Boeing boss and chairman head for exit amid safety crisis

Boeing has revealed its under-fire chairman and chief executive are leaving their roles while pledging to “fix” the safety crisis engulfing the planemaker.

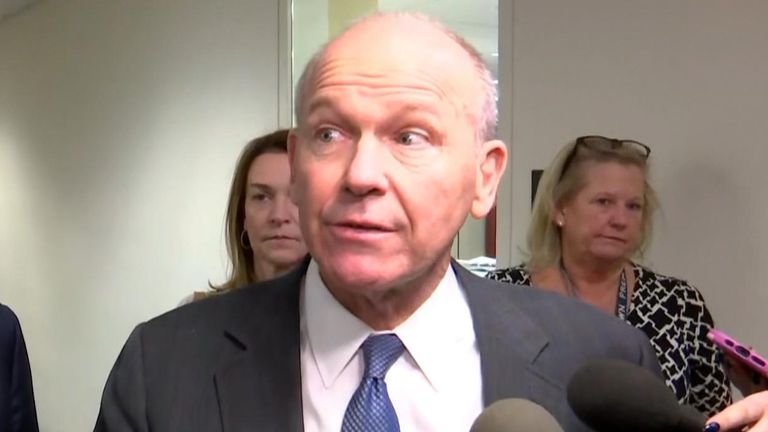

The company said Dave Calhoun, who has been CEO for just over four years, planned to step down by the year’s end as part of a management shake-up.

It will also see Stan Hope, the head of its commercial airlines division, retire – and chairman Larry Kellner stand down from the board.

The changes were revealed as Boeing customers, including Ryanair, pile pressure on the company over the fallout from its latest safety issue, which has resulted in further delays to plane orders.

Boeing CEO Dave Calhoun said he would play a role in the appointment of his successor

Money latest: Get ready for 3% interest rates, respected economists predict

Airlines have endured years of disruption related to 737 MAX aircraft variants.

The MAX 8 fleet was grounded globally for almost two years after two fatal crashes that left 346 people dead – accidents that were blamed on faulty flight control software.

What’s going on at Boeing?

The return to the skies in 2021 was knocked by the collapse in demand for international travel due to the COVID pandemic.

But Boeing’s safety record came under close scrutiny again in January this year when a panel blowout occurred on a 737 MAX 9 plane while at 16,000 feet, forcing an emergency landing.

Read more:

Ryanair boss declares passengers are safe despite Boeing issues

Boeing axes 737 MAX chief after mid-air scare

US regulator increases oversight of Boeing

Keep up with all the latest news from the UK and around the world by following Sky News

US aviation regulators have since placed strict production limits on Boeing as part of efforts to ensure confidence in its manufacturing quality.

“For years, we prioritised the movement of the airplane through the factory over getting it done right, and that’s got to change,” chief financial officer Brian West said last week.

Ryanair chief executive Michael O’Leary, who had previously been critical of quality control at Boeing, said in reaction to the company’s statement: “We welcome these much-needed management changes in Seattle.

“We look forward to working with Stephanie Pope to accelerate B737 aircraft deliveries to customers, including Ryanair in Europe, for summer and autumn 2024.

“We also look forward to continuing to work with Boeing CEO Dave Calhoun and CFO Brian West, and to helping Boeing recover its aircraft deliveries so that Ryanair can continue to grow strongly as Boeing’s No.1 customer here in Europe.”

Long-suffering Boeing investors also welcomed the announcements, with shares rising 4%.

Mr Calhoun told Sky’s US partner CNBC it was “100% my decision to go”, insisting he had not been pushed.

“Why now? I’ve entered my fifth year. The end of this year, I’ll be close to 68 years old.

“I’ve always said to the board and the board has been very prepared, I would give them plenty of notice so that they could understand and play in succession in, in regular order. And that’s what this is about. It’s me giving them notice that at the end of this year, I plan to retire. And then and then them taking the actions that they’ve taken.”

He added that he would play a role in the appointment of his successor.

In an email to Boeing staff, he said: “As we begin this period of transition, I want to assure you, we will remain squarely focused on completing the work we have done together to return our company to stability after the extraordinary challenges of the past five years, with safety and quality at the forefront of everything that we do.”

A trove of newly released Epstein files include emails that appear to involve Andrew Mountbatten-Windsor, while another suggests Donald Trump travelled on the billionaire’s private jet “many more times than previously has been reported”.

The US Department of Justice released at least 11,000 more files on Tuesday.

It went on to claim that some of them “contain untrue and sensationalist claims” about President Trump.

Here are some of the latest news lines from this release of Epstein files. Being named in these papers does not suggest wrongdoing.

Who is ‘The Invisible Man’?

Among the documents released is an email sent to Ghislaine Maxwell that speaks about “the girls” being “completely shattered” at a Royal Family summer camp at Balmoral.

It is dated 16 August 2001 and sent by a person referred to as “The Invisible Man”, who signed off the message as “A” – and is believed to be Andrew.

Sky News has come to that conclusion from reviewing the email address used, which is assigned to the Duke of York in Epstein’s contacts book and the chain of correspondence.

In the correspondence, “The Invisible Man” asks Maxwell: “How’s LA? Have you found me some new inappropriate friends?”

Andrew Mountbatten-Windsor has previously denied any allegations against him.

The Peru trip

Another email appears to show Maxwell arranging “two-legged sight seeing” for “The Invisible Man” during a trip to Peru.

She appears to forward to “The Invisible Man” part of a conversation between herself and another person.

The email says: “I just gave Andrew your telephone no. He is interested in seeing the Nazca lines. He can ride but it is not his favorite sport ie pass on the horses.”

“Some sight seeing some 2 legged sight seeing (read intelligent pretty fun and from good families) and he will be very happy. I know I can rely on you to show him a wonderful time and will only introduce him to friends that you can trust,” Maxwell said.

The context of the email is unclear and there is no suggestion of any wrongdoing.

Trump on Epstein’s jet?

The latest bunch of files also includes an email from an unidentified prosecutor dated 7 January, 2020, in which President Trump is mentioned.

The email accuses him of travelling on Epstein’s private jet “many more times than previously has been reported”.

It adds that President Trump “is listed as a passenger on at least eight flights between 1993 and 1996, including at least four flights on which Maxwell was also present”.

The email’s sender and receiver have been redacted. However, at the bottom of the email it says assistant US attorney, Southern District of New York. The name has also been redacted.

President Trump has denied any wrongdoing in relation to his relationship with Epstein, and being on any of Epstein’s flights does not indicate any wrongdoing.

Read more:

Trump defends ‘big boy’ Clinton after Epstein files release

Why Andrew photo in Epstein files is awkward for Royal Family

Limousine driver report about Trump

One of the documents in the release shows a report made to the FBI that was recorded on 27 October 2020.

It includes an unverified claim by a limousine driver that he overheard the US president discussing “abusing some girl” in 1995.

The driver also mentions Trump said “Jeffrey” while on the phone during a journey to Dallas Fort Worth Airport in Texas.

A significant part of the statement, along with the driver’s identity, has been redacted.

The US justice department has said that some of the documents in the latest Epstein files release “contain untrue and sensationalist claims made against President Trump that were submitted to the FBI right before the 2020 election”.

“To be clear: the claims are unfounded and false, and if they had a shred of credibility, they certainly would have been weaponized against President Trump already,” it said.

Postcard mentions ‘our president’

Also among the documents is a postcard that claims to have been sent by Jeffrey Epstein, but has been refuted by the justice department.

In it, the sender tells the recipient: “Our president also shares our love of young, nubile girls.”

It’s not clear who “our president” refers to and the context of the postcard is also unclear.

The US justice department initially said it was “looking into the validity” of the postcard but later said on X that the “FBI has confirmed” the postcard is “FAKE”.

It cited reasons including a claim that the writing does not appear to match Epstein’s and another that the letter was postmarked three days after his death.

Row over unreleased documents

It is believed that many files relating to Epstein are yet to be made public.

There has been anger at the justice department’s slow release of the files, with politicians threatening to launch legal action against Attorney General Pam Bondi.

The deadline for the release of all the documents has passed.

“The DOJ needs to quit protecting the rich, powerful, and politically connected,” Republican congressman Thomas Massie said.

A survivor of Jeffrey Epstein has spoken of the moment she met Andrew Mountbatten-Windsor on the disgraced financier’s private island.

Lisa Phillips says that revealing the true extent of Epstein’s abuses is important for the protection of future generations.

Andrew Mountbatten-Windsor has previously denied any allegations against him.

Speaking to US correspondent James Matthews on the day a new tranche of documents was released, she said she believes the “really important stuff” wasn’t released.

She recalled meeting Epstein in 2000 when she was working as a fashion model.

Ms Phillips said she was working on an island near Saint Thomas in the Caribbean and went over to Epstein’s island for a day, and met Epstein himself at dinner that evening.

“It took a few hours of him speaking to me one-on-one at the table, basically asking me a lot of questions about my life and my relationship with my family and my ambitions.”

She said Epstein was “very big” on her goals and became excited when he heard she had lived in Oxford, England, as a child.

“He asked me if I wanted to meet a prince, and I said yes.”

Epstein files latest: New batch of documents released

Ms Phillips explained that a man walked up and was introduced to her, and that he spoke to some people there and then said goodbye.

“It was very brief,” she said, adding that only years later did she realise that this was the former prince, Andrew.

She was asked about an email in the recently released files that appears to show Andrew Mountbatten-Windsor asking Ghislaine Maxwell about “inappropriate friends”.

“That is a very revealing email, isn’t it?” Ms Phillips said. “It’s very creepy, disturbing, and I mean, that’s why she’s in jail, right?”

The context of the email is unclear, and there is no suggestion of any wrongdoing.

Andrew Mountbatten-Windsor has previously denied any allegations against him and Sky News has contacted Andrew’s representatives for comment on the latest release.

Asked about the impact being in Epstein’s orbit has had on her life, Ms Phillips said: “It hasn’t felt good to know that so much of my past that I worked hard for was really just smoke and mirrors and part of a bigger web.”

On the delays in releasing the files, she claimed “the really important stuff wasn’t released”.

She also spoke about her and other survivors’ ongoing fight for justice.

“We’re still doing our research, and we will still be bringing whatever we find to the proper authorities. And we’re not going to give up.”

Survivors of Jeffrey Epstein’s abuse are already looking beyond the release of the files in their pursuit of justice. It would seem sensible.

For the second time, a tranche of images and documents was released by the US Department of Justice and, for the second time, it didn’t detail the facts and failures which allowed Epstein to thrive.

If those key elements were in there, they were redacted.

The release of the files had been anticipated as a moment to unveil the whole story, to identify its characters and their crimes.

But this is a book with pages missing and piecing together the broader network that enabled sex-trafficking on an industrial scale won’t be easy.

It remains the fierce ambition for survivors, aware that Epstein was no one-man operation.

They know because they were there.

“I think the really important stuff wasn’t released,” Lisa Phillips told me.

Jeffrey Epstein with Ghislaine Maxwell. Pic: U.S. Department of Justice via AP

A survivor of Epstein’s abuse, she said women who suffered at his hands had been sharing information and would have something to report in the New Year.

“We’re still fighting, we’re still doing our research and we will still bring whatever we find to the proper authorities. This is really important to us, we’re all mothers now and have kids the same age as we were, so this fight is to the heart.”

They have seen their story wrapped in politics, in all its management and manipulation.

The resistance to publish, the timing of release, the redactions – they are matters beyond their control that could scarcely matter more.

Read more:

Epstein survivor describes ‘blindness’ around financier

Trump defends ‘big boy’ Clinton after Epstein files release

Why Andrew photo in Epstein files is awkward for Royal Family

We have seen thousands of files released but they come without context or explanation.

While they each say something about Epstein, his crimes and depravity, they don’t join the dots to the broader conspiracy. No one is better placed to do that than its victims.

This news story is their story. Ultimately, it may be for them to tell because we’re hearing it from no one else.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024