Rate of inflation eases to 3.4% in February, official figures show

The rate of inflation slowed sharply to an annual rate of 3.4% in February, according to official figures charting a big contribution from food costs.

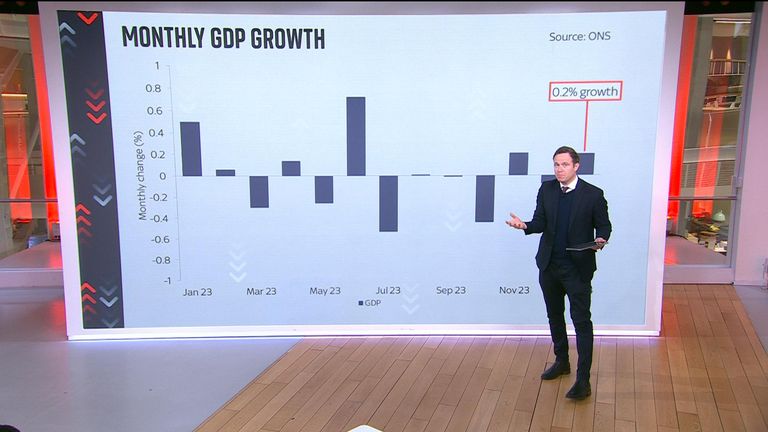

Data from the Office for National Statistics (ONS) showed an easing in the headline measure from the 4% rate recorded the previous month to a level last seen almost two-and-a-half years ago.

It was led, the report said, by food prices being almost flat this year compared with a large rise last year, while restaurant and café price rises also slowed.

Money latest: Reaction as UK inflation eases by more than expected

“These falls were only partially offset by price rises at the [fuel] pump and a further increase in rental costs,” ONS chief economist Grant Fitzner said.

The data marks further progress in the battle against energy-led price growth that followed Russia’s war in Ukraine and inflation is forecast to fall back below the Bank of England‘s target rate of 2% in the next few months.

However, the Bank’s interest rate-setting committee is widely expected to hold off on removing the medicine it has dished out to tackle inflation, possibly until the summer.

Its latest rate decision is due on Thursday.

Will the UK come out of recession?

Interest rate cuts would provide relief to millions of borrowers who have faced hefty increases to their costs as a consequence of higher interest rates.

But committee members are wary of starting the process as it’s feared inflation may tick back up in the second half of the year.

While there was some comfort in the latest data from core inflation figures, which strip out volatile elements such as food and energy costs, they are waiting for visibility on many price pressures including the pace of wage growth, disruption to shipping in the Red Sea and rising global oil costs.

Regular pay rises, according to separate ONS data last week, were still running above 6% – a level that could help drive demand in the flatlining economy and force up the pace of price increases.

Brent crude oil costs hit levels not seen since October last year earlier this week at $87 per barrel.

Interest rate cuts would help put more money back in people’s pockets over time, boosting the economy which officially entered recession in the second half of last year.

The economy is predicted to be the main battleground in the looming election so the timing of such action, by the politically neutral Bank, could be crucial.

‘I’m frustrated, I want an election’

London Stock Exchange Group (LSEG) data suggests the market expects the first cut to come in June but there is a growing school of thought that inflation may remain stickier than expected by that time, leaving August more in the frame.

Chancellor Jeremy Hunt said of the inflation data: “The plan is working. Inflation has not just fallen decisively but is forecast to hit the 2% target within months.

“This sets the scene for better economic conditions which could allow further progress on our ambition to boost growth and make work pay by bringing down national insurance as we work towards abolishing the double tax on work – but only if we can do so without increasing borrowing or cutting funding for public services.”

Rachel Reeves, Labour’s shadow chancellor, responded: “After fourteen years of chaos and uncertainty under the Conservatives working people are worse off. Prices are still high, the tax burden is the highest it has been in seventy years and mortgage payments are going up.

“Now Rishi Sunak is putting forward a reckless £46bn unfunded tax plan to abolish National Insurance that would risk crashing the economy and re-running the disastrous Liz Truss experiment.

“Britain cannot afford another five years of this failed Conservative government. It’s time for change and it’s time for Rishi Sunak to set the date for the election.”

Acres of sweet, red strawberries are ripening in West Sussex this winter ready to be sold in UK supermarkets.

LED lighting in vast glasshouses is enabling berries to be grown all year on a commercial scale for the first time ever.

It means less reliance on fruit flown in from countries like Egypt.

Bartosz Pinkosz

“The LED lighting is the prime reason for successful growing,” said Bartosz Pinkosz, operations director of The Summer Berry.

“If it was not a sunny day, the LED lighting would create enough energy for leaves to absorb that energy, take it in and deliver the energy to the berries.

“We are able to have the right sweetness in the berries and the right shape, right size.”

There are 36,000 square metres of the greenhouses at the site in Chichester, partially powered by renewable energy and buzzing with bees as pollinators.

Acres of strawberries ripening in West Sussex

And the new strand to the business means year-round work for 50 people.

But while it might cut the food miles dramatically, there’s still an inevitable environmental impact when a colossal space is created warm enough for pickers to wear short sleeves in winter.

Dr Tara Garnett, director of food systems platform TABLE, said: “You’re going to need a lot of heat and you’re going to need a lot of light in order to reproduce those summer growing conditions so everything hinges on the energy source you’re going to be using.

“And when we look at the UK self sufficiency levels in fruit and vegetables they are appalling – 16% of the fruit we consume is UK-grown, so the vast majority is imported, and when it comes to vegetables we’re looking more at 50% or so, so there’s a lot more we can do to build up, and should be doing.”

Around 1.5 million punnets of strawberries are expected to be picked on the site over the full stretch of winter, allowing British strawberries to be eaten this Christmas.

But for some, it’s simple – strawberries should be saved for summer, even if it is a much shorter journey from plant to plate.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024