EVgo shares record Q3 results and double digit YoY growth for eighth consecutive quarter

EV charging network EVgo has published its Q3 2024 financial report, which shows record revenue and tremendous year-over-year growth. EVgo’s growth has continued over the last eight quarters, seven of which saw a triple-digit increase in energy throughput.

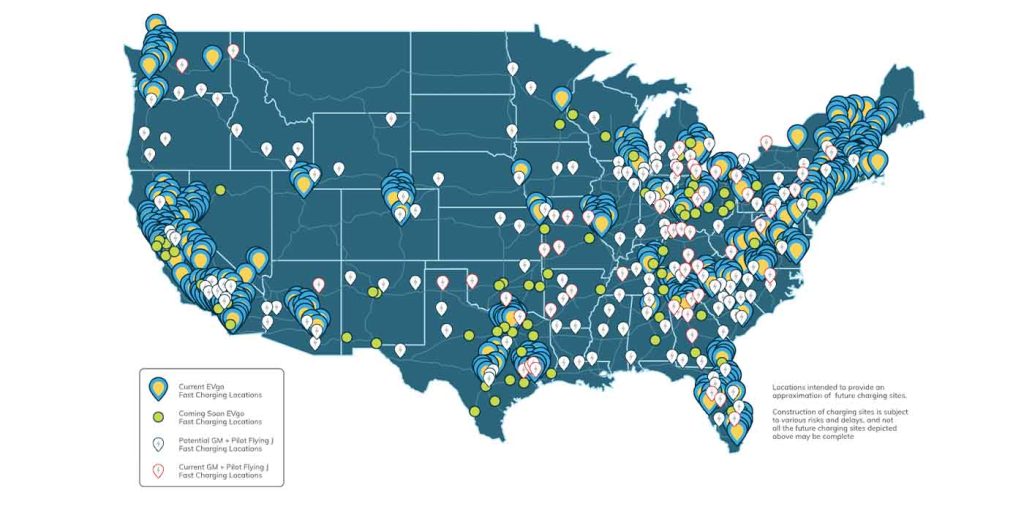

EVgo continues to grow as one of the United States’ largest EV charging networks. Its current footprint consists of over 1,000 fast-charging locations across 40 states, with many more pending, as shown in the company’s service map below.

In May, we reported that EVgo had doubled its registered users in two years, surpassing 1 million active customers. That milestone also saw a 400% increase since April 2020. While some competitors have caught flak for their lack of maintenance and reliability, EVgo has rolled out a “ReNew” program to repair and replace charging piles and ensure customers can replenish their EVs.

Before today’s Q3 report, EVgo had also rolled out several perks and support programs for EV drivers, including access for Tesla owners and fast charging for Hertz rentals, all while rolling out new 350 kW charging stations through partnerships with companies like Pilot/Flying J, and General Motors.

Those efforts appear to be paying off, as EVgo shared record revenue and steady growth in its Q3 2024 financial report.

EVgo added 147K additional customers in Q3 2024

According to EVgo’s Q3 2024 report, the EV charging network achieved record revenue totaling $67.5 million. That’s up from $35.1 million in Q3 of 2023, representing 92% YoY growth.

EVgo’s total throughput increased to 78 GWh last quarter, compared to 37 GWh in Q3 2023, representing 111% growth during that time. The charging network added over 147,000 new customers in Q3, eclipsing 1.2 million users in total, representing a 39% year-over-year increase. Total accounts are up 57% compared to Q3 2023. EVgo CEO Badar Khan spoke:

I’m pleased to report another record quarter anchored by strong revenues and triple digit year-over-year network throughput growth. Our deployment team continued to meet demand head-on bringing a record number of stalls online in the third quarter. With our conditional commitment from DOE for a loan guarantee of up to $1.05 billion announced last month, EVgo is poised to lead the industry as the charging provider of choice. As we look ahead to the end of the year and into fiscal 2025, we are working diligently to complete the loan process, drive our next phase of growth as an owner and operator of fast charging infrastructure, and deliver continued and sustainable value creation for our shareholders.

EVgo shared that its Q3 revenue milestone represents eight sequential quarters of double-digit growth and seven consecutive quarters of triple-digit growth year-over-year in terms of throughput. Here’s EVgo’s Q3 2024 report by the numbers:

- Revenue: $67.5 million

- Network Throughput: 78 gigawatt-hours

- Customer Account Additions: over 147,000 accounts

- Gross Profit: $6.4 million

- Net Loss: $33.3 million

- Adjusted Gross Profit: $18 million

- Adjusted EBITDA: $8.9 million

- Net Cash Provided by Operating Activities: $12.1 million

- Capital Expenditures: $25.8 million

- Capital Expenditures, Net of Capital Offsets: $5.2 million

Following today’s report, EVgo appears poised to continue to grow and could eventually become the nation’s largest EV charging network. As reported in October, the network received a loan from the US Department of Energy totaling $1.05 billion to install 7,500 additional EV fast chargers in the US. EVgo’s anticipated states for charger expansion will be Arizona, California, Florida, Georgia, Illinois, Michigan, New Jersey, New York, Pennsylvania, and Texas.

FTC: We use income earning auto affiliate links. More.

![Classic Jeep Grand Wagoneer gets a battery electric makeover [video]](https://i0.wp.com/electrek.co/wp-content/uploads/sites/3/2025/11/grand-wagoneer_EV_2.jpg?resize=1200,628&quality=82&strip=all&ssl=1)

Texas-based tuning firm Vigilante 4×4 is known for its wild, high-horsepower Jeep SJ Hemi restomods – but they’re more than just a hot rod shop. To prove it, they’ve developed a bespoke, all-electric skateboard chassis designed to turn the classic Jeep Grand Wagoneer into a modern, desirable electric SUV.

The scope of the Vigilante 4×4 electric chassis project is truly impressive. More than just a Jeep SJ frame with an electric drive train bolted in, the chassis is a completely fresh design that utilizes precise 3D scans of the original SJ Wagoneers, Grand Wagoneers, and J-Trucks to establish hard points, then fitted with low-slung battery packs to give the electric restomods superior weight balance, a lower center of gravity, and objectively improved ride and handling compared to its classic, ICE-powered forefathers.

The result is a purpose-built platform that delivers power to the wheels through a dual-motor system – one mounted in the front, and one at the rear – to provide a permanent, infinitely variable four-wheel drive system that offers both on-road performance and the kind of off-road capability that made the Grand Wagoneer famous in the first place.

Vigilante 4×4 electric Jeep SJ

“This isn’t a replacement for our Vigilante HEMI offerings,” reads the official copy. “It’s a total revisit of the Vigilante platform under electric power.”

The company emphasizes that its new chassis is still in the prototype stages. As such, there are no specs, there is no pricing, there are no range estimates. Despite it all, the response from Jeep enthusiasts has already been strong. “Keep in mind this is our first prototype,” a spokesperson said. “There’s still a lot of work to be done – but the journey has begun.”

Electrek’s Take

Retro done wrong – think the Dodge Charger Daytona EV or VW ID.Buzz – is a disaster. Always. If that nostalgic tone is just a little bit off, the song doesn’t work. The heartstrings don’t pull. Done right, however, the siren song of nostalgia will have you putting a second mortgage on your house to put a Singer Porsche or ICON Bronco in your garage.

It’s too soon to tell what side of that line the Vigilante 4×4 Jeep SJ will eventually fall, but one thing (at least) is certain: it’s closer to the mark than that Wagoneer S.

SOURCE | IMAGES: Vigilante 4×4, via Mopar Insiders.

If you’re considering going solar, it’s always a good idea to get quotes from a few installers. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

EQORE, a distributed battery storage startup based in Somerville, Massachusetts, has raised $1.7 million in seed funding to help industrial buildings tackle rising electricity costs. The round was oversubscribed and includes backing from the Massachusetts Clean Energy Center (MassCEC), Henry Ford III of Ford Motor Company, and Jonathan Kraft of The Kraft Group.

The timing couldn’t be more relevant. Data centers are booming, and that demand is slamming an already stressed grid. Big, utility-scale batteries help at the grid level, but they can’t fix the bottlenecks happening on local distribution networks. That’s where onsite storage steps in — storing energy when demand is low and discharging it when demand spikes, which helps stabilize costs for both the grid and the businesses using it.

MassCEC’s head of investments, Susan Stewart, said, “What excites us the most about EQORE’s technology is the dual impact: grid support and customer savings.” She noted that commercial and industrial buildings are ideal hosts for battery storage, but haven’t gotten much attention until now. “EQORE is closing that gap.”

Investor Randolph Mann highlighted what makes the company stand out: “By uniting advanced controls with high‑resolution metering and true end‑to‑end service, EQORE finally makes commercial behind-the-meter storage effortless and financially compelling for businesses.”

EQORE comes out of MIT’s Sandbox program and delta v accelerator and is currently part of the Harvard Climate Entrepreneurs Circle incubator. CEO and cofounder Valeriia Tyshchenko, a third‑generation engineer from Ukraine and MIT graduate, said the new funding will help the company scale alongside its existing revenue.

With the seed round closed, EQORE plans to grow its team and ramp up battery deployments at energy-intensive manufacturing facilities. The company doesn’t just install batteries; it operates them. Its autonomous software shifts when a facility uses power based on market conditions and utility incentives, reshaping load in real-time without disrupting operations.

Read more: Battery boom: 5.6 GW of US energy storage added in Q2

If you’re looking to replace your old HVAC equipment, it’s always a good idea to get quotes from a few installers. To make sure you’re finding a trusted, reliable HVAC installer near you that offers competitive pricing on heat pumps, check out EnergySage. EnergySage is a free service that makes it easy for you to get a heat pump. They have pre-vetted heat pump installers competing for your business, ensuring you get high quality solutions. Plus, it’s free to use!

Your personalized heat pump quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here. – *ad

FTC: We use income earning auto affiliate links. More.

![Check out Hyundai's cool new off-road electric SUV concept [Images]](https://i0.wp.com/electrek.co/wp-content/uploads/sites/3/2025/11/Hyundai-off-road-SUV.jpeg?resize=1200,628&quality=82&strip=all&ssl=1)

Hyundai took the sheets of its new off-road electric SUV, the Crater Concept, at the LA Auto Show. Here’s our first look at the compact off-roader.

Meet Hyundai’s new off-road SUV, the Crater Concept

We knew it was coming after Hyundai teased the off-road SUV earlier this week, hidden under a drape. Hyundai took the sheets off the Crater Concept at the LA Auto Show on Thursday, giving us our first real look at the rugged off-roader.

Hyundai refers to it as a compact off-road SUV that’s inspired by extreme events. The concept was brought to life at the Hyundai America Technical Center in Irvine, California.

The off-road SUV draws design elements from Hyundai’s Extra Rugged Terrain (XRT) models, such as the IONIQ 5 XRT, Santa Cruz XRT, and the new Pallisade XRT Pro.

Although it’s a concept, Hyundai said the Crater Concept is a testament to its commitment to designing future XRT vehicles that are more functional, more capable, and more emotional.

“CRATER began with a question: ‘What does freedom look like?’ This vehicle stands as our answer,” Hyundai’s global design boss, SangYup Lee said.

The off-road SUV features Hyundai’s new Art of Steel design theme, first showcased on the THREE concept at the Munich Motor Show in September.

Hyundai said the design team was guided by one clear goal: To create a rugged and capable vehicle that’s designed to go anywhere. The Crater Concept embodies that vision with added wide skid plates, 33″ off-road tires, limb risers, rocker panels, and a roof platform.

Hyundai designed the interior for “tech-savvy adventure seekers,” with a singular design centered around a high-brow crash pad that stretches across the dashboard.

The concept also swaps the traditional infotainment setup for a head-up display that spans the entire front window, which Hyundai said includes a live rearview camera.

Hyundai’s off-roader includes a new Off-Road Controller for front and rear locking differentials, as well as a terrain selector with modes including Sand, Snow, and Mud. Other off-road features include downhill brake control, trailer brake control, a compass, and an altimeter.

Although Hyundai said it was electric, it didn’t reveal any further details about the powertrain. The off-road SUV could be a battery-electric or fuel-cell-electric vehicle.

Like the new Nexo, Hyundai’s hydrogen fuel cell vehicle, the concept features “HTWO” lamps exclusive to its FCEVs.

Earlier this week, the design team at Hyundai Design North America also introduced its new design and ideation studio codenamed “The Sandbox.” The creative design studio is set to serve as a global hub for future XRT vehicles and gear.

FTC: We use income earning auto affiliate links. More.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024