SEC nominee Atkins discloses at least $327M in assets ahead of confirmation hearing

Paul Atkins, US President Donald Trump’s nominee to lead the Securities and Exchange Commission (SEC), disclosed combined employment assets of at least $327 million with his wife ahead of a scheduled confirmation hearing with the US Senate Banking Committee.

Atkins and his wife, Sarah Humphreys, held up to a combined $327 million in assets, in part through their respective stakes in Atkins’ consulting firm Patomak Global Partners and Tamko Building Products, according to a financial disclosure report made public by the US Office of Government Ethics on March 25.

Humphreys and her family members reportedly control a 75% stake in Tamco, the roofing business founded by her grandfather.

Atkins personally disclosed up to $78.8 million in total employment assets of: up to $15,000 each; between $25,000,001 and $50 million in membership interest at Patomak; between $250,001 and $500,000 in call options at Securitize, a real-world asset tokenization platform; and between $50,001 and $100,000 at financial technology company Pontoro.

If confirmed, Atkins he would resign as CEO of Patomak and divest his membership interest, as well as divest his stock options at Securitize. Atkins served as a commissioner at the agency from 2002 to 2008.

The financial disclosure was made public ahead of Atkins’ March 27 appearance before the Senate Banking Committee. Massachusetts Senator Elizabeth Warren, the ranking Democrat on the committee, called on Atkins to be prepared to answer questions related to his “deep involvement with FTX and other high-paying crypto clients.”

Related: What to expect at Paul Atkins’ SEC confirmation hearing

Atkins could also have some Republican allies on the committee and face some softball questions during his hearing. The prospective SEC commissioner previously met with Wyoming Senator Cynthia Lummis, who told Cointelegraph she expected he would “work quickly to provide regulatory certainty for the digital asset industry.”

Conflicts of interest regulating digital assets?

Other Trump administration officials have taken steps to mitigate any appearance of conflicts of interest.

David Sacks, Trump’s artificial intelligence and crypto czar, filed a notice on March 5 suggesting that his venture capital firm sold more than $200 million in crypto and related stocks ahead of assuming his role.

Trump has faced criticism from lawmakers and figures in the crypto industry for his family’s involvement with World Liberty Financial and the launch of his memecoin in January.

Atkins’ hearing will mark the first time US lawmakers will consider his nomination since Trump put his name forward as a replacement former SEC Chair Gary Gensler in December. Commissioner Mark Uyeda became acting chair of the agency following Gensler’s departure on Jan. 20.

Magazine: Trump’s crypto ventures raise conflict of interest, insider trading questions

Emmanuel Macron addressing parliament in the Palace of Westminster’s Royal Gallery was a highly anticipated moment in the long history of our two nations.

That story – the conflict and a historic Anglo-French agreement that ended centuries of feuding, the Entente Cordiale – adorn the walls of this great hall.

Looming over the hundreds of MPs and peers who had gathered in the heat to hear the French president speak, hang two monumental paintings depicting British victories in the Napoleonic wars, while the glass stand in the room commemorates the 408 Lords who lost their lives fighting for Europe in two world wars.

Politics latest: UK and France will get ‘tangible results’ on migration

The French president came to parliament as the first European leader to be honoured with a state visit since Brexit.

It was the first address of a French president to parliament since 2008, and Mr Macron used it to mark what he called a new era in Anglo-Franco relations.

Sky News’ political correspondent Tamara Cohen was watching Emmanuel Macron’s speech. She highlights the president saying he wants to see tangible results on migration.

Peers and MPs cheered with delight when he confirmed France would loan the Bayeux Tapestry to the UK in the run-up to the anniversary of William the Conqueror’s birthday.

“I have to say, it took properly more years to deliver that project than all the Brexit texts,” he joked as former prime minister Theresa May watched on from the front row

From Brexit to migration, European security, to a two-state solution and the recognition of Palestine, Mr Macron did not shy away from thorny issues, as he turned the page on Brexit tensions woven through Anglo-French relations in recent years, in what one peer described to me as a “very political speech rather than just the usual warm words”.

Emmanuel Macron addresses parliament

He also used this address to praise Sir Keir Starmer, sitting in the audience, for his leadership on security and Ukraine, and his commitment to the international order and alliances forged from the ashes of the Second World War. For that, he received a loud ovation from the gathered parliamentarians.

Macron’s first-ever state visit: personal or political?

Read more:

Thatcher loyalist Norman Tebitt dies aged 94

Public finances in ‘relatively vulnerable position’

The test now for Sir Keir is whether he can turn his deft diplomatic work in recent months with Mr Macron into concrete action to give him a much-needed win on the domestic front, particularly after his torrid week on welfare.

The government hopes that France’s aim for “cooperation and tangible results” at the upcoming political summit as part of this state visit, will give Starmer a much-needed boost.

The PM is attempting to drive-down crossings by negotiating a one-in one-out return treaty with France.

Under this plan, those crossing the Channel illegally will be sent back to France in exchange for Britain taking in an asylum seeker with a family connection in the UK.

But as I understand it, the deal is still in the balance, with some EU countries unhappy about France and the UK agreeing on a bilateral deal.

Politics

UK and France have ‘shared responsibility’ to tackle illegal migration, Emmanuel Macron says

Emmanuel Macron has said the UK and France have a “shared responsibility” to tackle the “burden” of illegal migration, as he urged co-operation between London and Paris ahead of a crunch summit later this week.

Addressing parliament in the Palace of Westminster on Tuesday, the French president said the UK-France summit would bring “cooperation and tangible results” regarding the small boats crisis in the Channel.

Politics latest: Lord Norman Tebbit dies, aged 94

Mr Macron – who is the first European leader to make a state visit to the UK since Brexit – told the audience that while migrants’ “hope for a better life elsewhere is legitimate”, “we cannot allow our countries’ rules for taking in people to be flouted and criminal networks to cynically exploit the hopes of so many individuals with so little respect for human life”.

“France and the UK have a shared responsibility to address irregular migration with humanity, solidarity and fairness,” he added.

Looking ahead to the UK-France summit on Thursday, he promised the “best ever co-operation” between France and the UK “to fix today what is a burden for our two countries”.

Sir Keir Starmer will hope to reach a deal with his French counterpart on a “one in, one out” migrant returns deal at the key summit on Thursday.

King Charles also addressed the France-UK summit at the state banquet in Windsor Castle on Tuesday evening, saying it would “deepen our alliance and broaden our partnerships still further”.

King Charles speaking at state banquet welcoming Macron.

Sitting next to President Macron, the monarch said: “Our armed forces will cooperate even more closely across the world, including to support Ukraine as we join together in leading a coalition of the willing in defence of liberty and freedom from oppression. In other words, in defence of our shared values.”

In April, British officials confirmed a pilot scheme was being considered to deport migrants who cross the English Channel in exchange for the UK accepting asylum seekers in France with legitimate claims.

The two countries have engaged in talks about a one-for-one swap, enabling undocumented asylum seekers who have reached the UK by small boat to be returned to France.

👉Listen to Politics at Sam and Anne’s on your podcast app👈

Britain would then receive migrants from France who would have a right to be in the UK, like those who already have family settled here.

The small boats crisis is a pressing issue for the prime minister, given that more than 20,000 migrants crossed the English Channel to the UK in the first six months of this year – a rise of almost 50% on the number crossing in 2024.

President Macron greets Commons Speaker Sir Lindsay Hoyle at his address to parliament in Westminster.

Elsewhere in his speech, the French president addressed Brexit, and said the UK could not “stay on the sidelines” despite its departure from the European Union.

He said European countries had to break away from economic dependence on the US and China.

Read more:

French police forced to watch on as migrants attempt crossing

Public finances in ‘relatively vulnerable position’, OBR warns

“Our two countries are among the oldest sovereign nations in Europe, and sovereignty means a lot to both of us, and everything I referred to was about sovereignty, deciding for ourselves, choosing our technologies, our economy, deciding our diplomacy, and deciding the content we want to share and the ideas we want to share, and the controversies we want to share.

“Even though it is not part of the European Union, the United Kingdom cannot stay on the sidelines because defence and security, competitiveness, democracy – the very core of our identity – are connected across Europe as a continent.”

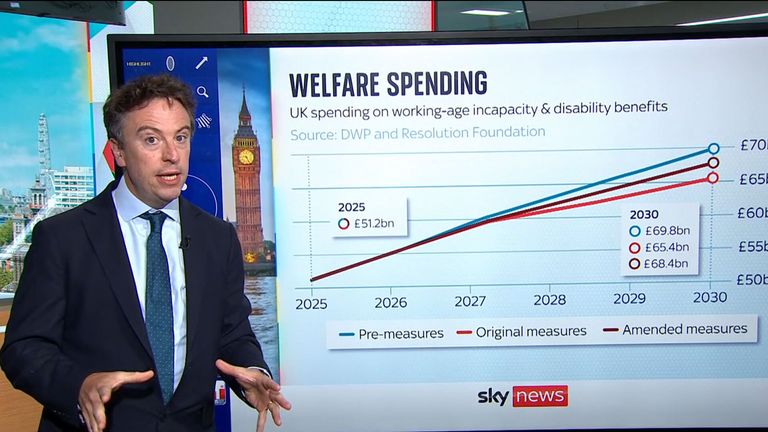

A UN committee on disability rights has criticised the UK government’s welfare reforms, saying they will “increase poverty rates”.

In an intervention likely to be seized on by MPs seeking to further water down the measures, the committee asks ministers for answers on 10 issues surrounding the benefit changes – and says the reforms risk “regression” for disabled people.

The committee, which reports to the Office of the High Commissioner for Human Rights, asks about British politicians suggesting people are defrauding the benefits system.

Chancellor Rachel Reeves and Prime Minister Sir Keir Starmer at the launch of the 10-year health plan in east London. Pic: PA

One point on which it wants clarification is: “Public statements by politicians and authorities portraying persons with disabilities as making profit of social benefits, making false statements to get social and disability benefits or being a burden to society.”

Other questions are on the impact the measures will have on “young persons, new claimants of disability benefits, women with disabilities, persons with disabilities with high level supports” and others.

They ask ministers about what measures they have taken to address “the foreseeable risk of increasing poverty rates amongst persons with disabilities if cuts are approved” and claim the welfare bill has had “limited scrutiny”.

The letter claims that the committee has “received credible information” that the Universal Credit and Personal Independent Payment Bill “will deepen the signs of regression” that the committee warned about in a report last year on the cost of living crisis and its impact on disabled people.

An intervention by the UN will be an embarrassment to the government, which has promised its welfare reforms will help disabled people into work.

Welfare bill blows ‘black hole’ in chancellor’s accounts

Liz Kendall, the welfare secretary, was criticised heavily earlier in the year for saying some people on benefits were “taking the mickey”.

After a chaotic first vote in Parliament on 1 July, in which MPs succeeded in watering down the reforms significantly, the government now says its reforms will lift 50,000 people out of poverty. The bill was backed by 335 MPs, with 260 against – a majority of 75.

Read more:

This has been PM’s most damaging U-turn yet

Is Starmer at the mercy of his MPs?

The first version of the reforms would have – the government’s assessment said – pushed 250,000 people into poverty.

Charities are urging MPs to continue to push for further changes – including on cuts to Universal Credit sickness payments.

Labour welfare rebel wants ‘respect’

A different UN committee heavily criticised benefit changes made by the Conservatives in 2016 and called on the UK to take “corrective measures” when Labour came into office.

The UN’s committee on Economic, Social and Cultural Rights (CESCR) concluded that “welfare reform” measures introduced by Conservative-led governments in 2012 and 2016 had disproportionately affected disabled people, low-income families, and workers in “precarious employment”.

The committee said this had led to “severe economic hardship, increased reliance on food banks, homelessness, negative impacts on mental health, and the stigmatisation of benefit claimants”.

The Department for Work and Pensions has been contacted for comment.

The Universal Credit and Personal Independent Payment Bill returns to the Commons on Wednesday for its remaining stages.

Mikey Erhardt, policy lead at Disability Rights UK, said: “The fact that the UN has yet again felt it needs to write to the UK government about our cruel and punitive social security system should be a national shame.

“We hope this letter is a wake-up call for MPs. Despite all the chaos of the last-minute climbdowns and concessions, the Universal Credit bill remains broken.

“There are still billions of cuts on the table, and we urge MPs to approach tomorrow’s proceedings with caution as their vote will have serious implications for disabled people across the country.

“If disabled people feel unable to trust the government’s promises on co-production and the UN needed to raise concerns over the bill’s impact, how can MPs vote this bill through?”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike