Interest rate hikes ‘net positive’ for economy but not everyone

Here’s a sentence which might sound a little odd: higher interest rates have been good news for the UK economy.

For the first time in many decades, the pain faced by borrowers from higher interest rates has been more than balanced out by the benefit experienced by savers from those interest rates.

If this sounds a little odd it’s partly because invariably, when people – the media, politicians and economists – talk about interest rates they focus unduly on one side of the equation: the plight of the borrower. And there’s an understandable reason for that: in previous “hiking cycles”, when the Bank of England raises interest rates, that pain has invariably outweighed the windfall.

Money latest: Mortgage price war ‘likely’ as 3% interest rates predicted

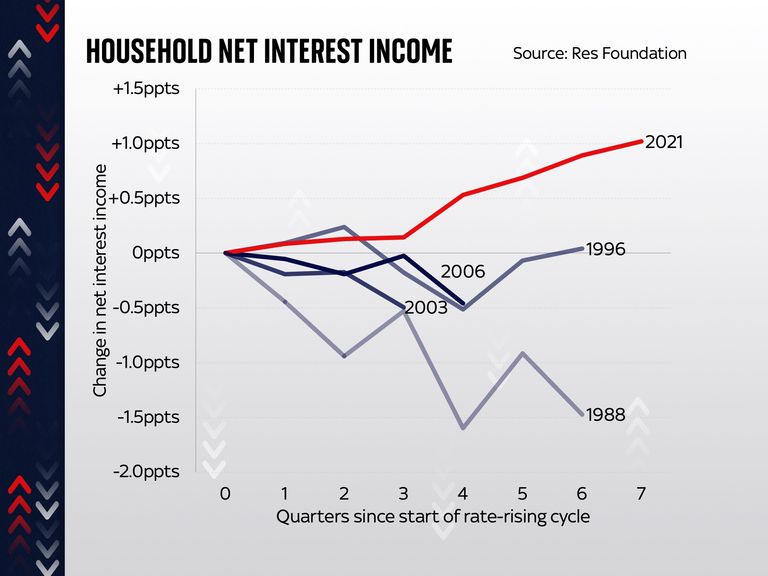

That was the case when borrowing rates were lifted in 1988; it was the case in 1996, in 2003 and in 2006.

In each case the overall impact, across the economy, on households’ balance sheets was negative.

But not so this time around.

According to the Resolution Foundation, the net income we’ve earned, across the economy, as a result of interest rates, has actually risen rather than fallen – up by a percentage point since rates started going up.

To put that into perspective, the “interest rate effect” on incomes in the late 1980s was -1.5 percentage points.

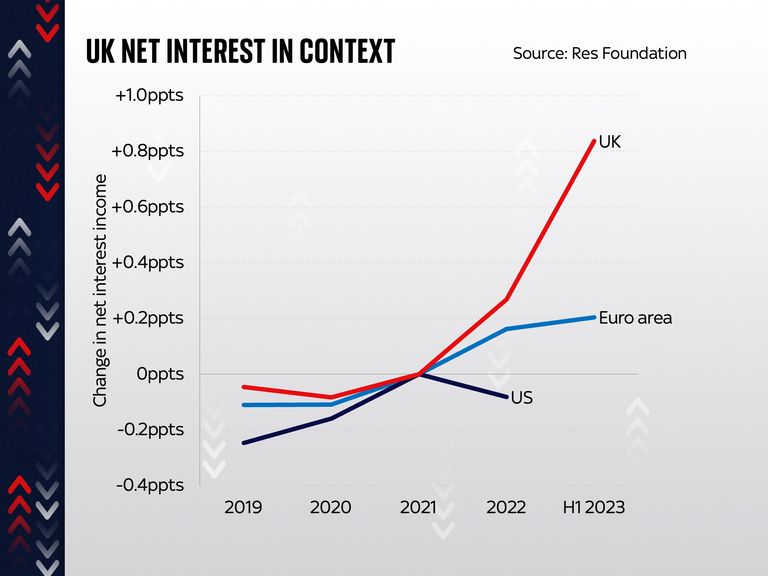

And what’s striking, when you compare the UK to the euro area and the US, is that we are a bit of an outlier: the interest rate effect, across the economy, was much more positive than it was in those two other areas.

This, says the Resolution Foundation, is at least part of the explanation for how the UK hasn’t yet slipped into the recession a lot of people anticipated this time last year.

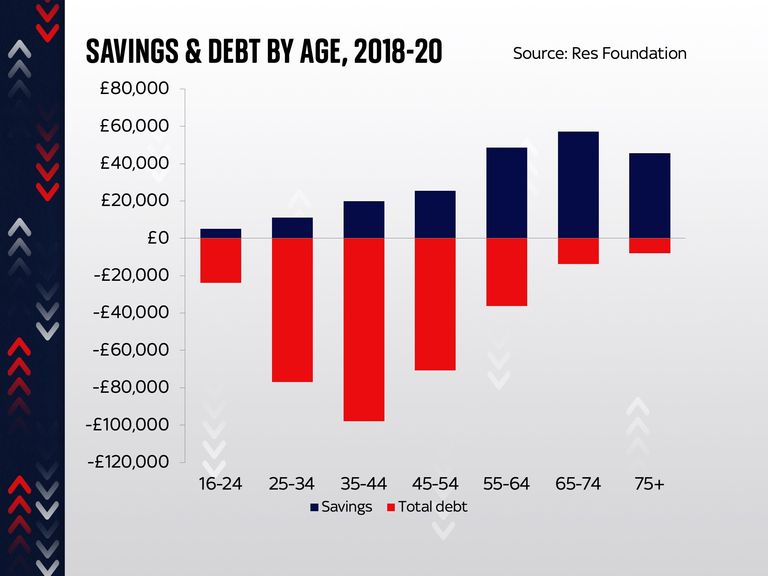

Part of the explanation for this is that it so happened, in large part because of the pandemic lockdowns, that people began this hiking cycle with a lot of savings in their bank accounts – far more than usual.

Read more:

Mortgage approvals up as more lenders cut rates

First-time buyers fall to ‘lowest level in a decade’

FTSE 100 bosses ‘earn typical UK annual salary in three days’

The upshot was that, across the economy, the benefit from those savings (and savings rates went up very quickly – albeit not to the levels of borrowing rates) was greater than the impact on mortgages and loans. Another part of the explanation is that so far only around half of those with fixed-rate mortgages have re-fixed their loans.

But there are a few very important provisos here. The first and perhaps most important is that while the above is certainly true across the whole economy, there’s a dramatic difference of experience for different categories of people.

Those whose debts outweigh their savings (which in this case mostly means younger people) will certainly see a negative impact from higher rates. Those with far more savings than debts – the older segments of the population – will see a benefit. In other words, the pain and the dividends are not being equally shared out. The old are doing much better; the young are doing worse.

And there are two other provisos. The first is that this positive impact will begin to wear off as more and more people re-fix their mortgages and go up from low-interest rates to higher rates. Even though the typical fixed-rate deal has been coming down recently, it’s still far higher than it was two or five years ago.

Click to subscribe to The Ian King Business Podcast wherever you get your podcasts

The final proviso is that none of the above takes into account the broader impact of the cost of living crisis.

Everyone is having to pay higher prices for nearly everything. And while the annual rate at which those prices are increasing (inflation) has decelerated, the level of prices remains more than 15% above where it was a couple of years ago.

That’s a painful adjustment for everyone. The good news is that the impact of rates – across the economy as a whole – has actually been positive rather than negative. But not everyone will be seeing the benefits.

Talk to economists and they will tell you that the cost of living crisis is over.

They will point towards charts showing that while inflation is still above the Bank of England’s 2% target, it has come down considerably in recent years, and is now “only” hovering between 3% and 4%.

So why does the cost of living still feel like such a pressing issue for so many households? The short answer is because, depending on how you define it, it never ended.

Economists like to focus on the change in prices over the past year, and certainly on that measure inflation is down sharply, from double-digit levels in recent years.

But if you look over the past four years then the rate of change is at its highest since the early 1990s.

But even that understates the complexity of economic circumstances facing households around the country.

For if you want a sense of how current financial conditions really feel in people’s pockets, you really ought to offset inflation against wages, and then also take account of the impact of taxes.

That is a complex exercise – in part because no two households’ experience is alike.

But recent research from the Resolution Foundation illustrates some of the dynamics going on beneath the surface, and underlines that for many households the cost of living crisis is still very real indeed.

UK inflation slows to 3.4%

The place to begin here is to recall that perhaps the best measure of economic “feelgood factor” is to subtract inflation and taxes from people’s nominal pay.

You end up with a statistic showing your real household disposable income.

Consider the projected pattern over the coming years. For a household earning £50,000, earnings are expected to increase by 10% between 2024/25 and 2027/28.

Subtract inflation projected over that period and all of a sudden that 10% drops to 2.5%.

Now subtract the real increase in payments of National Insurance and taxes and it’s down to 0.2%.

Now subtract projected council tax increases and all of a sudden what began as a 10% increase is actually a 0.1% decrease.

Read more:

UK economy figures ‘not as bad as they look’, analysts say

More options than ever for savers to beat inflation

Will we see tax rises in next budget?

Of course, the degree of change in your circumstances can differ depending on all sorts of factors. Some earners (especially those close to tax thresholds, which in this case includes those on £50,000) feel the impact of tax changes more than others.

Pensioners and those who own their homes outright benefit from a comparatively lower increase in housing costs in the coming years than those paying mortgages and (especially) rent.

Nor is everyone’s experience of inflation the same. In general, lower-income households pay considerably more of their earnings on essentials, like housing costs, food and energy. Some of those costs are going up rapidly – indeed, the UK faces higher power costs than any other developed economy.

But the ultimate verdict provides some clear patterns. Pensioners can expect further increases in their take-home pay in the coming years. Those who own their homes outright and with mortgages can likely expect earnings to outpace extra costs. But others are less fortunate. Those who rent their homes privately are projected to see sharp falls in their household income – and children are likely to see further falls in their economic welfare too.

The UK economy unexpectedly shrank in May, even after the worst of Donald Trump’s tariffs were paused, official figures showed.

A standard measure of economic growth, gross domestic product (GDP), contracted 0.1% in May, according to the Office for National Statistics (ONS).

Rather than a fall being anticipated, growth of 0.1% was forecast by economists polled by Reuters as big falls in production and construction were seen.

It followed a 0.3% contraction in April, when Mr Trump announced his country-specific tariffs and sparked a global trade war.

A 90-day pause on these import taxes, which has been extended, allowed more normality to resume.

This was borne out by other figures released by the ONS on Friday.

Exports to the United States rose £300m but “remained relatively low” following a “substantial decrease” in April, the data said.

Overall, there was a “large rise in goods imports and a fall in goods exports”.

A ‘disappointing’ but mixed picture

It’s “disappointing” news, Chancellor Rachel Reeves said. She and the government as a whole have repeatedly said growing the economy was their number one priority.

“I am determined to kickstart economic growth and deliver on that promise”, she added.

But the picture was not all bad.

Growth recorded in March was revised upwards, further indicating that companies invested to prepare for tariffs. Rather than GDP of 0.2%, the ONS said on Friday the figure was actually 0.4%.

It showed businesses moved forward activity to be ready for the extra taxes. Businesses were hit with higher employer national insurance contributions in April.

Read more:

Trump plans to hit Canada with 35% tariff – warning of blanket hike for other countries

Woman and three teenagers arrested over M&S, Co-op and Harrods cyber attacks

The expansion in March means the economy still grew when the three months are looked at together.

While an interest rate cut in August had already been expected, investors upped their bets of a 0.25 percentage point fall in the Bank of England’s base interest rate.

Such a cut would bring down the rate to 4% and make borrowing cheaper.

Is Britain going bankrupt?

Analysts from economic research firm Pantheon Macro said the data was not as bad as it looked.

“The size of the manufacturing drop looks erratic to us and should partly unwind… There are signs that GDP growth can rebound in June”, said Pantheon’s chief UK economist, Rob Wood.

Why did the economy shrink?

The drops in manufacturing came mostly due to slowed car-making, less oil and gas extraction and the pharmaceutical industry.

The fall was not larger because the services industry – the largest part of the economy – expanded, with law firms and computer programmers having a good month.

It made up for a “very weak” month for retailers, the ONS said.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike