Google lays off hundreds of ‘Core’ employees, moves some positions to India and Mexico

Sundar Pichai, chief executive officer of Alphabet Inc., during Stanford’s 2024 Business, Government, and Society forum in Stanford, California, US, on Wednesday, April 3, 2024.

Justin Sullivan | Getty Images

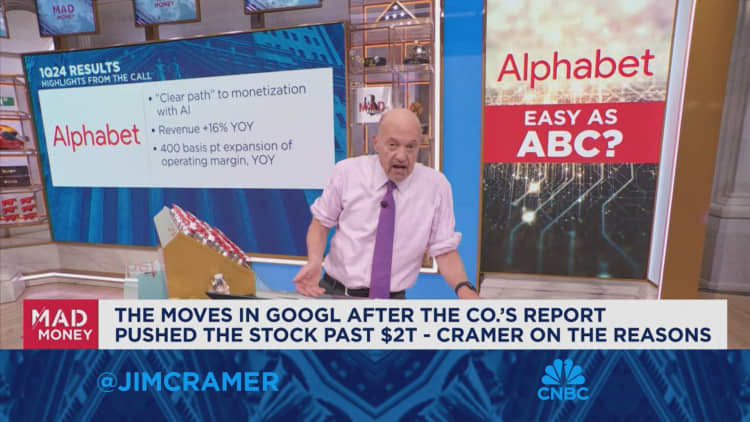

Just ahead of its blowout first-quarter earnings report last week, Google laid off at least 200 employees from its “Core” teams, in a reorganization that will include moving some roles to India and Mexico, CNBC has learned.

Google’s Core unit is responsible for building the technical foundation behind the company’s flagship products and protecting users’ online safety, according to Google’s website. Core teams include key technical units from information technology, its Python developer team, technical infrastructure, security foundation, app platforms, core developers and various engineering roles.

At least 50 of the positions eliminated were in engineering at the company’s offices in Sunnyvale, California, filings show. Many of the Core teams will hire corresponding roles in Mexico and India, according to internal documents viewed by CNBC.

Asim Husain, vice president of Google Developer Ecosystem, announced some of the layoffs to his team in an email last week. He also spoke at a town hall and told employees that this was the biggest planned reduction for his team this year, an internal document shows.

“We intend to maintain our current global footprint while also expanding in high-growth global workforce locations so that we can operate closer to our partners and developer communities,” Husain wrote in the email.

Alphabet has been slashing headcount since early last year, when the company announced plans to eliminate about 12,000 jobs, or 6% of its workforce, following a downturn in the online ad market. Even with digital advertising rebounding in the past couple quarters, Alphabet has continued downsizing, with layoffs across multiple organizations this year.

CFO Ruth Porat announced in mid-April a restructuring to the company’s finance department, which included layoffs and moving positions to Bangalore and Mexico City. The company’s search boss, Prabhakar Raghavan, told employees at an all-hands meeting in March that Google plans to build teams closer to users in key markets, including India and Brazil, where labor is cheaper than in the U.S.

The latest cuts comes as the company enjoys its fastest growth rate since early 2022, alongside improving profit margins. Last week, Alphabet reported a 15% jump in first-quarter revenue from a year earlier, and announced its first-ever dividend and a $70 billion buyback.

“Announcements of this sort may leave many of you feeling uncertain or frustrated,” Husain wrote in the email to developers. He added that his message to developers is that the changes “are in service of our broader goals” as a company.

The teams involved in the reorganization have been key to the company’s developer tools, an area that’s being streamlined by Google as it incorporates more AI into the products. In February, Google announced a major rebrand of its chatbot from Bard to Gemini, the same name as the suit of AI models that power it.

Alphabet is gearing up for its annual developer conference, Google I/O, on May 14, where the company traditionally reveals new developer products and tools that have been underway during the prior year. Husain said in a memo explaining the developer changes that generative AI is at an “inflection point.”

“Recent advances in Generative AI across the industry, including Google’s Gemini, are changing the very nature of software development as we know it,” Husain wrote.

In a separate email, security engineering vice president Pankaj Rohatgi, told his team that, “In order to optimize for our business goals, we are expanding work to other locations, which will result in some role eliminations and proposed role eliminations.”

The Core layoffs also include the governance and protected data group, which will be at the center of regulatory challenges facing the company, particularly as lawmakers across the globe focus more on developments in AI. The European Union’s Digital Markets Act (DMA) went into effect in March, and is aimed at clamping down on anti-competitive practices in tech.

Evan Kotsovinos, Google’s vice president of governance and protected data, wrote about the upcoming changes in an email last week.

Kotsovinos said the team’s success means responding to “escalating regulatory focus” and is contingent on “moving faster.”

Raghavan, Google’s senior vice president overseeing search, recently referenced heightened competition, a more challenging regulatory environment and slower organic growth as the company’s “new operating reality.”

Google confirmed the Core reorganization and layoffs, and a spokesperson told CNBC that employees will be able to apply for open roles within Google and to access outplacement services.

“As we’ve said, we’re responsibly investing in our company’s biggest priorities and the significant opportunities ahead,” the spokesperson said in an email. “A number of our teams made changes to become more efficient and work better, remove layers and align their resources to their biggest product priorities.”

WATCH: Google alumni-led startups turn up pressure on top AI companies

Tesla CEO Elon Musk attends the Saudi-U.S. Investment Forum, in Riyadh, Saudi Arabia, May 13, 2025.

Hamad I Mohammed | Reuters

Tesla’s shares have finally turned positive for the year.

After a dismal first quarter, which was the worst for the stock in any period since 2022, and a brutal start to April, following President Donald Trump’s announcement of sweeping new tariffs, Wall Street has again rallied around the electric vehicle maker.

The stock rose 3.6% on Monday to $410.26, topping its closing price of 2024 by over $6. It’s up 85% since bottoming for the year at $221.86 on April 4. A new filing revealed that CEO Elon Musk purchased about $1 billion worth of shares in the company through his family foundation.

It’s the second straight year Tesla has bounced back after a down first quarter. Last year, the shares fell 29% in the first three months before ending up 63% for 2024.

In recent weeks, analysts have praised the EV maker’s proposed pay plan for Musk, which could amount to a $1 trillion windfall for the world’s richest person over the next decade. The company has also gotten a boost from its new MegaBlocks battery energy storage systems that Tesla ships preassembled to businesses looking to lower their power costs or make greater use of electricity from renewable resources.

Even with the rebound, Tesla is the second-worst performer this year among tech’s megacaps, ahead of only Apple, which is down about 5% in 2025. Tesla is still in the midst of a multi-quarter sales slump due to an aging lineup of EVs and increased competition from lower-cost competitors in China, namely BYD.

Tesla has seen a consumer backlash, in part because of Musk’s political activities, including spending nearly $300 million to propel President Trump back to the White House and his work with the Trump administration to slash the federal workforce.

Tesla leadership has been working to shift investors’ attention to other topics such as robotaxis and humanoid robots.

However, the company has yet to deliver vehicles that are safe to use without a human onboard and ready to take control if needed. And while Musk is touting Tesla’s Optimus robots, which he says will be able to do everything from factory work to babysitting, a product is still a long way from hitting the market.

WATCH: Musk’s share purchase

Google CEO Sundar Pichai gestures to the crowd during Google’s annual I/O developers conference in Mountain View, California on May 20, 2025.

Camille Cohen | Afp | Getty Images

Alphabet has joined the $3 trillion club.

Shares of the search giant jumped more than 4% on Monday, pushing the company into territory occupied only by Nvidia, Microsoft and Apple.

The stock got a big lift in early September from an antitrust ruling by a judge, whose penalties came in lighter than shareholders feared. The U.S. Department of Justice wanted Google to be forced to divest its Chrome browser, and last year a district court ruled that the company held an illegal monopoly in search and related advertising.

But Judge Amit Mehta decided against the most severe consequences proposed by the DOJ, which sent shares soaring to a record. After the big rally, President Donald Trump congratulated the company and called it “a very good day.”

Alphabet shares are now up more than 30% this year, compared to the 15% gain for the Nasdaq.

The $3 trillion milestone comes roughly 20 years after Google’s IPO and a little more than 10 years after the creation of Alphabet as a holding company, with Google its prime subsidiary.

CEO Sundar Pichai was named CEO of Alphabet in 2019, replacing co-founder Larry Page. Pichai’s latest challenge has been the surge of new competition due to the rise of artificial intelligence, which the company has had to manage through while also fending off an aggressive set of regulators in the U.S. and Europe.

The rise of Perplexity and OpenAI ended up helping Google land the recent favorable antitrust ruling. The company’s hopes of becoming a major AI player largely ride with Gemini, Google’s flagship suite of AI models.

Technology

Bessent: TikTok deal ‘framework’ reached with China, Trump and Xi will finalize it Friday

Samuel Boivin | Nurphoto | Getty Images

The U.S. and China have reached a ‘framework’ deal for social media platform TikTok, Treasury Secretary Scott Bessent said Monday.

“It’s between two private parties, but the commercial terms have been agreed upon,” he said from U.S.-China talks in Madrid.

Both President Donald Trump and Chinese President Xi Jinping will meet Friday to discuss the terms. Trump also said in a Truth Social post Monday that a deal was reached “on a ‘certain’ company that young people in our Country very much wanted to save.”

Bessent indicated that the framework could pivot the platform to U.S.-controlled ownership.

TikTok did not immediately respond to a request for comment.

The comments came during the latest round of trade discussions between the U.S. and China. Relations have soured between the two countries in recent months from Trump’s tariffs and other trade restrictions.

At the same time, TikTok parent company ByteDance faces a Sept. 17 deadline to divest the platform’s U.S. business or face being shut down in the country.

U.S. Trade Representative Jamieson Greer said Monday that the deadline may need to be pushed back to get the deal signed, but there won’t be ongoing extensions.

Congress passed a law last year prohibiting app store operators like Apple and Google from distributing TikTok in the U.S. due to its “foreign adversary-controlled application” status.

But Trump postponed the shutdown in January, signing an executive order in January that gave ByteDance 75 more days to make a deal. Further extensions came by way of executive orders in April and in June.

Commerce Secretary Howard Lutnick said in July that TikTok would shutter for Americans if China doesn’t give the U.S. more autonomy over the popular short-form video app.

As for who controls the platform, Trump told Fox News in June that he had a group of “very wealthy people” ready to buy the app and could reveal their identities in two weeks. The reveal never came.

He has previously said he’d be open to Oracle Chairman Larry Ellison or Tesla CEO Elon Musk buying TikTok in the U.S. Artificial intelligence startup Perplexity has submitted a bid for an acquisition, as has businessman Frank McCourt’s Project Liberty internet advocacy group, CNBC reported in January.

Trump told CNBC in an interview last year that he believed the platform was a national security threat, although the White House started a TikTok account in August.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment11 months ago

Environment11 months agoHere are the best electric bikes you can buy at every price level in October 2024