Jeremy Hunt says ‘I don’t yet know’ if govt can cut taxes again before election after National Insurance reduction

Chancellor Jeremy Hunt is unsure if the government can afford further tax cuts – as a National Insurance (NI) reduction comes into force today.

The pre-election cut to NI, from 12% to 10%, will impact around 27 million payroll employees across the UK.

A person earning the UK’s average salary of £35,000 will save £450 a year, or £37.38 a month, as a result of this change.

Money latest:

See how much your pay will change

Mr Hunt said the reduction, announced in his Autumn Statement last year, means “that a typical family with two earners will be nearly a thousand pounds better off this year”.

But Labour argued this wasn’t true, saying frozen income tax and national insurance thresholds mean that many families have been drawn into higher tax bands.

The Opposition’s new attack ads criticising the policy even made it onto the Tory-supporting website Conservative Home on Friday.

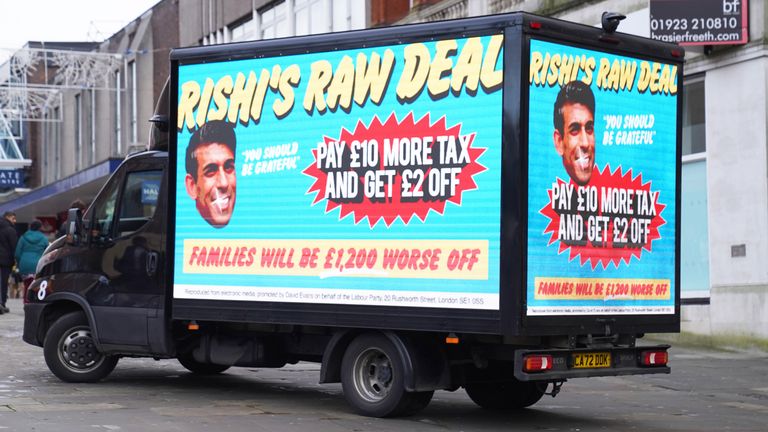

Shadow chancellor Rachel Reeves said: “Under Rishi Sunak’s raw deal, for every extra £10 people are paying in tax they are only getting £2 back.”

Labour attack ad

‘If I can afford to go further I will’

In a statement on Saturday, Mr Hunt said he wanted to further ease the tax burden, which is expected to rise to the highest level since the Second World War before the end of this decade, but he doesn’t yet know if he can.

He called the NI reduction “the start of a process”, adding: “If I can afford to go further I will… I don’t yet know if I can.

“We want to do this because it helps families, it also helps to grow the economy, and we believe that a lightly taxed economy will grow faster and in the end that’ll mean more money for public services like the NHS.”

Mr Hunt argued the Conservative government “wants to bring down taxes” and recognises that “families are finding life really tough”.

But he defended its previous measures, saying: “It was right to support families through COVID and through the cost of living crisis, and yes taxes had to go up in that period.”

The government says its NI reduction is the biggest tax cut on record for workers.

The chancellor added: “Even after the effect of the tax rises that have happened previously, this means that a typical family will see their taxes go down next year.”

Jeremy Hunt leaves Downing Street to deliver the autumn statement in the Commons

Will Hunt cut taxes again before election?

The clock is ticking for Mr Hunt to find the fiscal headroom to cut taxes again.

The spring budget, pencilled in for 6 March, will be the last chance for him to make major tax and spending promises before the election, which Mr Sunak has said will likely be in the second half of the year.

Following the Autumn Statement in November, the government has faced pressure from Tory MPs to go further and cut income tax or inheritance tax.

While many campaigners welcomed the National Insurance changes, they pointed out that the tax burden remains at record high levels for Britons – thanks in part to the threshold at which people start paying personal taxes being frozen, rather than rising with inflation.

Mr Sunak introduced the current tax freezes when he was chancellor back in 2021 and as prime minister, extended the time they would need to be in place, from 2026 to 2028.

This causes a so-called “fiscal drag” as pay goes up but tax thresholds don’t, so more people are dragged into higher tax brackets.

The Institute for Fiscal Studies has said the Autumn Statement gave back just £1 in tax cuts for every £4 of tax rises due to threshold freezes since 2021.

Ms Reeves claimed that despite the NI cut, the average family was paying £1,200 extra tax this year “because of choices by Rishi Sunak and this Conservative government”.

“Never have people paid so much in tax and got so little in return in the form of public services,” she said.

Read more:

A delay in calling the election is the last thing Starmer needs

What 2024 could have in store for UK politics

However, the Labour leadership has not committed to cutting tax or unfreezing the thresholds if they win the election.

Sir Keir Starmer told Sky News his priority is to grow the economy and he won’t make promises he can’t keep – but that he does want to “lower the burden of working people”.

The US Nasdaq stock exchange is making SEC approval of its proposal to offer tokenized versions of stocks listed on the exchange a top priority, according to the exchange’s crypto chief.

“We’ll just move as fast as we can,” Nasdaq’s head of digital assets strategy, Matt Savarese, said during an interview with CNBC on Thursday, when asked whether the SEC could approve the proposal this year.

“I think what we have to really evaluate where the public comments come back in and then answer and respond to the SEC questions as they come through,” Savarese said. “We hope to kind of work with them as quickly as possible,” Savarese said.

Savarese says Nasdaq isn’t “upending the system”

The proposal, submitted by Nasdaq on Sept. 8, is requesting to allow investors to buy and sell stock tokens — digital representations of shares in publicly traded companies — on the exchange.

Savarese emphasized that Nasdaq is not trying to overhaul the way stocks are invested in when asked whether he expects other major exchanges to follow suit.

“We’re not looking at upending the system; we want everyone to come along for that ride and bring tokenization more into the mainstream,” he said.

“We want to do it in that responsible investor-led way first, under the SEC rules themselves,” he added.

It was only in October that Robinhood CEO Vlad Tenev said that tokenization will “eventually eat the whole financial system.”

The crypto industry is divided on tokenized equities

Savarese emphasized that Nasdaq is aiming to be an innovator in the ecosystem, noting that the exchange was the first to transition markets from paper-based trading to electronic systems.

Related: DATs bring crypto’s insider trading problem to TradFi: Shane Molidor

Tokenizing stocks has been one of the most significant talking points in the crypto industry this year.

On Sept. 3, Galaxy Digital CEO Mike Novogratz said the company became the first Nasdaq-listed company to tokenize its equity on a major blockchain following its launch on the Solana network.

The conversation around tokenized equities has also drawn skepticism from the crypto industry.

On Oct. 1, Rob Hadick, general partner at crypto venture firm Dragonfly, told Cointelegraph that tokenized equities will be a significant benefit to traditional markets, but may not be a boon to the crypto industry as others have predicted.

Hadick said that if tokenized stocks use layer-2 networks, it creates “leakage” as value and may not flow back to Ethereum or the broader crypto ecosystem as much as hoped.

Magazine: When privacy and AML laws conflict: Crypto projects’ impossible choice

Hester Peirce, a commissioner of the United States Securities and Exchange Commission (SEC) and head of the SEC’s Crypto Task Force, reaffirmed the right to crypto self-custody and privacy in financial transactions.

“I’m a freedom maximalist,” Peirce told The Rollup podcast on Friday, while saying that self-custody of assets is a fundamental human right. She added:

“Why should I have to be forced to go through someone else to hold my assets? It baffles me that in this country, which is so premised on freedom, that would even be an issue — of course, people can hold their own assets.”

Peirce added that online financial privacy should be the standard. “It has become the presumption that if you want to keep your transactions private, you’re doing something wrong, but it should be exactly the opposite presumption,” she said.

The comments came as the Digital Asset Market Structure Clarity Act, a crypto market structure bill that includes provisions for self-custody, anti-money laundering(AML) regulations, and asset taxonomy, is delayed until 2026, according to Senator Tim Scott.

Related: SEC to hold privacy and financial surveillance roundtable in December

Exchange-traded funds (ETFs) challenge Bitcoin’s self-custody ethos

Many large Bitcoin (BTC) whales and long-term holders are pivoting from self-custody to ETFs to reap the tax benefits and hassle-free management of owning crypto in an investment vehicle.

“We are witnessing the first decline in self-custodied Bitcoin in 15 years,” Dr. Martin Hiesboeck, the head of research at crypto exchange Uphold, said.

Hiesboeck attributed the shift to the SEC approving in-kind creations and redemptions for crypto ETFs in July, which allowed authorized holders to exchange crypto for ETF shares and vice versa without triggering a taxable event, unlike cash-settled ETFs.

“A move away from the self-custody mantra of ‘not your keys, not your coins’ is another nail in the coffin of the original crypto spirit,” Hiesboeck added.

In February, notable Bitcoin analyst and investor PlanB, the developer of the BTC stock-to-flow model, announced that he transferred his Bitcoin to ETFs to alleviate the “hassle” of private key management.

PlanB’s announcement caused an outcry in the Bitcoin community, as many voiced concerns that handing over custody to a third party clashed with Bitcoin’s core values.

Magazine: When privacy and AML laws conflict: Crypto projects’ impossible choice

Jeremy Corbyn has declined to say his Your Party co-founder Zarah Sultana is a friend as supporters of the new grouping gather in Liverpool.

Speaking to Sky News on the eve of the conference, Mr Corbyn acknowledged “stresses and strains” in the set-up of the party but said it had become “a lot better in the last few days and weeks and we’re going to get through this weekend”.

The former Labour leader has publicly clashed with Ms Sultana, the MP for Coventry South, over the launch and structure of the new party.

Asked if they were friends, Mr Corbyn said they were “colleagues in parliament, and we obviously communicate and so on”.

The pair appeared at separate events on the eve of the party’s inaugural gathering.

Ms Sultana had previously claimed she was being “sidelined” by a “sexist boys’ club” within the fledgling party.

Mr Corbyn said her comments were an “unfortunate choice of words” but added that he had been more involved in the organisation of the conference than she had.

The co-founders have had a strained relationship since setting up the party. Pic: Your Party

The Islington North MP also said that Your Party was still waiting for Ms Sultana to transfer all of the funds she had raised from supporters.

“Obviously having money up front for a conference is a big help,” he said.

Ms Sultana has insisted she is transferring the donations in stages.

The weekend gathering in Liverpool will see supporters choose between four options for a permanent party name: Your Party, Our Party, Popular Alliance, For the Many.

The preferred choice of Ms Sultana – The Left – did not make the ballot.

Similarly, the Coventry MP had said she favoured a co-leader approach, but members will only be able to pick between single leadership or collective leadership models.

Speaking at her own pre-conference rally, Ms Sultana blamed a “nameless, faceless bureaucrat” for restricting the choices.

Read more from Sky News:

Reeves accused of deliberately making UK finances look worse

Famous names affected by prostate cancer criticise screening decision

The meeting also risked being disrupted by a series of member expulsions. One of those ejected, Lewis Nielsen, accused a “clique” of trying to “take over”.

Your Party sources said expulsions related to members of the Socialist Workers Party and that holding another national party membership was not allowed.

Ms Sultana blamed a “culture of paranoia at the top” and said she believed the same people who had been briefing against her were now also expelling members.

Mr Corbyn will open the conference on Saturday, while the results of the main decision-making votes will be announced on Sunday.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024