Trump hails ‘total reset’ with China as trade tariffs slashed

The US and China have agreed to slash trade tariffs on each other, a move Donald Trump has said was part of a “total reset” in relations.

The president said the 90-day truce followed “very friendly” talks between the two sides in Switzerland over the weekend and those discussions would continue..

“China was being hurt very badly. They were closing up factories they were having a lot of unrest and they were very happy to do something with us”, he told reporters at the White House.

The breakthrough was announced early on Monday – to the delight of fincial markets – by the leader of the US delegation, treasury secretary Scott Bessent.

US trade representative Jamieson Greer confirmed so-called reciprocal tariffs were now at 10% each.

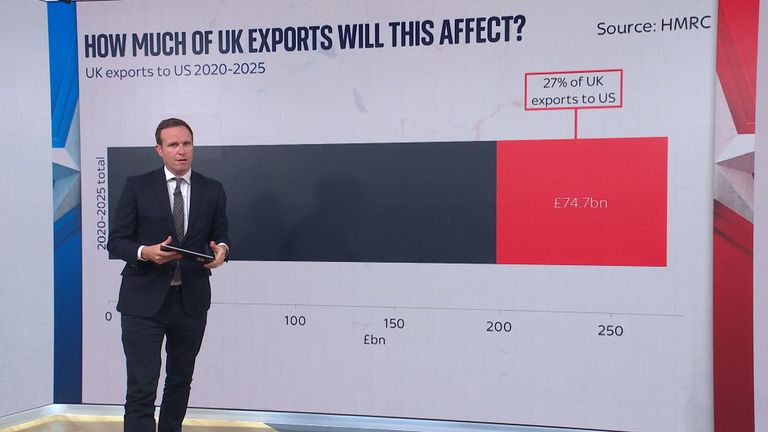

In real terms, it meant the US is reducing its 145% tariff to 30% on Chinese goods. A tariff of 20% had been implemented on China when President Donald Trump took office, over what his administration said was a failure to stop illegal drugs entering the US.

China has agreed to reduce its 125% retaliatory tariffs to 10% on US goods.

Sector-specific tariffs, such as the 25% tax on cars, aluminium and steel, remain in place.

Money blog: Life as a divorce lawyer

Tariffs, taxes on imports of more than 100%, had been imposed on both sides. China was the only country exempt from a 90-day pause on the “retaliatory” tariffs above the base 10% levies applied by America.

Major retailers had been warning Mr Trump of empty shelves as US importers pause shipments.

Mr Bessent said after a weekend of negotiations in Switzerland, the countries had a mechanism for continued talks.

It’s the second major trade announcement made by the US in the last week, after a deal was secured with the UK on Thursday.

The move signals a willingness from the Americans to make deals on tariffs.

Why Trump blinked in US-China trade war

Of all the fronts in Donald Trump’s trade war, none was as dramatic and economically threatening as the sky-high tariffs he imposed on China.

There are a couple of reasons: first, because China is and was the single biggest importer of goods into the US and, second, because of the sheer height of the tariffs imposed by the White House in recent months.

In short, tariffs of over 100% were tantamount to a total embargo on goods coming from the United States’ main trading partner.

That would have had enormous economic implications, not just for the US but every other country around the world (these are the world’s biggest and second-biggest economies, after all).

So the truce announced on Monday by treasury secretary Scott Bessent is undoubtedly a very big deal indeed.

Welcomed news

The news was received positively by Asian stock markets on Monday as major indexes were up.

In China, the Shanghai Composite stock index rose 0.8%, the Shenzhen Component gained 1.7%, and Hong Kong’s Hang Seng index was up nearly 3%.

In countries across Asia, benchmark stock indexes also rose. Korea’s Kospi grew 1.1%, Japan’s Nikkei was up 0.8%, while India’s Nifty 50 index of most valuable companies gained more than 3%.

US stocks rose sharply at the open.

The S&P 500 and tech-heavy Nasdaq saw their biggest leaps in more than a month, rising almost 3% and 4% respectively.

The market rally was visible in Europe too.

The dollar – hit in recent weeks by US recession speculation – was up more than a cent versus the pound while oil prices also rallied. Brent crude, the international benchmark, was 3.5% higher at $66 a barrel.

What next?

When asked by journalists about what the US wanted to see from China in the 90s, Mr Bessent said, “As long as there is good faith effort, engagement and constructive dialogue, then we will keep moving forward.”

Explained: The US-UK trade deal

The UK came to the front of the line for deals, Mr Bessent added, “as our oldest ally”.

Switzerland had also moved to the “front of the queue”, he said, while the EU has been slower.

As with the other counties subject to 90-day pauses, a permanent deal will need to be reached, but confidence across the world is likely to have been boosted.

Listen to The World with Richard Engel and Yalda Hakim every Wednesday

Businesses now need a clear timetable and roadmap for future negotiations under the newly announced economic and trade consultation mechanism, said Andrew Wilson, the deputy secretary general of the International Chamber of Commerce.

“The credibility of that process for resolving underlying frictions in the Sino-US economic relationship will be mission-critical in terms of restoring business confidence.”

The UK has come a “step closer” to having direct, high-speed rail connections to Germany, the Department for Transport has said.

A partnership between international train operator Eurostar and German national rail company Deutsche Bahn (DB) has “set the foundation” for a fast rail connection between Britain and Europe’s largest economy, the businesses announced on Thursday.

It means the companies are exploring options to offer direct services between London and Cologne and Frankfurt.

Money blog: Major airport increasing drop-off charge

Such direct services would mean reaching Cologne in four hours, and Frankfurt in less than five from the capital city.

At present, rail passengers have to change trains in Brussels to reach those cities. It takes at least five-and-a-half hours to reach Frankfurt, and four-and-a-quarter hours to arrive in Cologne.

Cologne Central Station could soon be served by trains from the UK. Pic: AP

The proposed services would use existing lines and infrastructure. Passengers would board a double-decker Eurostar in London, and be spared a change of trains on the continent.

The ambition to create such links had already been announced, as had a plan to allow direct rail travel from London to Geneva, but the partnership between DB and Eurostar had not.

Will it definitely happen?

Details and technicalities are yet to be worked out, with the German train company highlighting that any services are contingent upon “the necessary technical, operational, and legal prerequisites being met”.

“Implementation by individual railway companies is considered extremely difficult,” DB said.

“Joint partnerships are therefore crucial.”

What about Berlin?

Nothing was announced for a direct service to Berlin on Thursday, despite Transport Secretary Heidi Alexander singling out the benefits and prospect of journeys from London to the German capital in July.

“The Brandenburg Gate, the Berlin Wall and Checkpoint Charlie – in just a matter of years, rail passengers in the UK could be able to visit these iconic sights direct from the comfort of a train, thanks to a direct connection linking London and Berlin,” she said at the time.

A high-speed Eurostar train heading towards France. File pic: PA

Shorter journeys, like those to Frankfurt and Cologne, are seen as more commercially viable than the current 10-hour train journey time to Berlin.

Market studies conducted by Eurostar found travellers are comfortable with international rail journeys of up to six hours.

“Our research indicates that many would choose rail over air for trips within this timeframe,” Eurostar told Sky News. “This, combined with strong business and leisure demand on this route, is why we have prioritised London to Frankfurt.”

Read more from Sky News:

Petrofac administrators eye North Sea sale by Christmas

Submarine hunting pact signed by UK amid Russian threat

The Department for Transport said the focus on the two German cities was a commercial decision by Eurostar and DB, and the UK-Germany rail taskforce, established over the summer, could pave the way for further route announcements.

The energy regulator has confirmed plans for a massive upgrade to the UK’s energy grids, adding £108 to customer bills by 2031.

Ofgem said on Thursday that the £28bn investment over the next five years would bolster resilience in the transition to a renewable energy future and that much of the bill would be offset by increased efficiency.

It pointed to estimated savings for households of around £80 because of the planned investment in gas and power infrastructure, leaving a net additional contribution of £28.

Money latest: Is property still a good investment?

Ofgem said the £28bn sum formed part of an estimated £90bn to be invested in the energy networks by 2031, with “adaptive” funding arrangements helping to shield customers from volatility in the market.

Most of the funding announced on Thursday will go towards maintaining gas networks, which will remain a key source of energy as green power capacity is built up further.

“Investing now to maintain world-class resilience and expand grid capacity is the most cost-effective way to harness clean power, support economic growth and protect the country from gas price shocks like the one seen in 2022”, Ofgem said.

What’s driving energy prices higher?

Then, Russia’s invasion of Ukraine and Europe’s refusal to buy Russian gas in response, meant that energy bills hit unprecedented levels and gave birth to the wider cost-of-living crisis as higher energy costs were passed on across the economy.

Read more: Paying up front for energy future should lead to tangible savings

Ofgem made its announcement as costs of government energy policy and other upgrades make the biggest upwards contributions to household bills. However, the budget moved to take away some costs from April next year.

Ofgem boss Jonathan Brearley said: “The funding announced today will keep Britain’s energy network among the safest, most secure and resilient in the world. The investment will support the transition to new forms of energy and support new industrial customers to help drive economic growth and insulate us from volatile gas prices.

“But this is not investment at any price. Every pound must deliver value for consumers. Ofgem will hold network companies accountable for delivering on time and on budget, and we make no apologies for the efficiency challenge we’re setting as the industry scales up investment.

“We’ve built strong consumer protections into these contracts, meaning funds will only be released when needed and clawed back if not used. Households and businesses must get value for money, and we will ensure they do.”

‘It’s either keep warm or eat’

A Department for Energy Security and Net Zero spokesperson said: “This government is taking action to bring down energy bills for families, with the budget taking an average £150 of costs off bills in April, and expanding our £150 Warm Home Discount to over six million families.

“Upgrading our gas and electricity networks after years of underinvestment is essential to keep the lights on and ensure energy security for our country. Without these plans, which were first set out under the previous government, costs would spiral and our security would be compromised.

“The only way to bring down bills for good and get off the fossil fuel rollercoaster is with this government’s mission to deliver clean homegrown that we control.”

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024