How fiscal headroom has come to dominate Westminster and why it could decide the next election

“Fiscal headroom”. It is a desperately boring term, meaningless to many. Yet this bit of economic jargon may well have the power to swing the next election.

It is thanks to fiscal headroom that the chancellor may be able to splurge on billions of pounds of tax cuts in the coming months, hoping to lift the Conservatives’ sagging polls. It is on the basis of “fiscal headroom” that Sir Keir Starmer will decide whether he can go ahead with his much-vaunted plans to invest untold amounts in Britain’s energy sector.

All of which raises a rather important question – what is fiscal headroom anyway?

Happily, the explanation is quite simple. When politicians talk about fiscal headroom they are mostly talking about something quite specific; the room they have to spend money before they break their fiscal rules.

Ever since Gordon Brown, successive chancellors have imposed rules to discipline their borrowing. These rules have changed over time – mostly when the chancellor of the day realised he was about to break them. Today’s chancellor, Jeremy Hunt, has a few such rules but the most important one – the one he and pretty much everyone pays most attention to – is the rule about the national debt.

This rule states that he has to show that he is bringing down Britain’s net debt (in other words, the amount the state owes) as a percentage of gross domestic product (GDP) within five years.

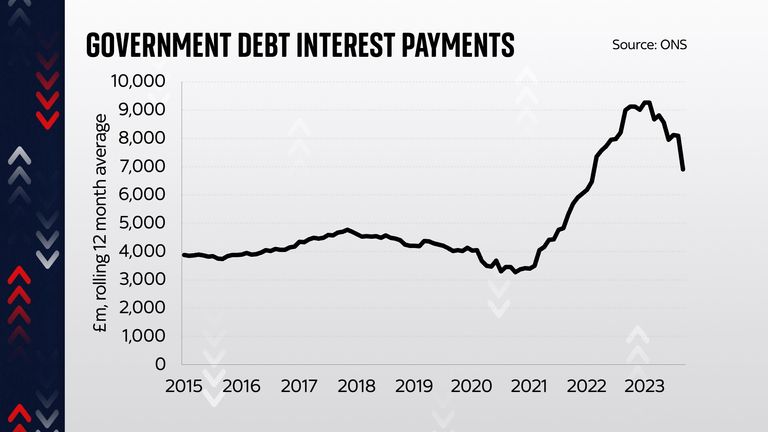

There is plenty of logic in trying to keep the national debt under control. While there’s no hard and fast rule about precisely what level of debt is “safe” or not, there are many episodes throughout history of countries getting into big economic trouble when they allow their national debt to rise too high (since it often means higher debt interest payments, which can spiral out of control).

The fiscal equivalent of St Augustine’s prayer

But it’s also worth pointing out at this point that this rule is actually a lot less strict than it might at first sound. It’s not saying “bring the debt down immediately”. It’s saying “you can absolutely increase the national debt if you want to, provided it looks like it’s on the way down five years from now”. It is the fiscal equivalent of St Augustine’s prayer: “Lord, make me good. But not yet.”

And the current government plans aim to do precisely that. The figures in last November’s autumn statement show that its preferred measure of the national debt (there are many – don’t ask) actually rises in the coming years, from 90.2% of GDP in 2023/24 up to 95% of GDP by 2026/27.

Only in the following years does it start to fall, quite gradually, to 94.9% of GDP in 2027/28 and then to 94.4% of GDP in 2028/29. And, since it’s falling, the debt rule is met. Hurrah!

If at this point you’re still following, you’ve probably noticed a few things.

First, these supposedly strict fiscal rules aren’t actually stopping the national debt from rising. It’ll be considerably higher in five years’ time than it is today.

Second, the rate at which the debt is falling towards the end of this decade is actually quite slow.

Third, we seem to be fixating quite a lot on a couple of years (the difference between 2027/28 and 2028/29) which are a long way away, way beyond the government’s current spending plans.

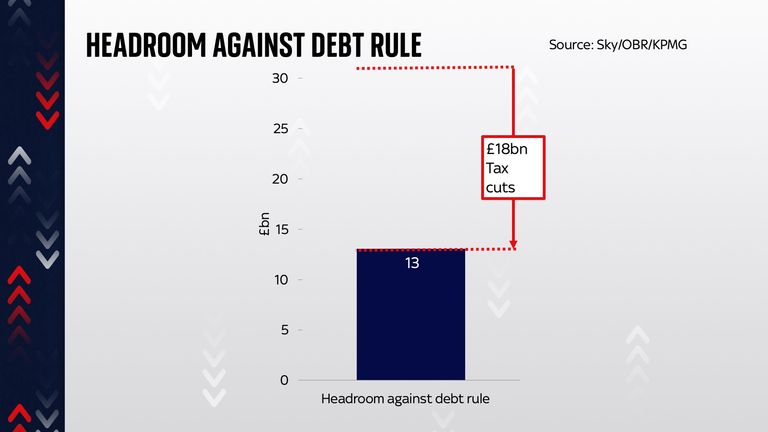

And you’re right on all three. But no matter, because if all you care about is fiscal headroom, all that matters is the difference between those two figures, 94.9% of GDP and 94.4% of GDP. And that difference works out, in actual money, at about £13bn.

A made-up rule

Now, I could have easily skipped the preceding paragraphs and begun this article with this fact. Headroom equals £13bn. That, after all, is what most of Westminster does.

But every so often context can come in useful, and in this case the context underlines something important. Namely, that headroom is not an immutable law of economics. It is the product of a self-imposed rule. It is, to put it more bluntly, made up.

But this made-up number has an enormous bearing on economic policy right now. Since both the Conservatives and Labour have adopted the same fiscal rule, they also find themselves having to bend their knee to the god of headroom.

Jeremy Hunt says he won’t spend any more than the headroom he has at the next budget. Which, to translate, means he’ll probably spend nearly all the billions of headroom he has. Rachel Reeves says while she would like to invest £28bn on green energy technology projects, she won’t do it if it breaks the fiscal rules.

So the questions of how many tax cuts the chancellor offers this year and how much Labour will invest in the energy transition both hang on this made-up number. Indeed, the two things are related, since if Mr Hunt splurges a lot in the coming months, there’s no headroom left for Ms Reeves if she gets into office.

One of the single most important numbers in politics

Some would say this is all a bit silly. And they might just have a point. But since both main parties have agreed to respect this concept of headroom, it is among the single most important numbers in politics right now.

Yet here’s the other thing. What looks like a monolithic number is actually changing all the time. Since “fiscal headroom” is actually the difference between two other big numbers (the national debt four years hence, minus the national debt five years hence) which change quite a lot when the economy gets bigger or smaller or taxes come in faster than expected, it has a tendency to yo-yo around from one year to the next.

Consider this – last March, the Office for Budget Responsibility (OBR) was saying the amount of headroom was a mere £6bn. Not much, in other words.

But then, at the autumn statement, we learned that the public finances turned out to be in a better state than expected. That, plus the fact that there was an extra year until the deadline, increased the potential headroom by nearly £25bn in one fell swoop. So what looked like £6bn in headroom actually turned out to be £31bn of headroom.

All of which is why the chancellor was able to splurge £18bn in November (on those National Insurance cuts) and to leave us still with a supposed £13bn headroom this time around.

And something similar is likely to happen again when we get to March’s spring budget. The public finances are looking a bit healthier than expected. This morning’s public finance figures showed the deficit and debt interest payments were both lower than anticipated.

The upshot is that most economists think that £13bn of headroom could actually be anywhere up to £23bn. So there’s more money for the chancellor to spend, should he see fit.

It’s possible that at this point your head is spinning. Perhaps you’re wondering why on earth Westminster is tying itself in knots to stay true to a fiscal rule which was only made up a few years ago. Perhaps you’re wondering why the future of this economy hangs not on the question of the smartest long-term policy but on the difference between a few decimal places on a spreadsheet produced by the OBR.

These are all good questions. But mentioning them in Whitehall these days is tantamount to blasphemy. Trust, instead, in the creed of fiscal headroom. Everyone else is.

Business

Vivergo: How US-UK trade deal could bring about collapse of huge renewable energy plant in Hull

The smell of yeast still hangs in the air at the Vivergo plant in Hull but the machines have fallen quiet.

More than 100 lorries usually pass through here each day, carrying 3,000 tonnes of wheat. It is milled, fermented and distilled. The final product is bioethanol, a renewable fuel that is then blended into E10 petrol.

This is a vast operation. It took several years to build, with considerable investment, but it is on the verge of closing down. Management and staff are holding out for a last-minute reprieve from the government but time is running out.

It’s been a turbulent journey. The plant was already being annihilated by US rivals, losing about £3m a month. Vivergo and Ensus, based in Teesside, blamed regulations that enable US companies to earn double subsidies.

They were pushing for regulatory change but then a killer blow: The US-UK trade deal, which allows 1.4 billion litres of American ethanol into the UK tariff-free (down from 19%).

“We’ve effectively given the whole of the UK market to the US producers,” said Ben Hackett, managing director at Vivergo.

“If we were to have the same support that the US industry has, if we could use genetically modified crops, we wouldn’t need that tariff. We would be able to compete. If we had the same energy costs. We wouldn’t need those tariffs.”

The government has the weekend to come up with a plan that could keep the business running. If it fails, Vivergo will begin issuing redundancy notices to its 160 staff.

Ben Hackett

It’s a devastating prospect for workers, many of them live in Hull and are nervous about alternative opportunities in the area.

Mike Walsh, a logistics manager who has been working at the plant for 14 years, said: “It’s not a great place to be at the moment. It’s a very well paid, very high-skilled role and they’ve (Vivergo) given everybody an opportunity in an area that doesn’t pay that well…. The jobs market isn’t as good as what people would like. So it does impact the local economy.”

He called on the government to “help us, save us, give this industry a future”.

His colleague Claire Wood, lead productions engineer, said: “I moved here after a career in oil and gas for 10 years, partly because I want to be part of the transition to renewable fuels. I can see so much potential here and it’s absolutely devastating to know that this place might be closed very, very shortly and that all that potential just goes away.”

Thousands more could be affected. Haulage companies may have to lay off truck drivers and farmers could also suffer a blow.

Vivergo makes bioethanol using wheat. That wheat is bought from farms from Yorkshire and Lincolnshire.

Claire Wood

The National Farmers Union has sounded the alarm, saying: “Biofuels are extremely important for the crops sector, and their domestic demand of up to two million tonnes can be very important to balance supply and demand and to produce up to one million tonnes of animal feed as a by-product.”

Another bioproduct is carbon dioxide. The gas can be captured and used to put the fizz in drinks or injected into packaging to preserve food.

If Vivergo and Ensus were to go, Britain would lose as much as 80% of its output of carbon dioxide. Supplies are already tight across Europe, meaning this decision could compound shortages across a range of sectors, from meat-packing to healthcare.

The industry is calling on the government to help. Vivergo says it needs temporary financial support but that the government must create a regulatory and commercial environment in which it can thrive.

It says rules that award double subsidies to companies that use waste product in their bioethanol must be changed. At present, these rules are being used by US companies that make ethanol from Uldr – a by-product of processing corn. They argue this is not a genuine waste product.

Read more money news:

Something for everyone in latest economic data

Claire’s falls into administration

Lola’s Cupcakes bakes £30m takeover by Finsbury Food

Another option is to grow the market. Industry leaders are calling on ministers to increase the mandated renewable fuel content in petrol from 10% to 15% and for an expansion into aviation fuels. That would allow British companies to carve out a space.

The government has been locked in talks with the company since June.

It said: “We will continue to take proactive steps to address the long-standing challenges it faces and remain committed to a way forward that protects supply chains, jobs and livelihoods.”

However, the time for talking is almost over.

Mr Hackett said he had no idea how the government would respond but he was firm with his stance, saying: “In times of global uncertainty, losing that energy certainty and supply from the UK is a problem.

“I think what they’re missing out on is the future growth agenda. We’re the foundation on which the green industrial strategy can be built. We make bioethanol that today decarbonises transport. Tomorrow it will decarbonise marine. It will decarbonise aviation.”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike