Thousands are being targeted by harsh HMRC tax-collecting scheme linked to 10 suicides

Four years ago, Michael Squires received a letter that turned his life upside down.

A brown envelope containing a tax demand for £24,000 landed on his doormat.

It came out of nowhere and gave Mr Squires sleepless nights as he worried about where he would find the money.

“It’s a horrible anxious feeling, I knew that I had taken due diligence and I knew that I had done what I thought was right,” he said.

“So, you feel the system is against you, you feel like you can’t fight back. In a way, you know that you’ve been conned, and you feel stupid… and I felt that for quite some time.”

Mr Squires, a healthcare worker from Leicestershire, is not alone.

‘Unjust campaign is targeting wrong people’

Tens of thousands of people across the country are facing crippling tax demands from HMRC in a harsh campaign that has been linked to 10 suicides.

HMRC has been ruthlessly pursuing people with the “loan charge” which came into force in 2017 through a piece of legislation that targeted those who were paid their salaries through loan schemes. It made individuals liable for tax that their employers should have paid.

Tax lawyers described it as an unjust campaign that is targeting the wrong people and undermining the rule of law by overriding statutory taxpayer rights.

HMRC has been targeting workers who had their salaries paid into umbrella companies, which would pay individuals a loan that was typically not paid back. Many of those who signed up, including nurses, supply teachers and council workers, had little or no choice but to take on work through these schemes.

They were directed to the schemes by their work agencies, reassured that their tax and national insurance was being taken care of and that the schemes were HMRC compliant.

In many cases, they were mis-sold.

Tens of thousands in fear of bankruptcy

For years HMRC failed to act against these schemes, which resulted in widespread underpayment of income tax and national insurance. The courts have since ruled that the employers or agencies should have been paying tax to the exchequer. However, the loan charge legislation allowed HMRC to pursue individuals in lieu of the agencies or employers.

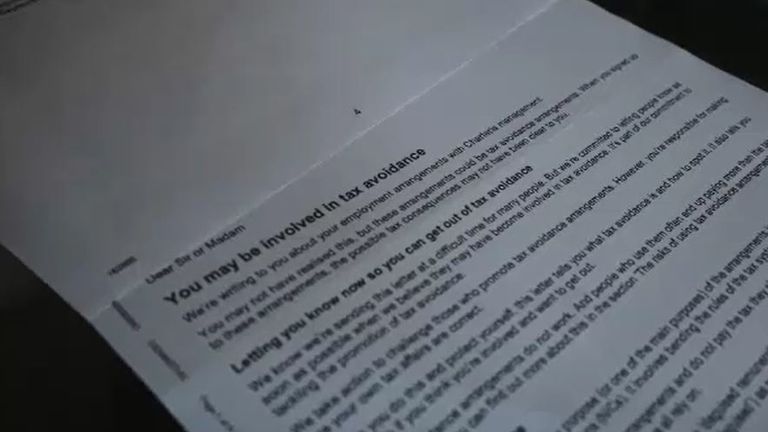

Five years ago HMRC started sending letters to individuals, explaining that these schemes were “disguised remuneration schemes”, imposing a tax liability on what it now classified as income and applying interest – then urging them to settle.

In some cases, the bills ran into the hundreds of thousands of pounds. Those who could or would not pay were warned that they would be hit with a loan charge, typically a much larger amount because the total sum was taxed in a single year, often applying a 45% tax rate on the income. It meant that in many cases people were paying back far more than they would have done if they weren’t part of the schemes.

HMRC threatened to take people’s possessions and sell them at auction if they didn’t find the money.

In some cases, the agency set up payment plans, but in others, people had little choice but to take out further loans.

Tens of thousands of people are still living in fear of bankruptcy, and they could be forced to hand over cash if and when they sell their homes.

The consequences have been devastating.

Warning of further suicides

Sky News has spoken to families whose lives have been torn apart. One woman told us that her marriage was breaking down, while others described dangerous mental health spirals.

HMRC has admitted that there have been 10 suicides linked to the loan charge.

It has referred cases of suicide to the Independent Office for Police Conduct (IOPC), which oversees certain serious complaints about the conduct of tax inspectors.

Campaigners have repeatedly warned of the risk of further suicides and have demanded that HMRC provide a 24-hour suicide prevention helpline.

Mr Squires said: “We are being pursued by a very big organisation who hasn’t warned us. I received a warning letter four years later that I may have been employed by a company involved in a scheme that wasn’t legitimate.

“So, we’ve had no warning. HMRC is not out of pocket. The umbrella companies aren’t out of pocket.

“The agencies that pushed it aren’t out of pocket. It’s only the end worker and we’re just normal people.”

Michael Squires says he felt like the system was against him

HMRC targeting individuals rather than scheme organisers

While some of those who engaged in loan schemes entered into them with the explicit intent to minimise their tax bills, a large number were simply trying to do the right thing.

In many cases individuals were advised by their work agencies to sign up to the umbrella companies to streamline their tax affairs, helping them to avoid the complicated process of setting up a limited company.

Others turned to the umbrella companies because they were worried about falling foul of new IR35 rules that apply to contractors operating as limited companies.

The NHS, local authorities and other public sector organisations all engaged workers who were part of these schemes.

Back in 2021 HMRC even admitted that it had at least 15 contractors on its own books who were part of “disguised remuneration schemes” between 2016 and 2020.

Read more from Sky News:

Asylum seekers moved from taxpayer-funded hotels – to other hotels

Warning about huge number of Facebook Marketplace scams

Toddler found starved to death – prompting questions for police

Keith Gordon, a tax barrister, said: “When the contractors were paid, the PAYE rules applied and were meant to ensure the tax was deducted from the salary before it was received by the workers.

“That PAYE was not paid. The workers suffered a deduction but that was just simply taken as fees by the promoters of the schemes which were running rather dubious tax avoidance of agents without contractors’ knowledge.”

He suggested that HMRC were targeting individuals instead of the organisers of the schemes because it was an easier way of recouping the money.

Mr Gordon continued: “Number one: The promoters have deeper pockets and might be able to fight back against unfair legislation.

“Number two: That would probably amount to admitting the revenue made a mistake in the first place.

“Number three: Some of these promoters are now insolvent because they’ve had plenty of years to wind up their affairs and become out of the reach of the tax authorities.”

Keith Gordon said HMRC is targeting individuals because it is easier

Loan charge has ‘no legal basis’

MPs and tax lawyers are calling for HMRC to rescind the policy – arguing that it amounts to a retrospective charge that overrides taxpayers’ statutory protections by effectively dismissing time limits on HMRC’s right to investigate tax affairs and by blocking individuals’ rights to fight their case in court.

It is also without any legal precedent.

The courts have repeatedly rejected HMRC’s interpretation that income tax can be applied on loans to individuals.

A 2017 Supreme Court ruling put the onus on the employer to deduct income tax before loans were advanced to an individual.

A 2019 parliamentary report concluded that “the loan charge is in defiance of the rulings of the court… no court case has given the legal basis for the loan charge”.

MPs are preparing to debate the loan charge in parliament today, where they will hear that tens of thousands of people were the victims of widespread mis-selling.

They will question why HMRC is not putting more energy into targeting the promoters and companies responsible for these schemes.

These companies made their money by charging individuals a fee to run the loan schemes. It meant that in many cases people had similar deductions to what they would have had if they were under PAYE.

David Davis, Conservative MP for Haltemprice and Howden, said: “The loan charge has been, frankly, a government-sponsored disaster for a very large number of people, ordinary decent people, nurses and other ordinary people who were faced with a work contract that denied them any employment rights, told them they had to accept and that was the basis on which they got the job.”

He added that HMRC should “go back to the promoters, go back to the contractors who insisted on these terms and say, ‘you can pay at least your share, if not the whole bill’, but they’re not doing that. And I’m afraid in my view, they’ve made a massive ethical error in not doing so”.

An HMRC spokesperson said: “The loan charge seeks to recover tax that has been avoided by disguising income as loans. It is our responsibility to collect the tax that people owe.

“We take the wellbeing of all taxpayers very seriously and recognise that dealing with large tax liabilities can lead to pressure on individuals.

“The support we have in place to help people settle their previous tax avoidance includes offering payment by instalments: these arrangements are based on what the taxpayer can afford, and there’s no upper limit over how long we can spread payments.

“Our message to anyone who is worried about paying what they owe is: please contact us as soon as possible to talk about options.

“Above all we want to prevent people getting into these types of situations and our message is clear – if a tax scheme sounds too good to be true, it probably is.”

Business

Claire’s to appoint administrators for UK and Ireland business – putting thousands of jobs at risk

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike