a succession of poor cocoa harvests in West Africa, where Ghana and the Ivory Coast produce around two-thirds of global supply.

A combination of drought and crop disease cut global output by around 14% last year, pushing consumer prices in the other direction, with chocolate inflation passing 17% in the UK in October.

…chocolate….

Skimpflation and shrinkflation

Some major brands have responded by cutting the chocolate content of products – “skimpflation” – or charging more for less – “shrinkflation”.

Household-name brands including Penguin and Club have cut the cocoa and milk solid content so far they can no longer be classified as chocolate, and are marketed instead as “chocolate-flavour”.

Whitakers have stuck to their recipes and product sizes, choosing to pass price increases on to customers while adapting products to the new market conditions.

“Not only are major brands putting up prices over 20%, sometimes 40%, they’ve also reduced the size of their pieces and sometimes the ingredients,” says William Whitaker.

“We haven’t done any of that. We knew that long-term, the market will fall again, and that happier days will return.

“We’ve introduced new products where we’ve used chocolate as a coating rather than a solid chocolate because the centre, which is sugar-based, is cheaper than the chocolate.

“We’ve got a big product range of fondant creams, and others like gingers and Brazil nuts, where we’re using that chocolate as a coating.”

The costs are adding up

A deluge of price rises

Brazil nuts have enjoyed their own spike in price, more than doubling to £15,000 a tonne at one stage.

On top of commodity prices determined by markets beyond their control, Whitakers face the same inflationary pressures as other UK businesses.

“We’ve had the minimum wage increasing every year, we had the national insurance rise last year, and sort of hidden a little bit in this budget is a business rate increase.

“This is a small business, we turn over £12m, but our rates will go up nearly £100,000 next year before any other costs.

“If you add up all the cocoa and all the other cost increases in 2024 and 2025, it’s nearly £3m of cost increases we’ve had to bear. Some of that is returning to a little normality. It does test the relevance of what you do.”

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024