Google employees question execs over ‘decline in morale’ after blowout earnings

Google’s business is growing at its fastest rate in two years, and a blowout earnings report in April sparked the biggest rally in Alphabet shares since 2015, pushing the company’s market cap past $2 trillion.

But at an all-hands meeting last week with CEO Sundar Pichai and CFO Ruth Porat, employees were more focused on why that performance isn’t translating into higher pay, and how long the company’s cost-cutting measures are going to be in place.

“We’ve noticed a significant decline in morale, increased distrust and a disconnect between leadership and the workforce,” a comment posted on an internal forum ahead of the meeting read. “How does leadership plan to address these concerns and regain the trust, morale and cohesion that have been foundational to our company’s success?”

Google is using artificial intelligence to summarize employee comments and questions for the forum.

Alphabet’s top leadership has been on the defensive for the past few years, as vocal staffers have railed about post-pandemic return-to-office mandates, the company’s cloud contracts with the military, fewer perks and an extended stretch of layoffs — totaling more than 12,000 last year — along with other cost cuts that began when the economy turned in 2022.

Employees have also complained about a lack of trust and demands that they work on tighter deadlines with fewer resources and diminished opportunities for internal advancement.

The internal strife continues despite Alphabet’s better-than-expected first-quarter earnings report, in which the company also announced its first dividend as well as a $70 billion buyback.

“Despite the company’s stellar performance and record earnings, many Googlers have not received meaningful compensation increases” a top-rated employee question read. “When will employee compensation fairly reflect the company’s success and is there a conscious decision to keep wages lower due to a cooling employment market?”

Another highly-rated comment centered around the company’s priorities, including its hefty investments in artificial intelligence.

“To many people, there’s a clear disconnect between spending billions on stock buybacks and dividends and re-investing in AI and retraining critical Googlers,” the post said.

Ruth Porat, Alphabet’s chief financial officer, appears on a panel session at the World Economic Forum in Davos, Switzerland, on May 24, 2022.

Hollie Adams | Bloomberg | Getty Images

“Our priority is to invest in growth,” Porat said, as she took the microphone to respond to questions. “Revenue should be growing faster than expenses.”

She also took the rare step of admitting to leadership’s mistakes in its prior handling of investments.

“The problem is a couple of years ago — two years ago, to be precise — we actually got that upside down and expenses started growing faster than revenues,” said Porat, who announced nearly a year ago that she would be stepping down from the CFO position but hasn’t yet vacated the office. “The problem with that is it’s not sustainable.”

Google executives have been hammering this theme of late.

Search boss Prabhakar Raghavan, in an internal meeting last month, pointed to Google’s core business challenges, saying “things are not like they were 15 to 20 years ago,” and urged employees to work faster. He told his team, “It’s not like life is going to be hunky-dory, forever.”

Google’s cloud business was among units instructing employees to move within shorter timelines even though they had fewer resources after cost cuts.

Google’s use of cash

There were a lot of employee questions ahead of last week’s meeting directed at the company’s buyback, Porat said.

As of last quarter, Alphabet had more than $100 billion in cash on the balance sheet but, Porat said, “you can’t just drain it” or the company would find itself in the same position as in 2022.

By contrast, distributing cash to shareholders is not considered an expense on the balance sheet, she said, adding that the board has a fiduciary duty to consider such measures. Buybacks and dividends don’t replace investments in AI, Porat said.

Pichai chimed in when Porat wrapped up her response.

“I think you almost set the record for the longest TGIF answer,” he said. Google all-hands meetings were originally called TGIFs because they took place on Fridays, but now they can occur on other days of the week.

Pichai then joked that leadership should hold a “Finance 101” Ted Talk for employees.

With respect to the decline in morale brought up by employees, Pichai said “leadership has a lot of responsibility here, adding that “it’s an iterative process.”

Pichai said the company staffed up too much during the Covid pandemic.

“We hired a lot of employees and from there, we have had course correction,” Pichai said.

Alphabet’s full-time headcount climbed to over 190,000 at the end of 2022, up almost 22% from a year earlier and 40% higher than at the close of 2020.

Pichai, who replaced Google co-founder Larry Page as CEO of Alphabet in 2019, has taken his share of criticism of late for his messaging to the workforce as well as his lofty pay package, which swelled to $226 million, including stock awards, in 2022.

The package in 2022 included $218 million in equities through a triennial stock grant. His total pay in 2023 was $8.8 million, up from about $8 million the prior year (excluding the stock grant), according to Alphabet’s proxy filing. Other than Pichai’s $2 million salary for each year, most of his additional compensation was for personal security.

Employees have complained about the level of Pichai’s compensation at a time when the company is downsizing.

“Given the recent headcount and positive earnings, what is the company’s headcount strategy?” one question read. Another asked, “Given the strong results, are we done with cost-cutting?”

Pichai said the company is “working through a long period of transition as a company” which includes cutting expenses and “driving efficiencies.” Regarding the latter point, he said, “We want to do this forever.”

“To be clear, we’re growing our expenses as a company this year, but we’re moderating our pace of growth” Pichai said. “We see opportunities where we can re-allocate people and get things done.”

A Google spokesperson reiterated to CNBC that the company is investing in its biggest priorities and will continue to hire in those areas.

The spokesperson also said most employees will receive a pay raise this year, including an increased salary, equity grants and a bonus. Executives at the all-hands meeting said that staffers who received raises last year got smaller raises than usual.

Another comment floated ahead of the meeting was tied to “growing concerns about jobs moving from the U.S. to lower-cost locations.” CNBC reported last week that Google is laying off at least 200 employees from its “Core” organization, which includes key teams and engineering talent.

Executives were asked about the ongoing layoffs, despite the strong earnings report, and “when can we expect an end to the uncertainty and disruption that layoffs create?”

Pichai said the company will have worked through the majority of layoffs in the first half of 2024.

“Assuming current conditions, the second half of the year will be much smaller in scale,” Pichai said, referring to job cuts. He said it will continue to be “very, very disciplined about managing headcount growth throughout the year.”

That means the company is still making tough choices regarding investments in new projects.

“There’s a lot of demand to do new things and, in the past, we would have just done it reflexively by growing headcount,” Pichai said. “We can’t do it now through the transition we are in.”

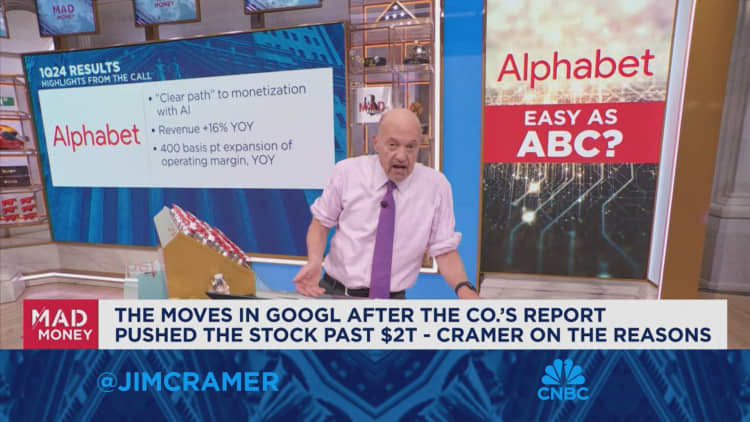

WATCH: Alphabet’s investor call had a ‘remarkable’ level of transparency, says Jim Cramer

Technology

ServiceNow in talks to acquire cybersecurity startup Armis in potential $7 billion deal, Bloomberg reports

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024