What is a Waspi woman and what happened to them?

Back in the 1990s, a row was brewing over the state pension.

After it was introduced for everybody back in 1948, men were entitled to receive it when they hit 65, but women started getting the payments from the age of 60.

Politics live: Tories suffer another defection to Reform

With more women heading to work and longer life expectancies, many argued it was time to even out the playing field and bring women’s retirement age in line with men’s.

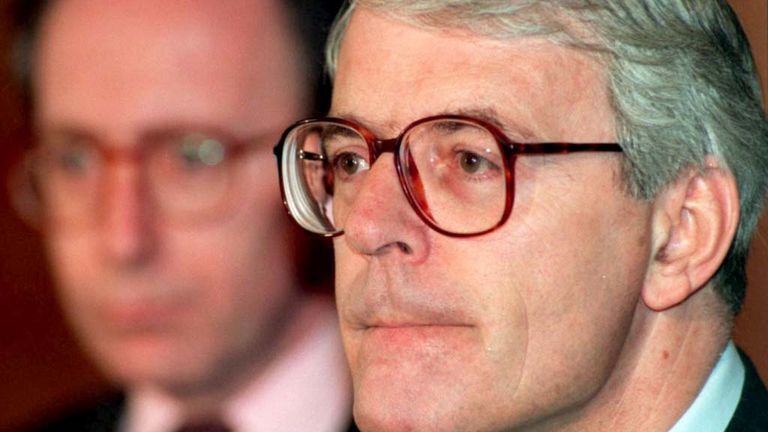

And come 1995, John Major’s Conservative government introduced the Pensions Act, setting out a timetable to make the change.

The legislation said the qualifying age for the state pension would slowly increase over 10 years between 2010 and 2020.

John Major introduced legislation to even out the pension age in 1995. Pic: PA

But come 2010 and the entrance of David Cameron’s coalition government, there was a desire to make cuts and save cash.

In 2011, a new Pensions Act was introduced that not only shortened the timetable to increase the women’s pension age to 65 by two years but also raised the overall pension age to 66 by October 2020 – saving the government around £30bn.

The changes in the law led to a backlash from the women affected – namely those born in the 1950s.

They complained many women weren’t appropriately notified of the changes by the Department for Work and Pensions (DWP) back in 1995, with some only receiving letters about it 14 years after the legislation passed.

Others claimed to only have received a notification the year before they had been expecting to retire, aged 60, while more said they never received any communication from the department at all.

And when the law changed again in 2011, there was again little or no notice from the government as women had to re-plan their retirements once more.

David Cameron and Nick Clegg’s coalition focused on saving cash. Pic: PA

Come 2015, a group of women impacted by the situation set up Women Against State Pension Inequality – or Waspi for short – to campaign on their behalf.

The group took no issue with plans to equalise the pension age, but they claimed millions of women had suffered financially because of the lack of time they had to plan their retirements.

By October 2018, Waspi had secured a full scale inquiry into the actions of the DWP by the Parliamentary and Health Service Ombudsman (PHSO).

MP sings Beatles hit to highlight Waspi plight

It took five years for them to carry out their work, but when they released their report in March 2024, it was damning.

The PHSO said thousands of women might have been impacted by the DWP’s “failure to adequately inform them” about the change to their state pension age, and they ruled compensation was “owed”.

The report suggested the compensation figure per person – based on the sample cases its authors have seen – should fall between £1,000 and £2,950.

But the ombudsman’s chief executive, Rebecca Hilsenrath, said she had “significant concerns” the DWP will not act on its findings and its recommendations – which are not legally binding – so PHSO had “proactively asked parliament to intervene and hold the department to account”.

Keep up with all the latest news from the UK and around the world by following Sky News

Both the DWP and Number 10 have said they will consider the ombudsman’s report and respond to their recommendations formally “in due course”.

But the Liberal Democrats are calling on the government to confirm payouts for “these courageous women, who have tirelessly campaigned for justice after being left out of pocket”.

The executive order creating the Office of Digital Assets and Blockchain Technology under the New York City government came three months before Eric Adams will leave office.

The US government said it would pursue forfeiture of the Bitcoin holdings tied to a Cambodia-based company if the alleged ringleader were convicted.

Less than a week after reports of an agreement between the “Bitcoin Jesus” and US authorities, Roger Ver’s 2024 criminal tax case may be nearing an end.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024