Spring statement: Rachel Reeves can make decisions on spending cuts without too much fallout for now – but worse could be yet to come

Rachel Reeves will keep her remarks short when she delivers the spring statement on Wednesday.

But the enormity of what she is saying will be lost on no one as the chancellor sets out the grim reality of the country’s finances.

Her economic update to the House of Commons will reveal a deteriorating economic outlook and rising borrowing costs, which has forced her to find spending cuts, which she’s left others to carry the can for (more on that in a bit).

Politics Live: Polling suggests almost everyone is pessimistic

The independent Office of Budget Responsibility (OBR) is expected to forecast that growth for 2025 has halved from 2% to 1%.

That, combined with rising debt repayment costs on government borrowing, has left the chancellor with a black hole in the public finances against the forecasts published at the budget in October.

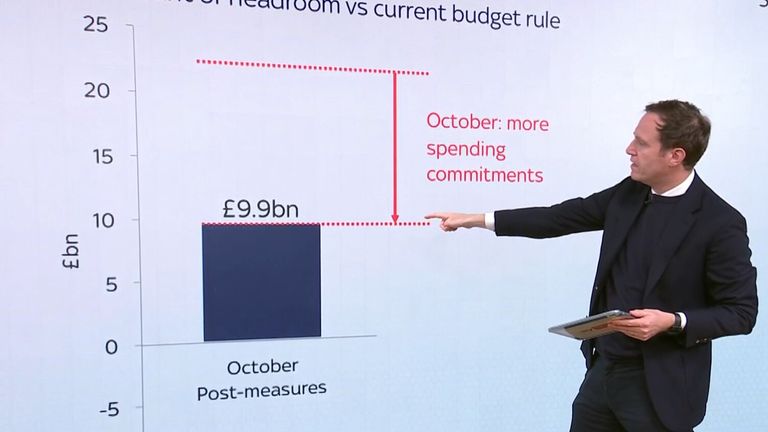

Back then, Reeves had a £9.9bn cushion against her “iron-clad” fiscal rule that day-to-day spending must be funded through tax receipts not debt by 2029-30.

But that surplus has been wiped out in the ensuing six months – now she finds herself about £4bn in the red, according to those familiar with the forecasts.

That’s really uncomfortable for a chancellor who just months ago executed the biggest tax and spend budget in a generation with the promise that she would get the economy growing again.

At the first progress check, she looks to be failing and has been forced into finding spending cuts to make up the shortfall after ruling out her other two options – further tax rises or more borrowing via a loosening of her self-imposed fiscal rules.

What to expect in the spring statement

‘World has changed’

When Reeves gets up on Wednesday, she will put it differently, saying the “world has changed” and all that means is the government must move “further and faster” to deliver the reforms that will drive growth.

But her opponents will be quick to lay economic woes at her door, arguing that the unexpected £25bn tax hike on employers’ national insurance contributions last October have choked off growth.

But it’s not just opposition from the Conservative benches that the chancellor is facing – it is opposition from within as she sets about cutting government spending to the tune of £15bn to fill that black hole.

Politically, her allies know how awkward it would have been for the chancellor to announce £5bn in welfare cuts to avoid breaking her own fiscal rules, with one acknowledging that those cuts had to be kept separate from the spring statement.

There’s also expected to be more than £5bn of extra cuts from public spending in the forecast period, which could see departments that don’t have protected budgets – education, justice, home – face real-term spending cuts by the end of the decade.

Pic: PA

Not an emergency budget

We won’t see the detail of that until the Spending Review in June.

This is not an emergency budget because the chancellor isn’t embarking on a round of tax raising to fix the public finances.

But these are, however they are framed, emergency spending cuts designed to plug her black hole and that is politically difficult for a government that has promised no return to austerity if some parts of the public sector face deep cuts to stick with fiscal rules.

If that’s the macro picture, what about the “everyday economics” of peoples’ lives?

I’d point out two things here. On Wednesday, we will get to see where those £5bn of welfare cuts will fall as the government publishes the impact assessment that it held back last week.

Read more:

Corbyn brands benefit cuts a ‘disgrace’

Expect different focus from Reeves at spring statement

Up to a million people could be affected by cuts, and the reality of who will be hit will pile on the pressure for Labour MPs already uncomfortable with cuts to health and disability benefits.

Benefits cuts explained

The second point is whether the government remains on course to deliver its key pledge to “put more money in the pockets of working people” during this parliament after the Joseph Rowntree Foundation think-tank produced analysis over the weekend saying living standards for all UK families are set to fall by 2030.

The chancellor told my colleague Trevor Phillips on Sunday that she “rejects” the analysis that the average family could be £1,400 worse off by 2030.

But that doesn’t mean that the forecasts published on Wednesday calculating real household disposable income per head won’t make for grim reading as the economic outlook deteriorates.

Nervousness in Labour

Ask around the party, and there is obvious nervousness about how this might land, with a degree of anxiety about the economic outlook and what that has in store for departmental budgets.

But there is recognition too from many MPs that the government has political space afforded by that whopping majority, to make these decisions on spending cuts without too much fallout – for now.

Because while Wednesday will be bad, worse could be yet to come.

Staring down the barrel

The chancellor is staring down the barrel of a possible global trade war that will only serve to create more economic uncertainty, even if the UK is spared from the worst tariffs by President Donald Trump.

The national insurance hike is also set to kick in next month, with employers across the piece sounding the warnings around investment, jobs and growth.

Six months ago, Reeves said she wouldn’t be coming back for more after she announced £40bn in tax rises in that massive first budget.

Six months on she is coming back for more, this time in the form of spending cuts. And in six months’ time, she may well have to come back for more in the form of tax rises or deeper cuts.

The spring statement was meant to be a run-of-the-mill economic update, but it has morphed into much more.

The chancellor now has the hard sell to make from a very hard place, that could soon become even tougher still.

As a milestone is reached of 50,000 migrants crossing the Channel since he became prime minister, Keir Starmer finds himself in a familiar place – seemingly unable to either stop the boats, or escape talking about them.

Home Office data shows 50,271 people made the journey since the election last July, after 474 migrants arrived on Monday. This is around 13,000 higher than the comparable period the previous year.

Politics Live: Starmer hits unwanted small boat crossings milestone

Starmer has tweeted more than 10 times about this issue in the past week alone, more than any other.

On Monday he wrote on X: “If you come to this country illegally, you will face detention and return. If you come to this country and commit a crime, we will deport you as soon as possible.”

It could be a tweet by a politician of any party on the right – and many voters (and Labour MPs) will say it’s right that the prime minister is taking this issue seriously.

Illegal – or irregular – migration is a relatively small proportion of total migration. Net migration was down at 431,000 in 2024 which the OCED say is comparable to other high-income countries. But it is of course highly visible and politically charged.

Nigel Farage’s Reform party have had a busy few months campaigning on it, and the prime minister has been toughening up his language in response.

Shortly after the local elections in May in which Reform won hundreds of seats and took control of councils, Starmer made his speech in which he warned: “In a diverse nation like ours, without fair immigration rules, we risk becoming an island of strangers.”

It outraged some in his own party, and he later said he regretted that language.

But it was part of a speech which made clear that he wanted action – vowing to end “years of uncontrolled migration” in a way “that will finally take back control of our borders and close the book on a squalid chapter for our politics.”

A group of people thought to be migrants are brought in to the Border Force compound in Dover, Kent. Pic: PA

It’s a long way from his early months as Labour leader in 2020 when he said: “We welcome migrants, we don’t scapegoat them.” Migration did not feature as one of his five missions for “change” at the general election.

The strategy by Starmer and his minister is to talk up forthcoming new measures – a crackdown on social media adverts by traffickers, returns of people without a right to be in the UK which are indeed higher than under the Conservatives, and last week, a “one in, one out” deal with France to send people back across the channel.

The government say some people have been detained, although it is not known when these returns will happen. Ministers are also still pointing the finger at the previous Conservative government – which found stopping the boats easy to say and hard to achieve.

Read More:

Kemi Badenoch suggests asylum seekers should be housed in ‘Nightingale’ camps

What is the UK-France migrant returns deal, who will be returned and how many?

Baroness Jacqui Smith, a former home secretary, said this morning: “I don’t think it was our fault that it was enabled to take root. We’ve taken our responsibility to work internationally, to change the law, to improve the way in which the asylum system works, to take through legislation to strengthen the powers that are available.

“The last government did none of those things and focused on gimmicks. And it’s because of that, that the crime behind this got embedded in the way which it did. And that won’t be solved overnight.”

But for a prime minister who appears to have come to this issue reluctantly, talking about it a lot – and suggesting he’ll be judged on whether he can tackle it – risks raising expectations.

Joe Twyman, of the pollsters Deltapoll said: “You cannot simply out-Farage Nigel Farage when it comes to the subject of immigration. In a sense, Labour is falling into precisely the same trap that the Conservatives fell into. They’re giving significant prominence to a subject where they don’t have much control”.

Starmer has avoided mentioning firm numbers on how many migrants his crackdown may stop, but as previous prime ministers have found with the difficult issue of controlling migration, if you ask to be judged on delivery, voters will do so.

AI systems are already ignoring shutdown commands. Decentralized audit trails are needed to prevent centralized AI from becoming humanity’s Skynet.

Stablecoin laws are popping up all over the globe, but their differences could spell trouble for cross-border crypto projects.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike