How fiscal headroom has come to dominate Westminster and why it could decide the next election

“Fiscal headroom”. It is a desperately boring term, meaningless to many. Yet this bit of economic jargon may well have the power to swing the next election.

It is thanks to fiscal headroom that the chancellor may be able to splurge on billions of pounds of tax cuts in the coming months, hoping to lift the Conservatives’ sagging polls. It is on the basis of “fiscal headroom” that Sir Keir Starmer will decide whether he can go ahead with his much-vaunted plans to invest untold amounts in Britain’s energy sector.

All of which raises a rather important question – what is fiscal headroom anyway?

Happily, the explanation is quite simple. When politicians talk about fiscal headroom they are mostly talking about something quite specific; the room they have to spend money before they break their fiscal rules.

Ever since Gordon Brown, successive chancellors have imposed rules to discipline their borrowing. These rules have changed over time – mostly when the chancellor of the day realised he was about to break them. Today’s chancellor, Jeremy Hunt, has a few such rules but the most important one – the one he and pretty much everyone pays most attention to – is the rule about the national debt.

This rule states that he has to show that he is bringing down Britain’s net debt (in other words, the amount the state owes) as a percentage of gross domestic product (GDP) within five years.

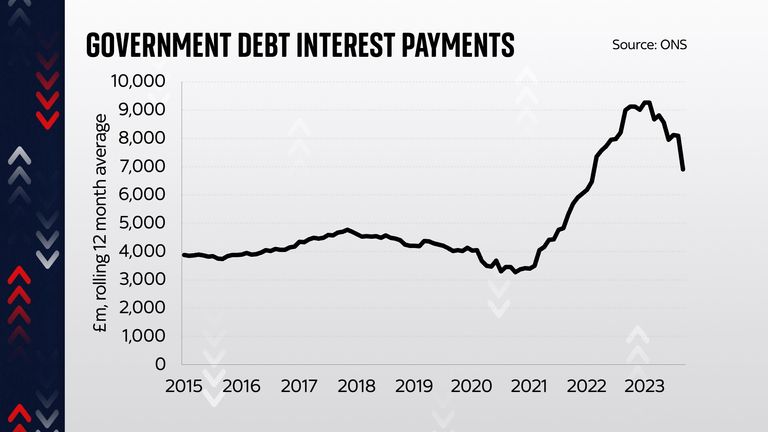

There is plenty of logic in trying to keep the national debt under control. While there’s no hard and fast rule about precisely what level of debt is “safe” or not, there are many episodes throughout history of countries getting into big economic trouble when they allow their national debt to rise too high (since it often means higher debt interest payments, which can spiral out of control).

The fiscal equivalent of St Augustine’s prayer

But it’s also worth pointing out at this point that this rule is actually a lot less strict than it might at first sound. It’s not saying “bring the debt down immediately”. It’s saying “you can absolutely increase the national debt if you want to, provided it looks like it’s on the way down five years from now”. It is the fiscal equivalent of St Augustine’s prayer: “Lord, make me good. But not yet.”

And the current government plans aim to do precisely that. The figures in last November’s autumn statement show that its preferred measure of the national debt (there are many – don’t ask) actually rises in the coming years, from 90.2% of GDP in 2023/24 up to 95% of GDP by 2026/27.

Only in the following years does it start to fall, quite gradually, to 94.9% of GDP in 2027/28 and then to 94.4% of GDP in 2028/29. And, since it’s falling, the debt rule is met. Hurrah!

If at this point you’re still following, you’ve probably noticed a few things.

First, these supposedly strict fiscal rules aren’t actually stopping the national debt from rising. It’ll be considerably higher in five years’ time than it is today.

Second, the rate at which the debt is falling towards the end of this decade is actually quite slow.

Third, we seem to be fixating quite a lot on a couple of years (the difference between 2027/28 and 2028/29) which are a long way away, way beyond the government’s current spending plans.

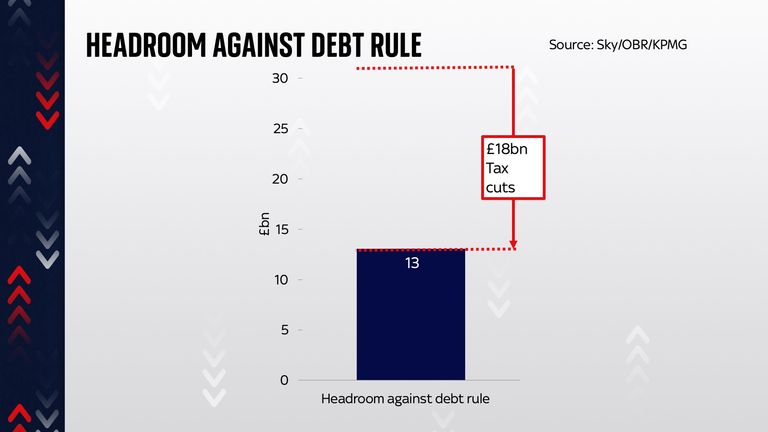

And you’re right on all three. But no matter, because if all you care about is fiscal headroom, all that matters is the difference between those two figures, 94.9% of GDP and 94.4% of GDP. And that difference works out, in actual money, at about £13bn.

A made-up rule

Now, I could have easily skipped the preceding paragraphs and begun this article with this fact. Headroom equals £13bn. That, after all, is what most of Westminster does.

But every so often context can come in useful, and in this case the context underlines something important. Namely, that headroom is not an immutable law of economics. It is the product of a self-imposed rule. It is, to put it more bluntly, made up.

But this made-up number has an enormous bearing on economic policy right now. Since both the Conservatives and Labour have adopted the same fiscal rule, they also find themselves having to bend their knee to the god of headroom.

Jeremy Hunt says he won’t spend any more than the headroom he has at the next budget. Which, to translate, means he’ll probably spend nearly all the billions of headroom he has. Rachel Reeves says while she would like to invest £28bn on green energy technology projects, she won’t do it if it breaks the fiscal rules.

So the questions of how many tax cuts the chancellor offers this year and how much Labour will invest in the energy transition both hang on this made-up number. Indeed, the two things are related, since if Mr Hunt splurges a lot in the coming months, there’s no headroom left for Ms Reeves if she gets into office.

One of the single most important numbers in politics

Some would say this is all a bit silly. And they might just have a point. But since both main parties have agreed to respect this concept of headroom, it is among the single most important numbers in politics right now.

Yet here’s the other thing. What looks like a monolithic number is actually changing all the time. Since “fiscal headroom” is actually the difference between two other big numbers (the national debt four years hence, minus the national debt five years hence) which change quite a lot when the economy gets bigger or smaller or taxes come in faster than expected, it has a tendency to yo-yo around from one year to the next.

Consider this – last March, the Office for Budget Responsibility (OBR) was saying the amount of headroom was a mere £6bn. Not much, in other words.

But then, at the autumn statement, we learned that the public finances turned out to be in a better state than expected. That, plus the fact that there was an extra year until the deadline, increased the potential headroom by nearly £25bn in one fell swoop. So what looked like £6bn in headroom actually turned out to be £31bn of headroom.

All of which is why the chancellor was able to splurge £18bn in November (on those National Insurance cuts) and to leave us still with a supposed £13bn headroom this time around.

And something similar is likely to happen again when we get to March’s spring budget. The public finances are looking a bit healthier than expected. This morning’s public finance figures showed the deficit and debt interest payments were both lower than anticipated.

The upshot is that most economists think that £13bn of headroom could actually be anywhere up to £23bn. So there’s more money for the chancellor to spend, should he see fit.

It’s possible that at this point your head is spinning. Perhaps you’re wondering why on earth Westminster is tying itself in knots to stay true to a fiscal rule which was only made up a few years ago. Perhaps you’re wondering why the future of this economy hangs not on the question of the smartest long-term policy but on the difference between a few decimal places on a spreadsheet produced by the OBR.

These are all good questions. But mentioning them in Whitehall these days is tantamount to blasphemy. Trust, instead, in the creed of fiscal headroom. Everyone else is.

If you ever fly to Washington DC, look out of the window as you land at Dulles Airport – and you might snatch a glimpse of the single biggest story in economics right now.

There below you, you will see scattered around the fields and woods of the local area a set of vast warehouses that might to the untrained eye look like supermarkets or distribution centres. But no: these are in fact data centres – the biggest concentration of data centres anywhere in the world.

For this area surrounding Dulles Airport has more of these buildings, housing computer servers that do the calculations to train and run artificial intelligence (AI), than anywhere else. And since AI accounts for the vast majority of economic growth in the US so far this year, that makes this place an enormous deal.

Down at ground level you can see the hallmarks as you drive around what is known as “data centre alley”. There are enormous power lines everywhere – a reminder that running these plants is an incredibly energy-intensive task.

This tiny area alone, Loudoun County, consumes roughly 4.9 gigawatts of power – more than the entire consumption of Denmark. That number has already tripled in the past six years, and is due to be catapulted ever higher in the coming years.

Inside ‘data centre alley’

We know as much because we have gained rare access into the heart of “data centre alley”, into two sites run by Digital Realty, one of the biggest datacentre companies in the world. It runs servers that power nearly all the major AI and cloud services in the world. If you send a request to one of those models or search engines there’s a good chance you’ve unknowingly used their machines yourself.

Inside a site run by Digital Realty

Their Digital Dulles site, under construction right now, is due to consume up to a gigawatt in power all told, with six substations to help provide that power. Indeed, it consumes about the same amount of power as a large nuclear power plant.

Walking through the site, a series of large warehouses, some already equipped with rows and rows of backup generators, there to ensure the silicon chips whirring away inside never lose power, is a striking experience – a reminder of the physical underpinnings of the AI age. For all that this technology feels weightless, it has enormous physical demands. It entails the construction of these massive concrete buildings, each of which needs enormous amounts of power and water to keep the servers cool.

Sky’s Ed Conway at the data centre

Read more from Ed Conway:

Blow to UK’s bid to become minerals superpower

There’s more to your AirPods than meets the eye

We were given access inside one of the company’s existing server centres – behind multiple security cordons into rooms only accessible with fingerprint identification. And there we saw the infrastructure necessary to keep those AI chips running. We saw an Nvidia DGX H100 running away, in a server rack capable of sucking in more power than a small village. We saw the cooling pipes running in and out of the building, as well as the ones which feed coolant into the GPUs (graphic processing units) themselves.

Such things underline that to the extent that AI has brainpower, it is provided not out of thin air, but via very physical amenities and infrastructure. And the availability of that infrastructure is one of the main limiting factors for this economic boom in the coming years.

According to economist Jason Furman, once you subtract AI and related technologies, the US economy barely grew at all in the first half of this year. So much is riding on this. But there are some who question whether the US is going to be able to construct power plants quickly enough to fuel this boom.

Is Trump’s AI plan a ‘tech bro’ manifesto?

For years, American power consumption remained more or less flat. That has changed rapidly in the past couple of years. Now, AI companies have made grand promises about future computing power, but that depends on being able to plug those chips into the grid.

Last week the International Monetary Fund’s chief economist, Pierre-Olivier Gourinchas, warned AI could indeed be a financial bubble.

He said: “There are echoes in the current tech investment surge of the dot-com boom of the late 1990s. It was the internet then… it is AI now. We’re seeing surging valuations, booming investment and strong consumption on the back of solid capital gains. The risk is that with stronger investment and consumption, a tighter monetary policy will be needed to contain price pressures. This is what happened in the late 1990s.”

‘The terrifying thing is…’

For those inside the AI world, this also feels like uncharted territory.

Helen Toner, executive director of Georgetown’s Center for Security and Emerging Technology, and formerly on the OpenAI board, said: “The terrifying thing is: no one knows how much further AI is going to go, and no one really knows how much economic growth is going to come out of it.

“The trends have certainly been that the AI systems we are developing get more and more sophisticated over time, and I don’t see signs of that stopping. I think they’ll keep getting more advanced. But the question of how much productivity growth will that create? How will that compare to the absolutely gobsmacking investments that are being made today?”

Whether it’s a new industrial revolution or a bubble – or both – there’s no denying AI is a massive economic story with massive implications.

For energy. For materials. For jobs. We just don’t know how massive yet.

Business

Pizza Hut to shut 68 restaurants in UK after company behind venues falls into administration

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024