Former Rank chief Birch in talks to run Ladbrokes-owner Entain

Henry Birch, the former boss of Rank Group, is among the candidates vying to run Entain, the FTSE-100 owner of Ladbrokes.

Sky News has learnt that Mr Birch is one of a small number of candidates being considered by Entain to replace Jette Nygaard-Andersen as its permanent chief executive.

The recruitment process comes at a challenging time for Entain, which has been beset by boardroom upheaval and regulatory difficulties in various international markets.

Its stock has halved in the last year, leaving it with a market capitalisation of just under £5bn.

This weekend, sources close to the company confirmed that Mr Birch was a serious contender for the post, although they said others were also in contention.

An appointment could still be weeks or even a small number of months away, they added.

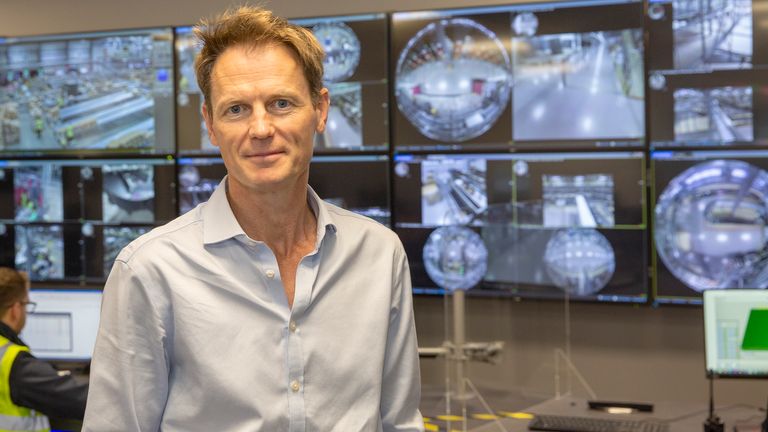

Henry Birch, former CEO of Very Group

Mr Birch stepped down as chief executive of Very Group, the online retailer owned by the Barclay family, in 2022.

He is an experienced gambling industry executive, having spent four years as chief executive of William Hill Online prior to joining the London-listed multichannel gaming operator Rank Group.

He has also held roles at Leisure & Gaming plc and BettingCorp.

Under Mr Birch, Very Group broke the £2bn annual sales mark for the first time.

Investors in Entain have been pressing its board to recruit a new chief executive with substantial gambling experience as it grapples with a plunging share price and numerous regulatory and strategic challenges.

Last week, Sky News revealed that former bosses of bookies Coral and Skybet had rejected overtures to become its new boss.

Pic: Reuters

Industry sources said that Dan Taylor, chief executive of Flutter Entertainment’s international operations, had also been approached, although it was unclear whether he was interested.

Entain has been under siege from activist investors for months.

In January, it announced that Ricky Sandler, who runs Entain shareholder Eminence Capital, would join its board as a non-executive director.

Last month, it said that Barry Gibson, its chairman, would retire later this year and be replaced by interim chair, and former acting CEO, Stella David.

Entain has hired bankers to sell PartyPoker and other non-core operations, which the Financial Times reported could include Netherlands-based BetCity, which Entain bought for £398mn last year.

As well as Ladbrokes, Entain owns Coral and a stake in BetMGM, a major US betting player.

Read more on Sky News:

Calls for arena ticket levy and tax relief

British Airways owner’s profits soar

Interest rate held for sixth consecutive time

Keep up with all the latest news from the UK and around the world by following Sky News

MGM Resorts, the US casino operator behind the Bellagio in Las Vegas, attempted to buy Entain in 2021 but was rebuffed at a much higher valuation than the UK company’s shares trade at now.

MGM has since ruled out a further bid, although analysts expect it to return at some stage.

The company has faced a deluge of regulatory problems, triggering sharp criticism of its governance and business practices.

Last December, it was ordered to pay £615m for failing to prevent bribery at its former Turkish subsidiary under a deferred prosecution agreement.

Shares in Entain closed at 778.8p on Friday, giving the company a market capitalisation of £4.98bn.

Entain declined to comment, while Mr Birch could not be reached for comment.

Rachel Reeves has said she is determined to “defy” forecasts that suggest she will face a multibillion-pound black hole in next month’s budget.

Writing in The Guardian, the chancellor argued the “foundations of Britain’s economy remain strong” – and rejected claims the country is in a permanent state of decline.

Reports have suggested the Office for Budget Responsibility is expected to downgrade its productivity growth forecast by about 0.3 percentage points.

Rachel Reeves. PA file pic

That means the Treasury will take in less tax than expected over the coming years – and this could leave a gap of up to £40bn in the country’s finances.

Ms Reeves wrote she would not “pre-empt” these forecasts, and her job “is not to relitigate the past or let past mistakes determine our future”.

“I am determined that we don’t simply accept the forecasts, but we defy them, as we already have this year. To do so means taking necessary choices today, including at the budget next month,” the chancellor added.

She also pointed to five interest rate cuts, three trade deals with major economies and wages outpacing inflation as evidence Labour has made progress since the election.

Speculation is growing that Ms Reeves may break a key manifesto pledge by raising income tax or national insurance during the budget on 26 November.

Read more from Sky News:

What tax rises and spending cuts could Reeves announce?

Start-ups warn the chancellor over budget tax bombshell

Chancellor faces tough budget choices

Although her article didn’t address this, she admitted “our country and our economy continue to face challenges”.

Her opinion piece said: “The decisions I will take at the budget don’t come for free, and they are not easy – but they are the right, fair and necessary choices.”

Yesterday, Sky’s deputy political editor Sam Coates reported that Ms Reeves is unlikely to raise the basic rates of income tax or national insurance, to avoid breaking a promise to protect “working people” in the budget.

Tax hikes possible, Reeves tells Sky News

Sky News has also obtained an internal definition of “working people” used by the Treasury, which relates to Britons who earn less than £45,000 a year.

This, in theory, means those on higher salaries could be the ones to face a squeeze in the budget – with the Treasury stating that it does not comment on tax measures.

Read more: The taxes Reeves could raise

In other developments, some top economists have warned Ms Reeves that increasing income tax or reducing public spending is her only option for balancing the books.

Experts from the Institute for Fiscal Studies have cautioned the chancellor against opting to hike alternative taxes instead, telling The Independent this would “cause unnecessary amounts of economic damage”.

Although such an approach would help the chancellor avoid breaking Labour’s manifesto pledge, it is feared a series of smaller changes would make the tax system “ever more complicated and less efficient”.

KitKats, Gaviscon, toothpaste, and even Freddo have all fallen victim to shrinkflation, consumer group Which? has found.

As families struggle with the cost of a trip to the supermarket, a survey of shoppers revealed how many products are getting smaller – while others are being downgraded with cheaper ingredients.

Among the examples are:

• Aquafresh complete care original toothpaste – from £1.30 for 100ml to £2 for 75ml at Tesco, Sainsbury’s and Ocado

• Gaviscon heartburn and indigestion liquid – from £14 for 600ml to £14 for 500ml at Sainsbury’s

• Sainsbury’s Scottish oats – from £1.25 for 1kg to £2.10 for 500g

• KitKat two-finger multipacks – from £3.60 for 21 bars to £5.50 for 18 bars at Ocado

• Quality Street tubs – from £6 for 600g to £7 for 550g at Morrisons

• Freddo multipacks – from £1.40 for five bars to £1.40 for four bars at Morrisons, Ocado and Tesco

Which? also received reports of popular treats missing key ingredients, as manufacturers seek to cut costs.

The amount of cocoa butter in white KitKats has fallen below 20%, meaning they can no longer actually be sold as white chocolate.

It comes after Penguin and Club bars lost their legal status as a chocolate biscuit, as they now contain more palm oil and shea oil than cocoa – as reported in the Sky News Money blog.

Which? retail editor Reena Sewraz called on supermarkets to be “more upfront” about price changes to help households “already under immense financial pressure” get better value.

While keeping track of the size and weight of products can be tricky, Which? has two top tips for detecting shrinkflation.

The first is to be wary of familiar products labelled as “new” – because the only thing that’s new may end up being the smaller size.

Meanwhile, the second is to pay attention to how much an item costs per 100g or 100ml, as this can be an easy way of finding out when prices change.

What have the companies said?

A spokeswoman for Mondelez International, which makes Cadbury products, said any change to product sizes are a “last resort”, but it’s facing “significantly higher input costs across our supply chain” – including for energy.

A Nestle spokesman said it was seeing “significant increases in the cost of coffee”, and some “adjustments” were occasionally needed “to maintain the same high quality and delicious taste that consumers know and love”.

“Retail pricing is always at the discretion of individual retailers,” they added.

A spokesman for the Food and Drink Federation also pointed to government policy, notably national insurance increases for employers and a new packaging tax.

Is inflation reaching its peak?

Fresh food prices on the rise

The Which? report comes as latest figures showed fresh food costs 4.3% more than it did a year ago.

The increase in October, reported by the British Retail Consortium (BRC) and market researchers NIQ, was up on the 4.1% year-on-year rise in September.

Overall food inflation was down slightly, though, to 3.7% from last month’s 4.2%.

Read more from Sky News:

Surprise move for Costa Coffee

Start-ups issue warning to Reeves

There has also been a slowdown in overall shop price inflation, which the BRC said was down to “fierce competition among retailers” ahead of Black Friday sales.

The annual shopping extravaganza will this year arrive in the same week as the chancellor’s budget, which is set for Wednesday 26 November.

BRC chief executive Helen Dickinson called on Rachel Reeves to help “relieve some pressures” keeping prices high, with the national insurance rise in last year’s budget having “directly contributed to rising inflation”.

“Adding further taxes on retail businesses would inevitably keep inflation higher for longer,” Ms Dickinson warned.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024