hits a road bump in third-quarter earnings, but things are looking up from here")

Rivian (RIVN) hits a road bump in third-quarter earnings, but things are looking up from here

EV maker Rivian (RIVN) released its third-quarter financial earnings Thursday after the market closed. With fewer deliveries in the quarter, Rivian’s revenue missed expectations. However, the EV maker promises things are looking up from here. Here’s a breakdown of Rivian’s Q3 2024 financial earnings

Earnings preview

Yesterday, Electrek posted a preview of what to look out for in Rivian’s third-quarter earnings. One of the biggest things investors will be watching is Rivian’s top line.

After a supply shortage caused Rivian to lower its production goal for 2024, the company now expects to build between 47,000 and 49,000 vehicles this year, down from the previous 57,000 target.

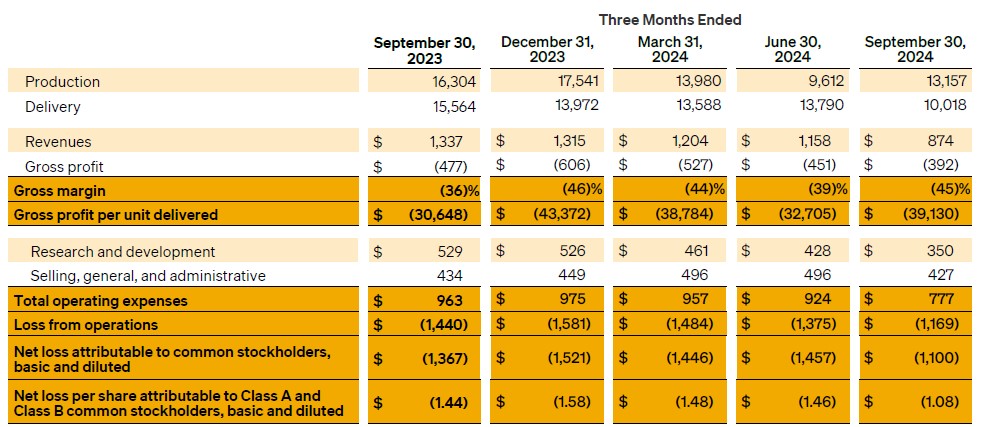

With another 13,157 EVs built last quarter, Rivian’s production total reached 36,749 through September. To hit its target, Rivian will need to build another 10,251 to 12,251 vehicles in Q4.

Despite this, Rivian still expects slight delivery growth over last year, with between 50,500 and 52,000 units delivered in 2024, up from 50,122 in 2023.

According to Estimize, Rivian is expected to report a loss of $0.96 per share in Q3 2024, an improvement from the 1.19 loss per share last year. Rivian is expected to report revenue of around $1 billion, which would be a 25% drop from the $1.34 billion generated in Q3 2023.

Rivian Q3 2024 earnings breakdown

Rivian reported third-quarter revenue of $874 million, a nearly 35% drop from Q3 2023 and missing expectations.

The company said higher electric delivery van (EDV) deliveries for Amazon last year was partly the reason for the lower top-line total.

Rivian posted a gross profit loss of $392 million, down from the $477 million loss last year due to the lower delivery total. Meanwhile, operating losses also fell to $1.17 billion, down from $1.44 billion in Q3 2023.

The company lost $39,130 on every vehicle delivered in Q3 2024, which is up from $30,648 last year and $32,705 in Q2 2024.

| Q3 ’22 | Q4 ’22 | Q1 ’23 | Q2 ’23 | Q3 ’23 | Q4 ’23 | Q1 ’24 | Q2 ’24 | Q3 ’24 | |

| Rivian loss per vehicle | $139,277 | $124,162 | $67,329 | $32,594 | $30,500 | $43,372 | $38,784 | $32,705 | $39,130 |

Rivian’s net loss in the third quarter was $1.1 billion, down from $1.34 billion last year with a $1.08 loss per share.

The EV maker confirmed it’s still on track for a positive gross profit in the fourth quarter of 2024. Rivian’s CEO, RJ Scaringe, said the company is seeing “meaningful progress” on its material costs with new tech and manufacturing processes.

| Q1 2024 | Q2 2024 | Q3 2024 | 2024 YTD | 2024 guidance | |

| Deliveries | 13,588 | 13,790 | 10,018 | 37,396 | 50,500 – 52,000 |

| Production | 13,980 | 9,612 | 13,157 | 36,749 | 47,000 – 49,000 |

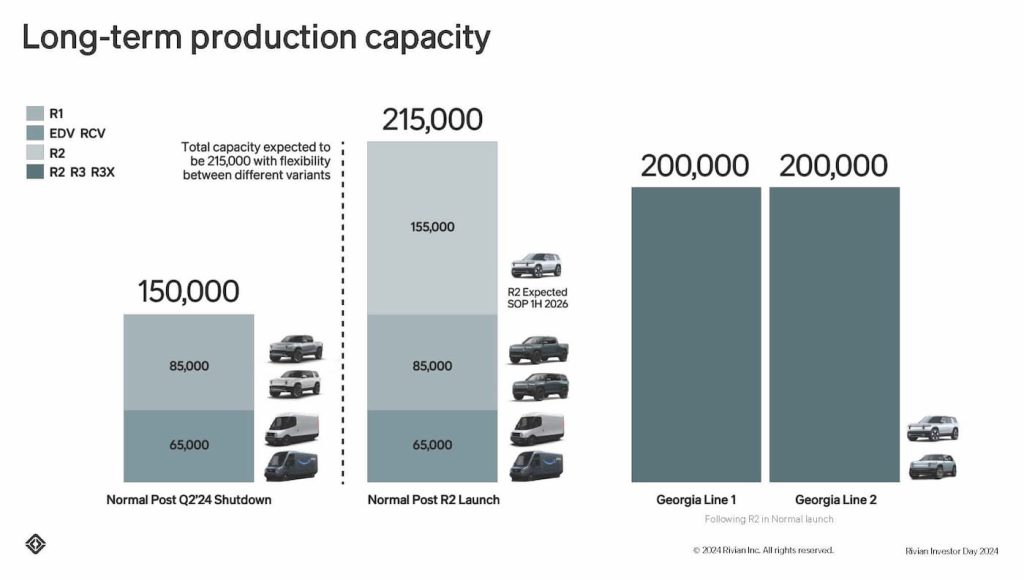

These improvements are meaningful steps toward its next-gen R2, which will launch in the first half of 2026.

Scaringe said Rivian believes R2 will be a “fundamental driver of Rivian’s growth.” It will start at $45,000, nearly half the cost of its current R1S and R1T models.

Once R2 production begins, Rivian expects the new EV will account for most of its output. The company plans to build 155,000 R2 models annually and about 85,000 R1S and R1Ts in Normal.

Rivian also believes its new alliance with Volkswagen will be “a landmark development for the industry.” The total deal size is up to $5 billion, which Rivian said is a “meaningful financial opportunity.”

The planned investments in addition to Rivian’s current cash and equivalents “are expected to provide the capital to fund Rivian’s operations through the ramp of R2 in Normal, as well as the midsize platform in Georgia,” the company said. This will establish a path to positive free cash flow and meaningful scale.

The company ended the quarter with $6.7 billion in cash and equivalents, including a $1 billion convertible note from Volkswagen. Rivian reaffirmed its (revised) production and delivery targets for 2024.

Due to the lower production outlook, Rivian now expects an EBITDA loss of $2.83 billion to $2.88 billion, compared to the previous guidance of a $2.7 billion loss.

Check back for more following Rivian’s earnings call with investors. We will post updates below.

FTC: We use income earning auto affiliate links. More.

Environment

New U.S. nuclear power boom begins with old, still-unsolved problem: What to do with radioactive waste

Castor containers for high-level radioactive waste.

Ina Fassbender | Afp | Getty Images

Nuclear power is back, largely due to the skyrocketing demand for electricity, including big tech’s hundreds of artificial intelligence data centers across the country and the reshoring of manufacturing. But it returns with an old and still-unsolved problem: storing all of the radioactive waste created as a byproduct of nuclear power generation.

In May, President Trump issued executive orders aimed at quadrupling the current nuclear output over the next 25 years by accelerating construction of both large conventional reactors and next-gen small modular reactors. Last week, the U.S. signed a deal with Westinghouse owners Cameco and Brookfield Asset Management to spend $80 billion to build nuclear plants across the country that could result in Westinghouse attempting to spinoff and IPO a stand-alone nuclear power company with the federal government as a shareholder.

There’s a growing consensus among governments, businesses and the public that the time is right for a nuclear power renaissance, and even if the ambitious build-out could take a decade or more and cost hundreds of billion of dollars, it will be an eventual boon to legacy and start-up nuclear energy companies, the AI-fixated wing of the tech industry and investors banking on their success.

But there are plenty of reasons to be skeptical. Only two nuclear power plants have been built since 1990 — more than $15 billion over budget and years behind schedule — and they went online in just the last two years. Almost all of the 94 reactors currently operating in 28 states, generating about 20% of the nation’s electricity, were built between 1967 and 1990. And though often unspoken, there’s the prickly issue that’s been grappled with ever since the first nuclear energy wave during the 1960s and ’70s: how to store, manage and dispose of radioactive waste, the toxic byproduct of harnessing uranium to generate electricity — and portions of which remain hazardous for millennia.

Solutions, employing old and new technologies, are under development by a number of private and public companies and in collaboration with the Department of Energy, which is required by law to accept and store spent nuclear fuel.

The most viable solution for permanently storing nuclear waste was first proffered back in 1957 by the National Academy of Sciences. Its report recommended burying the detritus in deep underground repositories (as opposed to the long-since-abandoned notion of blasting it into low-Earth orbit). It wasn’t until 1982, though, that Congress passed the Nuclear Waste Policy Act, assigning the DOE responsibility for finding such a site.

Five years later, lawmakers designated Yucca Mountain, a 6,700-foot promontory about 100 miles northwest of Las Vegas, Nevada, as the nation’s sole geological repository. Thus began a contentious, years-long saga — involving the Nuclear Regulatory Commission, legislators, lawyers, geologic experts, industry officials and local citizens — that delayed, defunded and ultimately mothballed the project in 2010.

Other nations have moved forward with the idea. Finland, for instance, is nearing completion of the world’s first permanent underground disposal site for its five reactors’ waste. Sweden has started construction on a similar project, and France, Canada and Switzerland are in the early stages of their subterranean disposal sites.

Workers inspect the Repository in ONKALO, a deep geological disposal underground facility, designed to safely store nuclear waste, on May 2, 2023, on the island of Eurajoki, western Finland.

Jonathan Nackstrand | Afp | Getty Images

An American startup, Deep Isolation Nuclear, is combining the underground burial concept with oil-and-gas fracking techniques. The methodology, called deep borehole disposal, is achieved by drilling 18-inch vertical tunnels thousands of feet below ground, then turning horizontal. Corrosion-resistant canisters — each 16 feet long, 15 inches in diameter and weighing 6,000 pounds — containing nuclear waste are forced down into the horizontal sections, stacked side-by-side and stored, conceivably, for thousands of years.

Deep Isolation foresees co-locating its boreholes at active and decommissioned nuclear plants, according to CEO Rod Baltzer. “Eighty percent look like they have good shale or granite formations nearby,” he said, referring to a geologic prerequisite. “That means we would not have to transport the waste” and the risk of highway or railway crashes unleashing radioactive material.

The company has received grants from the DOE’s Advanced Research Projects Agency for Energy program, Baltzer said, and in July closed a reverse merger transaction, an alternative to an IPO for going public. Through that deal, he said, “we raised money for a full-scale demonstration project [in Cameron, Texas]. It will probably be early 2027 by the time we get that fully implemented.”

Recycling radioactive waste for modular reactors

An entirely different, old-is-new-again technology, pioneered in the mid-1940s during the Manhattan Project, is gathering steam. It involves reprocessing spent fuel to extract uranium and other elements to create new fuel to power small modular reactors. The process is being explored by several startups, including Curio, Shine Technologies and Oklo. France has been utilizing reprocessed nuclear fuel at its vast network of reactors since the 1970s.

Oklo has gained attention among investors drawn to its two-pronged approach to nuclear energy. The company — which went public via a SPAC in 2024, after early-stage funding from OpenAI CEO Sam Altman, Peter Thiel’s venture capital firm and others — announced in September that it is earmarking $1.68 billion to build an advanced fuel reprocessing facility in Oak Ridge, Tennessee. Concurrently, the company signed an agreement with the Tennessee Valley Authority “to explore how we can take used nuclear fuel sitting on its sites and convert it into fuel we can use in our reactors,” said a company spokeswoman.

That refers to the TVA’s three nuclear reactors — two in Tennessee, another in Alabama — as well as the other part of Oklo’s business model, which focuses on constructing SMRs. In September, the company broke ground in Idaho Falls, Idaho, on its Aurora fast reactor, a type of SMR that will use reprocessed nuclear fuel. “We’re working on [reprocessing] the fuel right now, so that we can turn on the plant around late 2027 or early 2028,” the Oklo spokeswoman said. The separate Oak Ridge facility, she said, is expected to begin producing fuel by the early 2030s.

Oklo exemplifies both the promise and the perplexity associated with the rebirth of nuclear power. On one hand is the attraction of repurposing nuclear waste and building dozens of SMRs to electrify AI data centers and factories. On the other hand, the company has no facilities in full operation, is awaiting final approval from the NRC for its Aurora reactor, and is producing no revenue. Oklo’s stock has risen nearly 429% this year, with a current market valuation of more than $16.5 billion, but share prices have fluctuated over the past month.

“It’s a high-risk name because it’s pre-revenue, and I anticipate that the company will need to provide more details around its Aurora reactor plans, as well as the [fuel reprocessing] program on the [November 11] earnings report call,” said Jed Dorsheimer, an energy industry analyst at William Blair in a late October interview. “But we haven’t changed our [outperform] rating on the name as of right now,” he added.

Performance of nuclear power company Oklo shares over the past one-year period.

In the meantime, more than 95,000 metric tons of spent nuclear fuel (about 10,000 tons is from weapons programs) sits temporarily stockpiled aboveground in special water-filled pools or dry casks at 79 sites in 39 states, while about 2,000 metric tons are being produced every year. That’s a lot of tonnage, but requires perspective. The Nuclear Energy Institute, the industry’s trade association, states that the entirety of spent fuel produced in the U.S. since the 1950s would cover a football field to a depth of about 12 yards.

But because the DOE, despite its mandate, still hasn’t found a permanent disposal facility for nuclear waste, taxpayers pay utilities up to $800 million every year in damages. Since 1998, the federal government has paid out $11.1 billion, and the tab is projected to reach as much as $44.5 billion in the future.

The DOE’s Department of Nuclear Energy has initiated several programs to address nuclear waste, including coordination with Deep Isolation and Oklo. The agency declined to comment on its efforts in this area, citing the federal government shutdown.

Debate over size of the radiation problem

Opponents to nuclear power cite the well-documented accidents at Three Mile Island in Pennsylvania (1979), Chernobyl in Ukraine (1986) and Fukushima in Japan (2011) — all three which resulted in radiation leaks, and, at Chernobyl and Fukushima, related deaths — as reasons enough to halt building new reactors. Following Fukushima, Japan, Germany and some other nations shut down or suspended operations. Japan has since restarted its nuclear energy program, and its new prime minister, Sanae Takaichi, is expected to accelerate it.

There’s also the viewpoint, related to climate change, that nuclear energy is a emissions-free power source — and unlike solar and wind runs 24/7/365 — that produces relatively manageable waste.

“If you walk up to recently discharged spent fuel and get really close to it, you’ll probably get a lethal dose of radiation,” said Allison Macfarlane, professor and director of the School of Public Policy and Global Affairs at the University of British Columbia, as well as the chair of the NRC from 2012–2014. “But is it this huge, massive problem? No, it’s solvable.” By comparison, she said, “we are under much graver threat from fossil fuel emissions than we are from nuclear waste.”

As far as nuclear waste, “we need to put [it] deep underground,” Macfarlane said.

That was the recommendation of the Blue Ribbon Commission on America’s Nuclear Future, created by the Obama administration in 2010 after the Yucca Mountain project was defunded, on which she served. Macfarlane deems spent fuel reprocessing as far too expensive and a source of new waste streams, and dismisses deep borehole disposal as a “non-starter.”

“You think you’re going to be able to put waste packages down a hole and they’re not going to get stuck on the way?” she said.

Inside the north portal to a five-mile tunnel in Yucca Mountain, 90 miles northwest of Las Vegas.

Las Vegas Review-journal | Tribune News Service | Getty Images

Macfarlane said that the Trump administration’s fast-tracking of new reactors is neither realistic nor achievable, but “I certainly would not support shutting down the operating reactors. I’m not anti-nuclear, but I’m practical.”

She added that while nuclear may not face the current intermittent production challenges of renewables, it is one of the most expensive forms of electricity production, especially compared to utility-scale solar, wind and natural gas.

Nonetheless, the rush to build new reactors — and generate even more waste — marches on alongside the data center boom. Google and NextEra Energy are teaming up to reopen Iowa’s Duane Arnold Energy Center, a nuclear plant that closed five years ago. Microsoft and Constellation Energy plan to restart the Three Mile Island Unit 1 reactor in 2028. And Meta has signed a 20-year power purchase agreement with Constellation and its Clinton, Illinois, nuclear facility.

Although no SMRs have been completed yet in the U.S., several projects are under development by companies including NuScale Power, Holtec International, Kairos Power and X-Energy, which has received backing from Amazon. The only SMR actually under construction is from Bill Gates’ co-founded TerraPower, in Kemmerer, Wyoming, which aims to be operational by the end of 2030.

Those long timelines alone should be a deterrent, said Tim Judson, executive director of the Nuclear Information Resource Service, a nonprofit advocate for a nuclear-free world. “It is fanciful to think that nuclear energy is going to be helpful in dealing with the increases in electricity demand from data centers,” he said, “because nuclear power plants take so long to build and the data centers are being built today.”

And then there’s the waste issue, Judson said. “I’m not sure that the tech industry has really thought through whether they want to be responsible for managing nuclear waste at their data center sites.”

But you can count Gates, the big tech billionaire who was backing nuclear even before the AI data center boom, as having not only thought about the waste problem, but dismissed it as major impediment. “The waste problems should not be a reason to not do nuclear,” Gates said in an interview with the German business publication Handelsblatt back in 2023. “The amount of waste involved … that’s not a reason not to do nuclear. … Say the U.S. was completely nuclear-powered — it’s a few rooms worth of total waste. So it’s not a gigantic thing,” Gates said.

While NIU showed off a full lineup of production-ready electric scooters and motorcycles at EICMA this year, one of the most eye-catching was something you can’t buy just yet – but will definitely want to. It’s called the Concept 06, and it’s NIU’s boldest vision yet for the future of electric two-wheelers.

The Concept 06 is a high-performance electric maxi-scooter that blends power, futuristic design, and rider-focused technology in a way that feels more like a prototype from a sci-fi movie than something from a company best known for urban commuter scooters. But the way the company talks about it, the Concept 06 is actually angling for production instead of just catching eyeballs in the center of the booth.

And with performance like this, let’s hope the rubber does eventually hit the road.

Let’s start with the power: a massive 20kW side-mounted motor launches the Concept 06 to a top speed of 155 km/h (96 mph), putting it firmly in motorcycle territory. The TKX.LAB suspension system is designed to handle aggressive riding while still keeping things smooth over potholes and corners, and dual disc brakes provide serious stopping power.

But it’s the tech where NIU is really showing off. The Concept 06 is packed with smart mobility features that turn the scooter into a responsive, safety-focused machine. A rear radar monitors nearby vehicles and projects ground alerts to warn surrounding traffic. Smart adaptive headlights automatically adjust their beam to your environment, while ambient lighting “breathes” underneath the chassis for a futuristic glow.

Inside, the Concept 06 is built around personalized comfort and high-end convenience. Riders get an electrically adjustable handlebar and windscreen, a tray table (possibly for laptop work during a charging stop), and even future-ready options like wireless charging. Adaptive Cruise Control, Hill-Start Assist, Hill Descent Control, and Push Assist all make daily use more accessible and intuitive.

There’s also full 360° camera coverage with front, rear, and rider-facing cameras, plus a Sentry Mode that activates if someone tampers with the vehicle, sending alerts straight to your phone. Real-time tire pressure monitoring, regenerative braking, and a self-opening saddle round out the long list of rider-focused upgrades.

Electrek’s Take

Of course, this is still a concept vehicle, and it’s unlikely that every single one of these features will make it through to a potential production model. However, the Concept 06 shows that NIU is serious about pushing the boundaries of what an electric scooter can be. And it’s not like we haven’t seen NIU take cool designs that initially seemed far-fetched and ultimately bring them to production.

With high power, top-tier safety tech, and a feature list that rivals high-end EVs, the Concept 06 could be a glimpse at where NIU is going next. Let’s hope they don’t keep this one in the concept cage for long.

FTC: We use income earning auto affiliate links. More.

While the typical buyers of the flagship Mercedes-Maybach EQS 680 may not have to ask what one costs, they do need to know what number to write on the check – and if they happen to be asking this month, that number will be $50,000 LOWER than before.

CarsDirect is reporting a MASSIVE $50,000 lease or purchase cash incentive on the $181,050 top-of-the-line Mercedes-Maybach EQS 680, which amounts to a JC Penney-like 27% discount from the luxo liner’s original asking price and the biggest factory discount deal on any new Mercedes-Benz model so far.

Mercedes-Benz nearly doubled the savings on the 2025 Mercedes-Maybach EQS 680 this month, making it the SUV with the largest rebate offer. The high-end luxury SUV is available with $50,000 in lease cash or purchase cash. Previously, the automaker offered $30,000, making this the best deal to date on the $181,050 vehicle.

For that money, Mercedes-Maybach EQS buyers get Rolls-Royce rivaling material appointments and infotainment features that wouldn’t look out of place in a futuristic sci-fi movie, as well as reclining and massaging rear seats with quilted leather upholstery, lumbar support pillows, and a whole lot more, too.

It’s nice in there

The Maybach EQS 680 is all about opulence, of course – and the list of available features reads exactly the way you’d expect it to on a ride like this. For example: there’s a 12.3″-inch” digital instrument cluster, 17.7″ OLED touchscreen central multimedia display, another 12.3″ OLED display for the front passenger, something called MBUX Hyperscreen, ventilated/rapid-heating front seats so your chauffeur doesn’t get too sweaty, the previously-mentioned massaging seats, “soft close” doors, power side-window sunshades for added privacy, illuminated running boards, and a 64-color choice of interior mood lighting.

Power and torque rarely matter on a ride that you’re more likely to be relaxing in rather than driving, but the big Mercedes doesn’t disappoint in that department, either, thanks to a fully variable 4MATIC AWD system with Torque Shift power vectoring that can send the big SUV’s 649 hp away from the wheels that slip to the wheels that grip, and also work to accelerate inside wheels at a different rate than outside wheels to neutralize handling at the limits.

You know, in case you need to escape the hungry mobs with pitchforks forgot to pick up little Suzie from soccer and need to get there now, Now, NOW!

The big EQS features a 107-ish kWh battery pack good for an EPA-estimated 200 miles of range, with 10-80% charge available in about 30 minutes on a 200 kW DC fast charger. And, trust me, that’s the kind of convenience your personal driver will love.

You can find out more about Mercedes’ killer EV deals on the full range of EQ models, from this top-shelf Maybach on “down” to the also super-discounted compact EQB crossover, below, then let us know what you think of the three-pointed star’s latest discount dash in the comments section at the bottom of the page.

SOURCE: CarsDirect; images via Mercedes-Benz.

If you’re considering going solar, it’s always a good idea to get quotes from a few installers. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024