US House kills IRS DeFi broker rule, Solana won’t cut 80% inflation rate: Finance Redefined

In a significant regulatory development for the crypto industry, the United States House of Representatives voted to nullify a bill that threatened the privacy-preserving properties of decentralized finance (DeFi) protocols.

In the wider crypto space, one of the Solana network’s most significant governance proposals was rejected; it sought to implement a mechanism to reduce Solana’s inflation rate by about 80%.

US House follows Senate in passing resolution to kill IRS DeFi broker rule

The US House of Representatives voted to nullify a rule requiring decentralized finance (DeFi) protocols to report to the Internal Revenue Service.

On March 11, the House of Representatives voted 292 for and 132 against a motion to repeal the so-called IRS DeFi broker rule that aimed to expand existing IRS reporting requirements to crypto.

All 132 votes to keep the rule were Democrats. However, 76 Democrats joined with the Republicans to repeal it.

This followed the Senate’s March 4 vote on the motion, which saw it pass 70 to 27.

The rule would have forced DeFi platforms, such as decentralized exchanges, to disclose gross proceeds from crypto sales, including information regarding taxpayers involved in the transactions.

After the vote, Republican Representative Mike Carey, who submitted the repeal motion, said, “The DeFi broker rule invades the privacy of tens of millions of Americans, hinders the development of an important new industry in the United States and would overwhelm the IRS.”

Congressman Mike Carey speaking after the vote. Source: Mike Carey

Solana proposal to cut inflation rate by up to 80% fails

A proposal to dramatically change Solana’s inflation system was rejected by stakeholders but is being hailed as a victory for the network’s governance process.

“Even though our proposal was technically defeated by the vote, this was a major victory for the Solana ecosystem and its governance process,” commented Multicoin Capital co-founder Tushar Jain on March 14.

Around 74% of the staked supply voted on proposal SIMD-228 across 910 validators, but just 43.6% voted in favor of it, with 27.4% voting against it and 3.3% abstaining, according to Dune Analytics. It needed 66.67% approval from participating votes to pass and only received 61.4%.

Jain added that this was the biggest crypto governance vote ever, by the number of participants and the participating market cap, of any ecosystem, chain or network.

“This was a meaningful scaling stress test — a social, rather than technical, stress test — and the network passed despite a wide stratification of diverging opinions and interests.”

Bitcoin $70,000 retracement part of “macro correction” in bull market — Analysts

Bitcoin’s potential retracement to $70,000 may be an organic part of the current bull market, despite crypto investor fears of an early arrival of a bear market cycle.

Bitcoin (BTC) fell more than 14% during the past week to close at around $80,708 after investors were disappointed with the lack of direct federal Bitcoin investments in President Donald Trump’s March 7 executive order. It outlined a plan to create a Bitcoin reserve using cryptocurrency forfeited in government criminal cases.

Despite the drop in investor sentiment, cryptocurrencies and global markets remain in a “macro correction” as part of the bull market, according to Aurelie Barthere, principal research analyst at the Nansen crypto intelligence platform.

BTC/USD, 1-month chart. Source: Cointelegraph

Most cryptocurrencies have broken key support levels, making it hard to estimate the next key price levels, the analyst told Cointelegraph, adding:

“This is a macro correction (US tech will be down by 3% in the future, as discussed), so we have to monitor BTC. Next level will be $71,000 – $72,000, top of the pre-election trading range.”

The analyst added: “We are still in a correction within a bull market: Stocks and crypto have realized and are pricing; a period of tariff uncertainty and fiscal cuts, no Fed put. Recession fears are popping up.”

Calls for stricter rules on political memecoins after $4 billion Libra collapse

Industry voices warned that politically endorsed cryptocurrencies must adopt stronger investor protections and liquidity safeguards to prevent another significant market collapse.

Investor sentiment remains shaken after the Libra (LIBRA) token, which was endorsed by Argentine President Javier Milei, suffered a $4 billion market cap wipeout due to insider cash-outs.

According to blockchain analytics firm DWF Labs, at least eight insider wallets withdrew $107 million in liquidity, triggering the massive collapse.

Source: Kobeissi Letter

To avoid a similar meltdown, tokens with presidential endorsements will need more robust safety and economic mechanisms, such as liquidity locking or making the tokens in the liquidity pool non-sellable for a predetermined period, DWF Labs wrote in a report shared with Cointelegraph.

The report stated that tokens from high-profile leaders also need launch restrictions to limit participation from crypto-sniping bots and large holders or whales.

“Limiting bot and whale activity is essential in limiting the impact of individuals acting on insider information to corner a large percentage of the token supply,” according to Andrei Grachev, managing partner at DWF Labs.

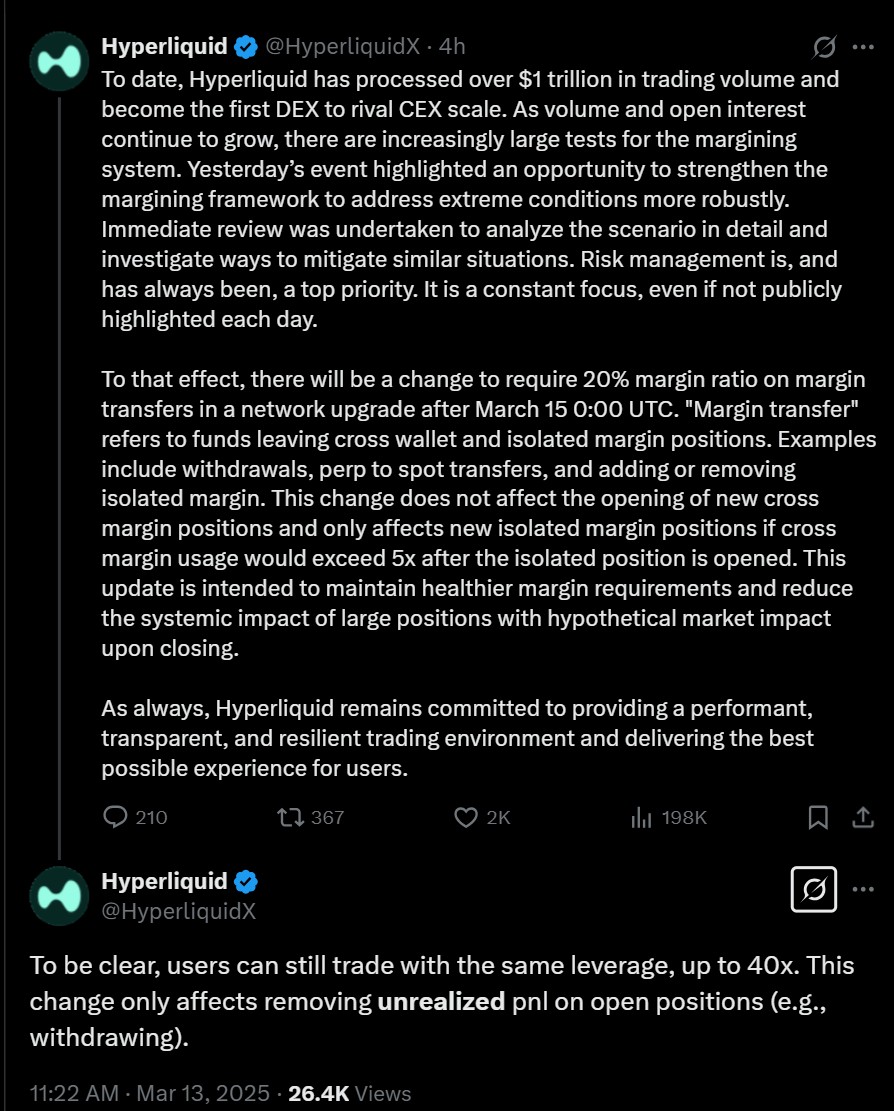

Hyperliquid ups margin requirements after $4 million liquidation loss

Hyperliquid, a blockchain network specializing in trading, increased margin requirements for traders after its liquidity pool lost millions of dollars during a massive Ether (ETH) liquidation, the network said.

On March 12, a trader intentionally liquidated a roughly $200 million Ether long position, causing Hyperliquid’s liquidity pool, HLP, to lose $4 million, unwinding the trade.

Starting March 15, Hyperliquid will require traders to maintain a collateral margin of at least 20% on certain open positions to “reduce the systemic impact of large positions with hypothetical market impact upon closing,” Hyperliquid said in a March 13 X post.

The incident highlights the growing pains confronting Hyperliquid, which has emerged as Web3’s most popular platform for leveraged perpetual trading.

Hyperliquid has adjusted margin requirements for traders. Source: Hyperliquid

Hyperliquid said the $4 million loss was not from an exploit but rather a predictable consequence of the mechanics of its trading platform under extreme conditions.

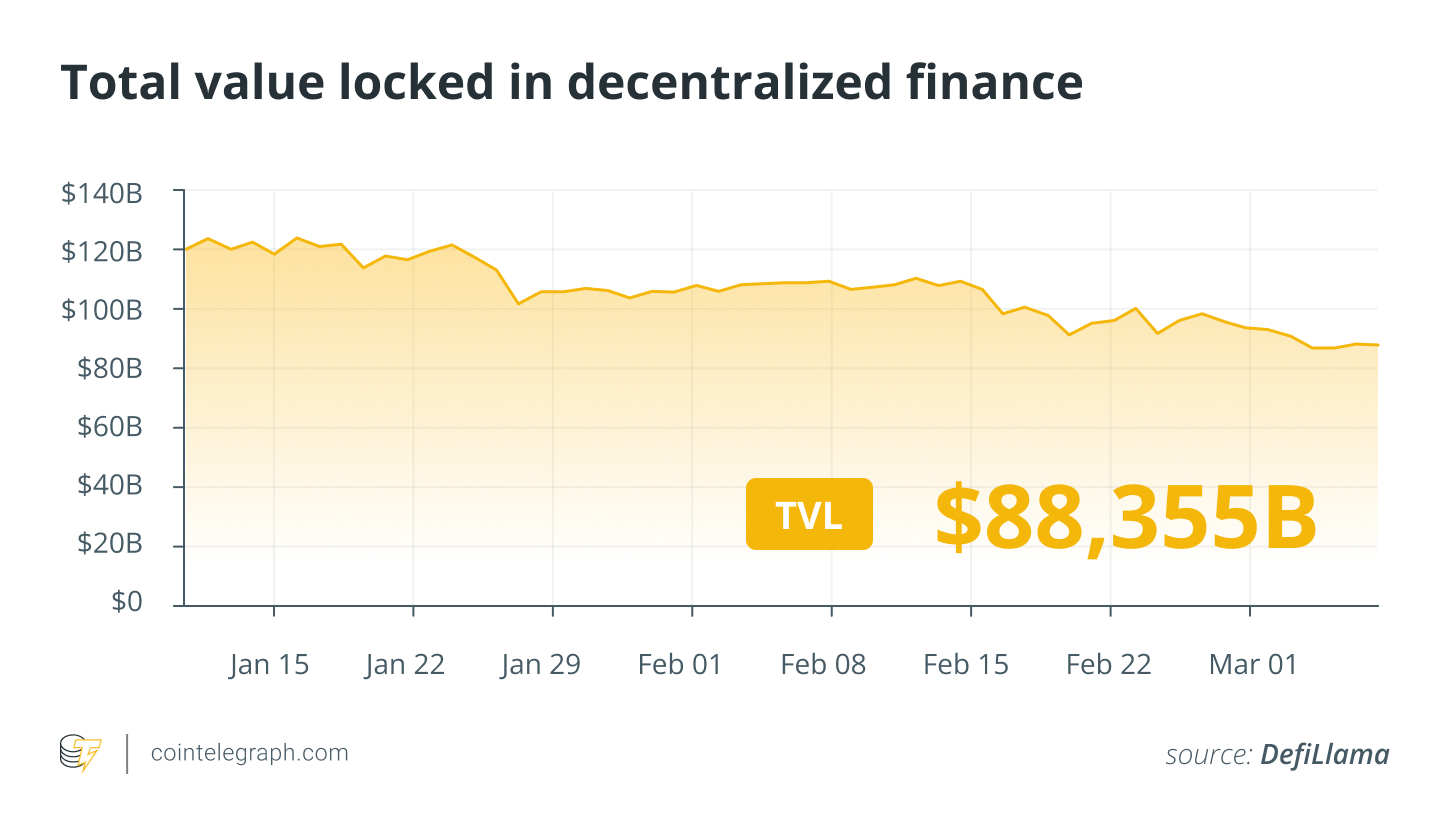

DeFi market overview

According to data from Cointelegraph Markets Pro and TradingView, most of the 100 largest cryptocurrencies by market capitalization ended the week in the red.

Of the top 100, the Hedera (HBAR) token fell over 24%, marking the biggest weekly decrease, followed by JasmyCoin (JASMY) down over 21% over the past week.

Total value locked in DeFi. Source: DefiLlama

Thanks for reading our summary of this week’s most impactful DeFi developments. Join us next Friday for more stories, insights and education regarding this dynamically advancing space.

Sir Keir Starmer will deliver a speech today defending the decisions the government made in the budget, following criticisms of sweeping tax rises and accusations the chancellor lied to the country about the state of public finances.

The prime minister is expected to set out how the budget, which saw £26bn of tax rises imposed across the economy, “moves forward the government’s programme of national renewal”, and set “the right economic course” for Britain, Downing Street says.

He will also confirm that ministers will try again to reform the “broken” welfare system, after Labour MPs forced the government to U-turn on its plans to narrow the eligibility for Personal Independence Payments (PIP) earlier this year.

Sir Keir Starmer will give a speech later defending last week’s budget. Pic: Reuters

‘Of course I didn’t’ lie about public finances, says Reeves

“We have to confront the reality that our welfare state is trapping people, not just in poverty, but out of work – young people especially. And that is a poverty of ambition,” Sir Keir will say.

“And so while we will invest in apprenticeships and make sure every young person without a job has a guaranteed offer of training or work, we must also reform the welfare state itself – that is what renewal demands.”

Sky’s Ed Conway looks at the aftermath of the budget and explains who the winners and losers are

The prime minister will add: “This is not about propping up a broken status quo. Nor is it because we want to look somehow politically ‘tough’. The Tories played that game and the welfare bill went up by £88bn. They left children too poor to eat and young people too ill to work. A total failure.”

Instead, he will argue it is about “potential”, saying: “If you are ignored that early in your career, if you’re not given the support you need to overcome your mental health issues, or if you are simply written off because you’re neurodivergent or disabled, then it can trap you in a cycle of worklessness and dependency for decades, which costs the country money, is bad for our productivity, but most importantly of all – costs the country opportunity and potential.

“And any Labour Party worthy of the name cannot ignore that. That is why we have asked Alan Milburn on the whole issue of young people, inactivity and work. We need to remove the incentives which hold back the potential of our young people.”

The announcement will come after the Conservative opposition described the budget as one for “benefits street”, following the chancellor’s decision to lift the two-child benefit cap from April, at a cost of £3bn.

Prime Minister defends the budget

‘Government must go further and faster on growth’

The prime minister is also expected to launch a staunch defence of the budget overall, saying it will bear down on the cost of living through measures like money off energy bills and frozen rail fares; increase economic stability; and protect investment in public services and infrastructure that will drive economic growth.

He will argue that “economic growth is beating the forecasts”, but that the government must go “further and faster” to encourage it.

He will also reiterate his vow to scrap regulation across the economy, which he will argue is not only pro-business, but also a way to deal with the cost of living.

How will your personal finances change following the budget announced by the chancellor?

“Rooting out excessive costs in every corner of the economy is an essential step to lower the cost of living for good, as well as promoting more dynamic markets for business,” the prime minister will say.

He will confirm reforms to the building of nuclear power plants, after the government’s nuclear regulatory taskforce found that “pointless gold-plating, unnecessary red-tape and well-intentioned, but fundamentally misguided environmental regulation had made Britain the most expensive place to build nuclear power”.

“We urgently need to correct this,” the prime minister will say.

Business secretary Peter Kyle will be tasked with applying the same deregulatory approach to major infrastructure schemes and to accelerate the implementation of Labour’s industrial strategy.

In response, Tory shadow chancellor Sir Mel Stride said: “It is frankly laughable to hear the prime minister say Rachel Reeves’s Benefits Street budget has put the country on the right course and that he wants to fix the welfare system.

“His chancellor has just hiked taxes by £26bn to pay for a welfare splurge, penalising people who work hard and making them pay for those who don’t work at all. And she misrepresented why she was doing it, claiming there was a fiscal black hole to fill that she knew didn’t exist.

“Labour’s leadership have repeatedly shown they lack the backbone to tackle welfare and instead are just acting to placate their left-wing backbenchers.”

Rachel Reeves tells Sky News she did not lie about the state of the public finances

Chancellor accused of ‘lying’

Sir Mel is referring to the chancellor’s speech on 4 November in which she laid the ground for tax rises due to the decision by the independent Office for Budget Responsibility (OBR) to review and downgrade productivity over recent years, at a cost of £16bn, which led to a black hole in the public finances.

But the OBR revealed on Friday that it had told the Treasury days earlier that there was actually a budget surplus of £4.2bn, leading to outrage and claims that she misled the country about the state of the public finances.

Rachel Reeves was asked directly by Sky’s Trevor Phillips if she lied, and she replied: “Of course I didn’t.”

Why did Reeves make the situation sound ‘so bleak’?

She said: “I said in that speech that I wanted to achieve three things in the budget – tackling the cost of living, which is why I took £150 off of energy bills and froze prescription charges and rail fares.

“I wanted to continue to cut NHS waiting lists, which is why I protected NHS spending. And I wanted to bring the debt and the borrowing down, which is one of the reasons why I increased the headroom.

“£4bn of headroom would not have been enough, and it would not give the Bank of England space to continue to cut interest rates.”

Ms Reeves also said: “In the context of a downgrade in our productivity, which cost £16bn, I needed to increase taxes, and I was honest and frank about that in the speech that I gave at the beginning of November.”

Badenoch says Rachel Reeves should resign

But Tory leader Kemi Badenoch said: “I think the chancellor has been doing a terrible job. She’s made a mess of the economy, and […] she has told lies. This is a woman who, in my view, should be resigning.”

Report due on OBR breach

The tumultuous run-up to the 26 November budget culminated in the OBR accidentally publishing its assessment of the chancellor’s measures 45 minutes before the speech began, in what was an unprecedented breach of budget security.

👉 Listen to Sky News Daily on your podcast app 👈

The chair of the OBR, Richard Hughes, apologised for the “error”, and announced an investigation into how it happened.

The chancellor has said that she retains confidence in him, despite the “serious breach of protocol”, and confirmed to Trevor that the investigation report will be delivered to her on Monday, although it is not clear when it will be published.

China’s central bank has flagged stablecoins as a risk and has promised to refresh its crackdown on crypto trading, which it has banned since 2021.

The People’s Bank of China said on Saturday, after a meeting with 12 other agencies, that “virtual currency speculation has resurfaced” due to various factors, posing new challenges for risk control.

“Virtual currencies do not have the same legal status as fiat currencies, lack legal tender status, and should not and cannot be used as currency in the market,” the bank said, according to a translation of its statement.

“Virtual currency-related business activities constitute illegal financial activities.”

China’s central bank banned crypto trading and mining in 2021, citing a need to curb crime and claiming that crypto posed a risk to the financial system.

Bank says stablecoins of concern

China’s central bank highlighted stablecoins as a particular concern, stating that the tokens weren’t meeting legal requirements and were being used in criminal activities.

“Stablecoins are a form of virtual currency, and currently cannot effectively meet requirements for customer identification and Anti-Money Laundering, posing a risk of being used for illegal activities such as money laundering, fundraising fraud, and illegal cross-border fund transfers,” the bank said.

{kind=link}

The bank said it would “persistently crack down on illegal financial activities” related to crypto to “maintain the stability of the economic and financial order.”

Related: South Korea targets sub-$680 crypto transfers in sweeping AML crackdown

The 13 agencies that attended the meeting stated that they would “deepen coordination and cooperation” in tracking down crypto users by strengthening information sharing and enhancing monitoring capabilities.

Reuters reported on Wednesday that China had the third-highest share of Bitcoin (BTC) mining, with its market share reaching 14% by the end of October.

In August, China’s financial regulators reportedly instructed brokers to cancel seminars and stop promoting research on stablecoins over concerns that it could be exploited as a tool for fraudulent activities.

Meanwhile, Hong Kong opened the doors to licensing stablecoin issuers in July, but some tech companies suspended plans to launch stablecoins in the region after Chinese regulators reportedly intervened to pause the offerings.

Magazine: Koreans ‘pump’ alts after Upbit hack, China Bitcoin mining surge: Asia Express

White House AI and crypto czar David Sacks has fired back at The New York Times over a report detailing how his government advisory role could benefit his investments and those of his close associates.

Sacks said in a post to X that despite having “debunked in detail” the Times’ reporting over the past five months, the outlet continued to publish the article on Sunday about his supposed conflicts of interest.

“Today they evidently just threw up their hands and published this nothing burger,” Sacks wrote. “Anyone who reads the story carefully can see that they strung together a bunch of anecdotes that don’t support the headline.”

Sacks is a co-founder and partner at the venture firm Craft Ventures, and his special government employee role at the White House has drawn scrutiny in the past, with Democrat Senator Elizabeth Warren saying in May that he is “financially invested in the crypto industry, positioning him to potentially profit from the crypto policy changes he makes at the White House.”

Before he became crypto czar, Sacks and Craft divested over $200 million in crypto and crypto-tied stocks, at least $85 million of which Sacks owned, but Sacks retained an interest in several illiquid investments of “private equity of digital asset-related companies.”

Sacks retains 20 crypto investments, The Times reports

The Times reported that its analysis of Sacks’ financial disclosure found he has retained 708 tech investments, 449 of which are AI-related and 20 are tied to crypto, all of which could benefit from the policies Sacks supports.

In one example of a perceived conflict in Sacks’ role, the outlet stated that Craft Ventures is invested in the crypto infrastructure company BitGo, which offers a stablecoin-as-a-service.

BitGo filed to go public in September, with regulatory filings showing Craft owned 7.8% of the company.

The Times noted that Sacks was a major backer of the stablecoin-regulating GENIUS Act, which was signed into law earlier this year. Many crypto commentators predicted that this would boost the use and adoption of the tokens by institutions.

Related: Trump-linked ALT5 Sigma shakes up leadership amid WLFI scrutiny

Other examples noted by the Times involved Sacks’ and Craft’s ties to companies involved with AI, which have skyrocketed in value as the White House and Wall Street bet on the technology’s potential.

The Times noted that Sacks’ ethics waivers, shared in March, stated he would sell his interests in AI and crypto; however, they don’t disclose when he sold the assets and do not detail the value of his remaining investments.

NYT created “bogus narrative,” says Sacks

In his X post, Sacks shared a letter to the Times sent by his lawyers at Clare Locke accusing the outlet of setting out “to write a hit piece” and giving their reporters “clear marching orders” to find conflicts of interest.

Sacks added it was “very clear how NYT willfully mischaracterized or ignored the facts to support their bogus narrative.”

Sacks’ spokesperson Jessica Hoffman told the Times that he has complied with rules for special government employees, and the Office of Government Ethics said that Sacks should sell his investments in certain types of companies but not others.

Sacks’ role as a special government employee is limited to 130 days, and in September, Democratic lawmakers questioned whether he had exceeded the number of days allowed with his appointment.

However, Sacks reportedly carefully manages the days he spends as a special government employee to ensure that he stays under the limit.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024