Loan charge: HMRC accused of ‘dangerous and sinister’ new tactics in tax crackdown linked to 10 suicides

HMRC has been accused of using “dangerous and sinister” new tactics in a tax crackdown that has already been linked to 10 suicides.

The government has recently come under pressure over the “Loan Charge” – controversial legislation which made tens of thousands of contractors who were paid their salaries through loans retrospectively liable for tax their employer should have paid.

The clampdown has been branded on par with the Post Office Horizon scandal as the unaffordable bills have been linked to suicides and bankruptcies, while one woman had an abortion due to the financial strain she was under, a debate in parliament heard last month.

HMRC has been criticised for going after individuals – including teachers, nurses and cleaners – rather than the firms that profited from promoting the schemes as tax compliant.

Politics Live: MPs return to Westminster after double by-election defeat for Sunak

However ministers have resisted pressure to overturn the policy, saying a review conducted by Lord Morse in 2019 resulted in a series of reforms to reduce the financial pressures of the some 50,000 people affected.

Crucially this included cutting the policy’s 20-year retrospective period so only loans received after December 2010 were in scope.

However it has emerged that HMRC have been pursuing people involved in loan schemes prior to 2010 through a different mechanism – a s684 notice.

This effectively gives HMRC the discretion to transfer a tax burden from an employer to an employee for the tax years excluded from the Loan Charge.

Conservative MP Greg Smith, co-chair of the Loan Charge APPG, said it “flies in the face” of what Lord Morse intended and risks more people taking their own lives because of the unaffordable bills.

Loan scheme causing tax turmoil

‘I could lose my home’

Sky News spoke to people who said they had experienced suicidal thoughts and feared becoming homeless after unexpectedly receiving the notices.

While the s684s don’t state how much tax is owed, one father-of-three said his bill could be as high as £250,000 as this is how much HMRC have previously tried to claw back from his time in a loan scheme pre-2010.

The IT consultant, who asked to remain anonymous, said he attempted to settle his tax affairs years ago but communication with the tax office “fizzled out” and following the Morse review he believed the “nightmare” was behind him.

Then in November he received a brown envelope containing an s684 and now he is worried HMRC is “going to absolutely hammer me” just as he is approaching retirement age.

“I have three children and in the worst case scenario I will lose my home.

“I can’t think of another government policy that has caused so much suffering. I fear this could really push some people over the edge.”

Wreathes to honour the suicides linked to the tax crackdown. There have now been 10 confirmed by HMRC

‘Dreadful landscape’

It is not clear how many people have been sent the notices.

The government previously estimated that 11,000 people would be removed from the Loan Charge by introducing the 2010 cut off.

While the Loan Charge is seen as particularly punitive because it adds together all outstanding loans and taxes them in a single year, often at the 45% rate, the notices mean HMRC can use its own discretion to turn off an employer’s PAYE obligations and seek the income tax that would have been due that year from the employee instead.

Rhys Thomas, director of the WTT tax firm, told Sky News: “There is considerable and understandable confusion amongst taxpayers that when the Morse review removed the loan charge for payments pre 9th December 2010, it was assumed that HMRC had no further recourse for those years.

“Where enquiries were outstanding for the earlier tax years, HMRC will seek to conclude these by utilising tools such as s684 notices.”

He called the situation a “dreadful landscape” as those in receipt of the notices only have 30 days to respond to HMRC over something “that has taken them 15 years to investigate”.

Click to subscribe to the Sky News Daily wherever you get your podcasts

There is no right to appeal the notices, so the only way to challenge HMRC is through a costly Judicial Review.

“It’s causing a huge amount of distress and anxiety; it’s hugely concerning and for lots of people it’s come as a surprise,” Mr Thomas said.

WTT is representing around 200 people who are challenging the notices, saying HMRC has not done enough to go after the core parties who should have collected the tax at the time.

A spokesperson for HMRC said the Morse Review “recommend we use our normal powers to investigate and settle cases taken out of the Loan Charge”.

They said they had been issuing the notices since May 2022, having won a case at the Court of Appeal over their use in relation to loan schemes, “so it’s not a sudden change”.

But campaigners disputed the use of the notices as “normal” and said it is another example of HMRC “abusing its power” to go after individuals rather than the companies that ran and promoted the loan schemes.

Money latest: The countries where retirement age is 58 – and those where it’s 67

‘We were mis-sold’

These became prolific in the 2000s and saw self-employed contractors encouraged to join umbrella companies that paid them their salaries through loans which were not typically paid back.

HMRC has argued those who signed up to the schemes are tax evaders who need to pay their fair share. But those affected claim they are victims of mis-selling as the arrangements were widely marketed as legitimate by the scheme promoters and tax advisers, and in some cases they had no choice but to be paid this way.

IT consultant Daniel (not his real name), from Stoke, said he did not stand to make any money from the scheme he joined in 2008 and was simply trying to avoid falling foul of complex off-payroll rules known as IR35.

His tax adviser said the scheme was HMRC compliant and the company said they “would sort out my taxes”, he added.

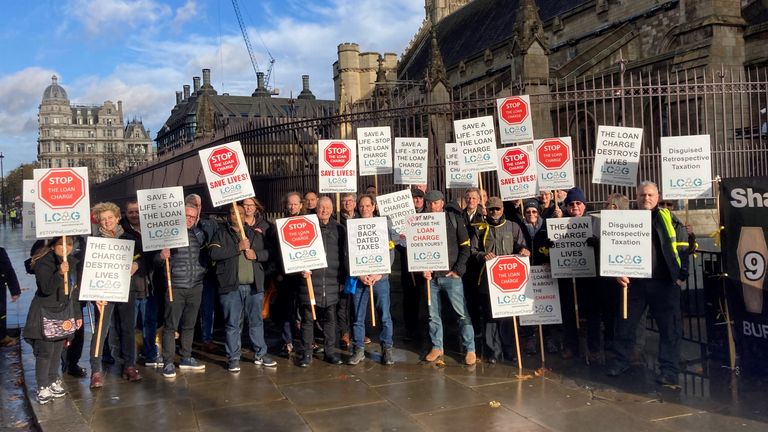

Loan Charge protest

He said he “did not hear a peep” from HMRC during his time in the scheme and his payslip looked normal as around 20% was being deducted from his salary each month – money experts say will have gone into the profits of those running the company rather than tax to the exchequer.

Now, he is expecting a £30,000 bill after receiving an s684 in November – cash the father-of-four “does not have”.

“If I felt like I had done something wrong I would accept it but I did not make one penny from this scheme, it was all to do with compliance and to make my life as simple as possible.

“This is causing so much stress and frustration. I have had plenty of sleepless nights.

“It feels like the Post Office scandal where we are the little people being backed into a corner and there’s nothing we can do and those who are really guilty are just laughing.”

Read More:

Post Office scandal: New concerns raised over second IT system used in branches

Buying a flat ruined my life’: Leaseholders plead for tougher legislation against home ownership ‘scam’

HMRC ‘abusing its powers’

The notices have renewed calls for the government to find a new solution to the Loan Charge scandal.

Keith Gordon, a tax barrister, said HMRC “is effectively responsible for this mess because they failed to warn employees that they did not like these schemes”.

Keith Gordon said HMRC is targeting individuals because it is an easier way of recouping the money

“Most people, if they got a whiff of HMRC dislike, would have left these schemes but they were sold it as being tax compliant. Why should the blame be on people who were at the very worst merely naïve?”

Campaigners fear the s684s will be used across the board instead of the Loan Charge, which Labour has said it will review if it wins the next election.

Steve Packham, of the Loan Charge Action Group, accused HMRC of being “downright reckless” in light of the 10 confirmed suicides, adding: “This is sinister and dangerous and is another example of how out-of-control HMRC is.

“The government must immediately order a stop to these notices and instead agree to find a resolution to the Loan Charge Scandal before there are more lives ruined.”

Greg Smith, co-chair of the Loan Charge Action and Taxpayer Fairness APPG. Pic: PA

A HMRC spokesperson said: “We appreciate there’s a human story behind every tax bill and we take the wellbeing of all taxpayers seriously.

“We recognise dealing with large tax liabilities can lead to pressure on individuals and we are committed to supporting customers who need extra help with their tax liabilities. We have made significant improvements to this service over the last few years.

“Our message to anyone who is worried about paying what they owe is: please contact us as soon as possible to talk about your options.”

Anyone feeling emotionally distressed or suicidal can call Samaritans for help on 116 123 or email jo@samaritans.org in the UK.

The chair of the Labour Party has insisted that Sir Keir Starmer will “absolutely” still be prime minister next Christmas, despite the party’s dire position in the polls.

Speaking to Sky’s Sunday Morning With Trevor Phillips, Anna Turley acknowledged that “things are still hard” for Britons, but struck an optimistic tone about the year ahead.

She said the government has “taken a lot of difficult decisions this year” to “stabilise the economy”, but we are now “starting to see that recovery”.

“As we go into the new year, I’m really optimistic about delivering the kind of change that people voted for last year, and to see them starting to see and feel it in their pockets and in their local communities,” Ms Turley insisted.

On average over the last 10 polls, the Labour Party is down in third place on 18.2%, while Reform UK is on 29.4%, and the Conservative Party is on 18.9%.

Trevor then asked if the public simply hasn’t noticed “how lucky they’ve been”, and the senior minister said: “Well, I think rightly, people are impatient for change. We all are. And people voted for change – that was on the front of our manifesto last year.

“But it takes time to deliver that. It takes time to stabilise things from the chaos that we inherited.”

She said fundamental changes, particularly those that require legislation, take time to deliver, pointing to the Employment Rights Bill, which only passed through parliament last week after the Lords repeatedly sought to amend it.

Ms Turley continued: “We live in the real world. We know things are still hard.

“But I’m conscious with every single day that goes by next year, people will really start to see and feel more money in their pockets, better public services when they’re looking for an appointment with a doctor, their streets and the neighbourhoods are looking better and better, and that change takes time.

“But we will be delivering that in the new year, and I’m confident people can really start to see that.”

Sir Keir Starmer is under pressure amid Labour’s dire position in the polls. Pic: PA

Asked directly if Sir Keir Starmer will be Labour leader and prime minister by next Christmas, Turley replied: “Of course. Absolutely.

“As I said, people will really start to see and feel the change in their pockets. He has got a very clear vision for making sure that people can really deal with the cost of living, that public services will get back on their […] feet.

“And he’s building a Britain that is one that is tolerant, that is open, that is confident in itself. And that is really about renewal and investment in young people as opposed to the division and the decline of the opposition.”

Read more:

Over half of Labour members want to ditch Starmer

Almost two in three Labour members back Burnham

Over a third of Britons think Reeves exaggerated bad news

Her backing of the prime minister comes amid continued unease on the Labour benches about the party’s position in the polls, and the manoeuvrings of some big figures who are rumoured to be plotting a move against the prime minister if May’s local elections go badly.

One such person thought to be preparing for a potential leadership bid is the health secretary, Wes Streeting, who has told The Observer today that he is not ruling himself out as a candidate for the top job in future.

“I’m diplomatically ducking the question to avoid any more of the silly soap opera we’ve had in the last few months,” Streeting said, despite also noting the “pressure” and the “demands of that job”.

Greater Manchester mayor Andy Burnham is repeatedly refusing to rule out a return to Westminster to challenge Sir Keir for the Labour leadership, and former deputy prime minister Angela Rayner is thought to be preparing to potentially launch a leadership bid of her own.

‘We’re going to smash the local elections’

Also on Sunday Morning With Trevor Phillips, the Conservative Party deputy chair, Matt Vickers, was bullish about his party’s prospects at May’s local elections.

“We’re going to go out there and smash these next elections,” he said.

“The reality is we had a tough general election. If anybody thought that we were going to dust ourselves off and be back in the game within months, then they’re a bit mad.”

US lawmakers have introduced a discussion draft that would ease the tax burden on everyday crypto users by exempting small stablecoin transactions from capital gains taxes and offering a new deferral option for staking and mining rewards.

The proposal, introduced by Representatives Max Miller of Ohio and Steven Horsford of Nevada, seeks to amend the Internal Revenue Code to reflect the growing use of digital assets in payments. The draft is set “to eliminate low-value gain recognition arising from routine consumer payment use of regulated payment stablecoins,” per the draft.

Under the draft, users would not be required to recognize gains or losses on stablecoin transactions of up to $200, provided the asset is issued by a permitted issuer under the GENIUS Act, pegged to the US dollar and maintains a tight trading range around $1.

The bill includes safeguards to prevent abuse. The exemption would not apply if a stablecoin trades outside a narrow price band, and brokers or dealers would be excluded from the benefit. Treasury would also retain authority to issue anti-abuse rules and reporting requirements.

Related: Crypto Biz: Bank stablecoins get a rulebook; Bitcoin gets a land grab

US bill defers taxes on crypto staking rewards

Beyond payments, the proposal addresses long-standing concerns around “phantom income” from staking and mining. Taxpayers would be allowed to elect to defer income recognition on staking or mining rewards for up to five years, rather than being taxed immediately upon receipt.

“This provision is intended to reflect a necessary compromise between immediate taxation upon dominion & control and full deferral until disposition,” the draft said.

The draft also extends existing securities lending tax treatment to certain digital asset lending arrangements, applies wash sale rules to actively traded crypto assets, and allows traders and dealers to elect mark-to-market accounting for digital assets.

Related: Galaxy predicts stablecoins will overtake ACH transaction volume in 2026

Crypto groups urge Senate to rethink stablecoin rewards ban

Last week, the Blockchain Association sent a letter to the US Senate Banking Committee, signed by more than 125 crypto companies and industry groups, opposing efforts to extend restrictions on stablecoin rewards to third-party platforms.

The group argued that expanding the GENIUS Act’s limits beyond stablecoin issuers would curb innovation and increase market concentration in favor of large incumbents. The letter compared crypto rewards to incentives commonly offered by banks and credit card companies, warning that banning similar features for stablecoins would undermine fair competition.

Magazine: 2026 is the year of pragmatic privacy in crypto — Canton, Zcash and more

Politics

Watchdog criticises ‘unprecedented’ government offer to delay local elections – as five councils confirm requests for postponement

The elections watchdog has criticised the government for offering to consider delaying 63 local council elections next year – as five authorities confirmed to Sky News that they would ask for a postponement.

On Thursday, hours before parliament began its Christmas recess, the government revealed that councils were being sent a letter asking if they thought elections should be delayed in their areas due to challenges around delivering local government reorganisation plans.

The chief executive of the Electoral Commission, Vijay Rangarajan, hit out at the announcement on Friday, saying he was “concerned” that some elections could be postponed, with some having already been deferred from 2025.

“We are disappointed by both the timing and substance of the statement. Scheduled elections should, as a rule, go ahead as planned, and only be postponed in exceptional circumstances,” he said in a statement.

“Decisions on any postponements will not be taken until mid-January, less than three months before the scheduled May 2026 elections are due to begin.

“This uncertainty is unprecedented and will not help campaigners and administrators who need time to prepare for their important roles.”

Mr Rangarajan added: “We very much recognise the pressures on local government, but these late changes do not help administrators. Parties and candidates have already been preparing for some time, and will be understandably concerned.”

He said “capacity constraints” were not a “legitimate reason for delaying long planned elections”, which risked “affecting the legitimacy of local decision-making and damaging public confidence”.

The watchdog chief also said there was “a clear conflict of interest in asking existing councils to decide how long it will be before they are answerable to voters”.

Sky News contacted the 63 councils that have been sent the letter about potentially delaying their elections.

At the time of publication, 17 authorities had replied with their decisions, while 33 said they would make up their minds before the government’s deadline of 15 January.

Many councils told Sky News they were surprised at yesterday’s announcement, saying that they had been fully intending to hold their polls as scheduled.

They said they were now working to understand the appropriate democratic mechanism for deciding whether to request a postponement of elections. Some local authorities believe it should be a decision made by their full council, while others will leave it up to council leaders or cabinet members to decide.

Multiple councils also emphasised in statements to Sky News that the ultimate decision to delay elections lay with the government.

Reform UK has threatened legal action against ministers, accusing Labour and the Tories of “colluding” to postpone elections in order to lock other parties out of power – a sentiment echoed by Liberal Democrat leader Sir Ed Davey.

But shadow local government secretary Sir James Cleverly told Sky News this morning that the Conservative Party “wants these elections to go ahead”. Sky News understands that the national party is making that position clear to local leaders.

A spokesperson for the Ministry of Housing, Communities, and Local Government, said it was taking a “locally-led approach”, and emphasised that “councils are in the best position to judge the impact of postponements on their area”.

They added: “These are exceptional circumstances where councils have told us they’re struggling to prepare for resource-intensive elections to councils that will shortly be abolished, while also reorganising into more efficient authorities that can better serve local residents.

“There is a clear precedent for postponing local elections where local government reorganisation is in progress, as happened in 2019 and 2022.”

The five councils that confirmed they would be seeking postponements were:

- Blackburn with Darwen Council (Labour);

- Chorley Borough Council (Labour);

- East Sussex County Council (Conservative minority);

- Hastings Borough Council (Green minority);

- West Sussex County Council (Conservative).

The councils in Chorley, and East and West Sussex, had decided prior to Thursday’s government announcement that they would request a delay.

An East Sussex County Council spokesperson told Sky News: “It is welcome that the government is listening to local leaders and has heard the case for focussing our resources on delivery in East Sussex, particularly with devolution and reorganisation of local government, as well as delivering services to residents, such high priorities.”

They also pointed to the cost of electing councillors for a term of just one year, and argued that it would be “more prudent for just one set of elections to be held in 2027”.

Read more from Sky News:

David Walliams dropped by publisher

Woman jailed for plotting to murder husband

Christmas number one revealed

West Sussex County Council echoed those reasons and said it would cost taxpayers across the county £9m to hold elections in 2026, 2027, and 2028, as currently planned.

Chorley and Blackburn councils also cited the cost of delivering elections, and said they would prefer that money be spent on delivering the local government reorganisation and delivering services to local residents.

Meanwhile, 12 councils confirmed to Sky News that they would not be requesting delays:

- Basingstoke and Deane Borough Council (Liberal Democrat-Independents);

- Broxbourne Borough Council (Conservative);

- Colchester City Council (Labour-Liberal Democrat);

- Eastleigh Borough Council (Liberal Democrat);

- Essex County Council (Conservative);

- Hart District Council (Liberal Democrat-Community Campaign);

- Hastings Borough Council (Green minority);

- Isle of Wight Council (no overall control);

- Newcastle-under-Lyme Borough Council (Conservative);

- Portsmouth City Council (Liberal Democrat minority);

- Rushmoor Borough Council (Labour minority);

- Southampton City Council (Labour).

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024