Woolworths demise 15 years on: What happened at the retail giant and could it come back?

Parachuted in to turn around a failing giant of the British high street, Robert McDonald was part of Woolworths’s last roll of the dice.

The new finance director said he was excited to join an “iconic” brand when he began work in early November 2008, but just three weeks later the company would sink into administration.

And there was little the company’s last ever executive hire could do to stop the famous store – known for its pick ‘n’ mix, homeware and everything in between – from closing for good on 6 January 2009.

“Like everyone my age, I had grown up thinking its existence was a normal part of life,” Mr McDonald told Sky News.

“I was very pleased to have the opportunity to work there. I knew it was going through hard times and looked forward to being able to help.

“But, sadly, it was past that by the time I joined, and the end seemed very swift.”

Analysts blame its downfall on a toxic combination of low cash reserves, lost credit insurance and crippling debt – all exacerbated by the 2008 financial crisis.

It marked the end of Woolies’s near century-long presence on the high street, with more than 800 stores closed down and about 27,000 jobs lost.

Woolworths was popular for its pic ‘n’ mix

For many of its staff, news of Woolworths’s demise into administration came from the media, with earlier rumours confirmed in reports on 26 November 2008.

Paul Seaton, who had worked as a store manager and as part of the IT team during 25 years at the company, said his colleagues “crowded around the TV” to hear their worst fears confirmed.

“It just all fell to pieces after that,” Mr Seaton, now 61, told Sky News.

“The sad reality is Woolworths took 99 years to build, and it took 42 days from administration to the day the last door shut. 99 years of meticulous care and thought… gone.”

The board insisted administration wouldn’t detract from “business as usual”, Mr Seaton said, but that all changed when he was called to a meeting on 5 December.

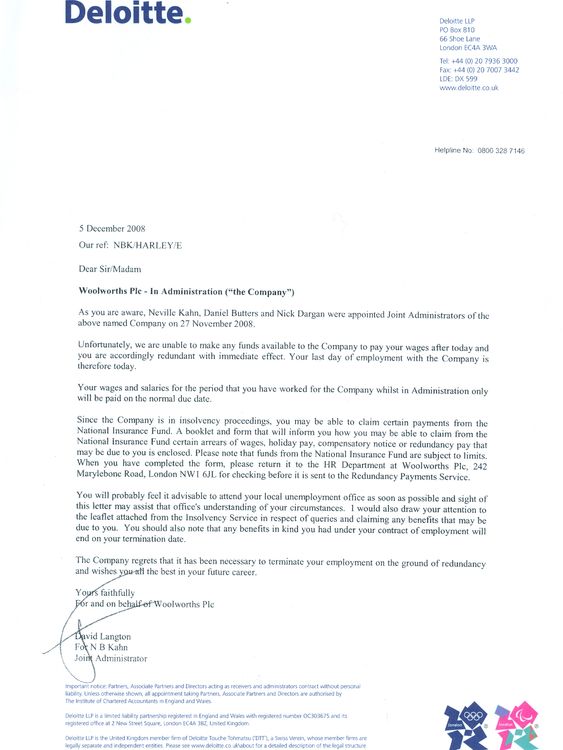

He was among 500 senior figures gathered at Woolworths HQ, where each was given a letter written by administrators Deloitte notifying none would be paid another day and all had lost their jobs with immediate effect.

The notice given by Deloitte to Paul Seaton

“We were summoned and told not to come back, all 500 of us,” Mr Seaton said, adding their passes into the building were deactivated on the spot. “The business only carried on for one month after that.”

While his time at the company came to an abrupt end, he dedicated time to creating a virtual Woolworths museum, preserving memorabilia and documenting the chain’s long history.

A store for the family

The first store opened in November 1909 in Liverpool, by New Yorker Frank Woolworth, who had already established the brand in the US.

In a prescient diary entry, he wrote during an earlier trip to Europe that “a good penny and sixpence store, run by a live Yankee, would be a sensation here”.

Such was the success of the UK counterpart, his successor Byron Miller reportedly beamed that “the child has long since outgrown the parent”.

Mr Seaton thinks the literal child-parent relationship was key to the store’s popularity.

“There used to be old adage that people need Tesco because everyone has to eat, and people trust Boots because you call the manager ‘doctor’, but they went to Woolworths because they love Woolworths,” he said.

“Have you ever heard a kid saying ‘mum I want to go to Tesco’? The whole reason I loved being a manager is kids and families loved coming to Woolworths.”

Paul Seaton with Woolworths memorabilia collected over the years

The store’s name lives on in Australia – though has no connection with US or UK equivalents – where it is the country’s largest supermarket chain and last year recorded a net profit of $1.62bn (about £87bn).

US stores closed in 1997, but the UK branches recorded a record profit topping £100m just one year later.

What went wrong?

Customers were still shopping at the UK stores, and in the firm’s final annual report the company made a slight pre-tax profit in 2007.

But even with some signs of recovery ahead of 2008, Woolworths had a terminal problem: modest cash flow and a £385m mountain of debt.

Retail expert Clare Bailey was among the consultants drafted in 2006 to tackle the mammoth task of detangling the company’s supply chain, which she says was collecting too much of some stock and too little of others.

As banks began to lose faith in Woolworths’s finances, the firm had its credit insurance withdrawn – meaning it had to pay suppliers immediately, rather than in instalments.

To make matters worse, many Woolworths stores were sold a few years before and rented back at a price that only appeared to increase over the years.

Left with fewer assets, little in way of cash reserves and no credit insurance, the retailer was not prepared for the coming shock of the 2008 financial crisis.

“Cashflow is like oxygen,” Ms Bailey told Sky News. “You can be profitable, but if you haven’t got cash to pay bills or for when something goes wrong, then that’s it – game over.”

The company reported a pre-tax loss of £90.8m over the first half of 2008 in September that year, despite launching the WorthIt range – promoting low-cost products – in 2007.

Losing sales and customers

One of the big issues Ms Bailey identified in the supply chain was a failure to keep evergreen products on shelves.

For example, she said only 20 stores out of more than 800 nationwide had the correct amount of coat hangers, a product that sells all year, while others bought far too many Christmas trees.

It meant money was “trapped in stocks”, she said, and would gradually turn customers away.

“And if you replicate that through other products, customers could find what they didn’t want, but not what they wanted,” she said.

“You might, as a customer, give them the benefit of the doubt a few times, but eventually they will turn to other places. So, they not only lost the sale – they also lost the customers.”

It’s this perceived neglect of the customer journey that small business growth expert Claire Hancott believes cost Woolworths at the turn of the century.

Footfall almost halved from 7.5 million in 2000 to around 4.5 million in 2007, she said, while the market for Woolworths’s once-popular CDs was shrinking as more consumers headed to the internet.

“Businesses can’t ignore these big trends, even if they won’t come into play for years,” Ms Hancott told Sky News.

“Blockbusters was a classic example, when they thought digital films wouldn’t take off.

“Woolworths wasn’t at the forefront of consumer technology and it’s so important to be looking 10, 20 years into the future – it takes a long time to prepare.”

Discount stores such as pound shops began to pop up on the high street, adding to growing competition that ultimately forced an attempt to sell the company in November 2008 for – ironically – just £1.

It was hoped a sale to restructuring experts Hilco would give them the job of repaying the debt, but the banks rejected the move.

The company went into administration just days later.

A false dawn, but will the sun rise on Woolworths again?

Ever since the company collapsed under the weight of its debt, rumours of a potential return to the high street have never been completely quashed.

A fake announcement – made by a social media account falsely claiming to be run by Woolworths – heralding a comeback was met with excitement in 2020, with savings platform Raisin UK reporting 44% of people discussing the store’s revival online “loved the news”.

The post turned out to be false

In August 2022, pollsters at YouGov found 49% of survey respondents said they wished they could bring back Woolies – a far higher proportion than any other defunct chain.

But for all the hopes of an encore, some of those involved with the firm rue the time that has since been lost – and believe it may have even survived.

“I came in at the end of 2006, but the work we were doing can take three or five years,” Ms Bailey said. “Maybe they started too late.”

All but a small handful of the Woolworths stores were re-let to other retailers within a decade, she added, meaning the spaces “still had merit in the local community”.

“The inner workings of a business are quite complicated,” she said.

“But I think it’s a sad situation it collapsed, because – had they been given a stay of execution – they may well have been successful in turning it around.”

Read more:

Christmas tree from 1920s Woolworths sells for ‘astonishing’ price

Next raises profit forecast but warns stock could be delayed by Red Sea attacks

Ms Hancott agrees: “In another time, would it have crumbled? That’s the million-pound question that nobody will be able to answer.

“Had it not been in the midst of a crisis, then it may have survived.”

For Mr McDonald, a chance to draw on his experience handling company finances never materialised.

It was, nonetheless, a “fascinating experience”, he said.

“It’s such a shame we didn’t have longer to turn that business around,” he said.

“I joined as part of a turnaround plan, but it was too late to change the course of history.”

The rate of inflation has risen by more than expected on the back of fuel and food price pressures, according to official figures which have prompted accusations of an own goal for the chancellor.

The Office for National Statistics (ONS) reported a 3.6% level for the 12 months to June – a pace not seen since January last year.

That was up from the 3.4% rate seen the previous month. Economists had expected no change.

Money latest: What do inflation figures mean for rate cut prospects?

ONS acting chief economist Richard Heys said: “Inflation ticked up in June driven mainly by motor fuel prices which fell only slightly, compared with a much larger decrease at this time last year.

“Food price inflation has increased for the third consecutive month to its highest annual rate since February of last year. However, it remains well below the peak seen in early 2023.”

A key driver of food inflation has been meat prices.

Beef, in particular, has shot up in cost – by more than 30% over the past year – according to Association of Independent Meat Suppliers data reported by FarmingUK.

Beef has seen the biggest percentage increase in meat costs. Pic: PA

High global demand alongside raised production costs have been blamed.

But Kris Hamer, director of insight at the British Retail Consortium, said: “While inflation has risen steadily over the last year, food inflation has seen a much more pronounced increase.

“Despite fierce competition between retailers, the ongoing impact of the last budget and poor harvests caused by the extreme weather have resulted in prices for consumers rising.”

It marked a clear claim that tax rises imposed on employers by Rachel Reeves from April have helped stoke inflation.

Balwinder Dhoot, director of sustainability and growth at the Food and Drink Federation, said: “The pressure on food and drink manufacturers continues to build. With many key ingredients like chocolate, butter, coffee, beef, and lamb, climbing in price – alongside high energy and labour expenses – these rising costs are gradually making their way into the prices shoppers pay at the tills.”

Chancellor Rachel Reeves said of the data: “I know working people are still struggling with the cost of living. That is why we have already taken action by increasing the national minimum wage for three million workers, rolling out free breakfast clubs in every primary school and extending the £3 bus fare cap.

“But there is more to do and I’m determined we deliver on our Plan for Change to put more money into people’s pockets.”

The wider ONS data is a timely reminder of the squeeze on living standards still being felt by many households – largely since the end of the COVID pandemic and subsequent energy-driven cost of living crisis.

Record rental costs alongside elevated borrowing costs – the latter a result of the Bank of England’s action to help keep a lid on inflation – have added to the burden on family budgets.

Is the cost of living crisis over?

Most are still reeling from the effects of high energy bills.

The cost of gas and electricity is among the reasons why the pace of price growth for many goods and services remains above a level the Bank would ideally like to see.

Added to that is the toll placed on finances by wider hikes to bills. April saw those for water, council tax and many other essentials rise at an inflation-busting rate.

The inflation figures, along with employment data due tomorrow, are the last before the Bank of England is due to make its next interest rate decision on 7 August.

The vast majority of financial market participants, and many economists, expect a quarter point cut to 4%.

That forecast is largely based on the fact that wider economic data is suggesting a slowdown in both economic growth and the labour market – twin headaches for a chancellor gunning for growth and juggling hugely squeezed public finances.

Read more from Sky News:

Chancellor considering ‘changes’ to ISAs

Most important part of Reeves’s speech was what wasn’t said

HMRC doesn’t know how many billionaires pay tax in the UK

Professor Joe Nellis, economic adviser at the advisory firm MHA, said of the ONS data: “This is a reminder that while price rises have slowed from the highs of 2021-23, the battle against inflation is far from over and there is no return to normality yet – especially for many households who are still feeling the squeeze on essentials such as food, energy, and services.

“However, while the Bank of England is expected to take a cautious approach to interest rate policy, we still expect a cut in interest rates when the Monetary Policy Committee next votes on 7th August.

“Despite inflation at 3.6% remaining above the official 2% target, a softening labour market – slowing wage growth and decreasing job vacancies – means that the MPC will predict inflation to begin falling as we head into the new year, justifying the lowering of interest rates.”

Business

Chancellor Rachel Reeves considering ‘changes’ to ISAs – and says there’s too much focus on ‘risk’ in investing

The chancellor has confirmed she is considering “changes” to ISAs – and said there has been too much focus on “risk” in members of the public investing.

In her second annual Mansion House speech to the financial sector, Rachel Reeves said she recognised “differing views” over the popular tax-free savings accounts, in which savers can currently put up to £20,000 a year.

She was reportedly considering reducing the threshold to as low as £4,000 a year, in a bid to encourage people to put money into stocks and shares instead and boost the economy.

However the chancellor has shelved any immediate planned changes after fierce backlash from building societies and consumer groups.

In her speech to key industry figures on Tuesday evening, Ms Reeves said: “I will continue to consider further changes to ISAs, engaging widely over the coming months and recognising that despite the differing views on the right approach, we are united in wanting better outcomes for both savers and for the UK economy.”

She added: “For too long, we have presented investment in too negative a light, quick to warn people of the risks, without giving proper weight to the benefits.”

Rachel Reeves’s fiscal dilemma

Ms Reeves’s speech, the first major one since the welfare bill climbdown two weeks ago, appeared to encourage regulators to focus less on risks and more on the benefits of investing in things like the stock market and government bonds (loans issued by states to raise funds with an interest rate paid in return).

She welcomed action by the financial regulator to review risk warning rules and the campaign to promote retail investment, which the Financial Conduct Authority (FCA) is launching next year.

“Our tangled system of financial advice and guidance has meant that people cannot get the right support to make decisions for themselves”, Ms Reeves told the event in London.

Read more:

Should you get Lifetime ISA? Two key issues to consider

Building societies protest against proposed ISA reforms

Is there £15bn of wiggle room in Reeves’s fiscal rules?

Last year, Ms Reeves said post-financial crash regulation had “gone too far” and set a course for cutting red tape.

On Tuesday, she said she would announce a package of City changes, including a new competitive framework for a part of the insurance industry and a regulatory regime for asset management.

Reeves is ‘totally’ up for the job

In response to Ms Reeves’s address, shadow chancellor Sir Mel Stride said: “Rachel Reeves should have used her speech this evening to rule out massive tax rises on businesses and working people. The fact that she didn’t should send a shiver down the spine of taxpayers across the country.”

👉Listen to Politics at Sam and Anne’s on your podcast app👈

The governor of the Bank of England, Andrew Bailey, also spoke at the Mansion House event and said Donald Trump’s taxes on US imports would slow the economy and trade imbalances should be addressed.

“Increasing tariffs creates the risk of fragmenting the world economy, and thereby reducing activity”, he said.

The taxpayer is to help drive the switch to non-polluting vehicles through a new grant of up to £3,750, but some of the cheapest electric cars are to be excluded.

The Department for Transport (DfT) said a £650m fund was being made available for the Electric Car Grant, which is due to get into gear from Wednesday.

Users of the scheme – the first of its kind since the last Conservative government scrapped grants for new electric vehicles three years ago – will be able to secure discounts based on the “sustainability” of the car.

Money latest: easyJet bereavement policy faces refund question

It will apply only to vehicles with a list price of £37,000 or below – with only the greenest models eligible for the highest grant.

Buyers of so-called ‘Band two’ vehicles can receive up to £1,500.

The qualification criteria includes a recognition of a vehicle’s carbon footprint from manufacture to showroom so UK-produced EVs, costing less than £37,000, would be expected to qualify for the top grant.

It is understood that Chinese-produced EVs – often the cheapest in the market – would not.

BYD electric vehicles before being loaded onto a ship in Lianyungang, China. Pic: Reuters

DfT said 33 new electric car models were currently available for less than £30,000.

The government has been encouraged to act as sales of new electric vehicles are struggling to keep pace with what is needed to meet emissions targets.

Challenges include the high prices for electric cars when compared to conventionally powered models.

At the same time, consumer and business budgets have been squeezed since the 2022 cost of living crisis – and households and businesses are continuing to feel the pinch to this day.

Another key concern is the state of the public charging network.

The Chinese electric car rivalling Tesla

Transport Secretary Heidi Alexander said: “This EV grant will not only allow people to keep more of their hard-earned money – it’ll help our automotive sector seize one of the biggest opportunities of the 21st century.

“And with over 82,000 public charge points now available across the UK, we’ve built the infrastructure families need to make the switch with confidence.”

The Government has pledged to ban the sale of new fully petrol or diesel cars and vans from 2030 but has allowed non-plug in hybrid sales to continue until 2025.

It is hoped the grants will enable the industry to meet and even exceed the current zero emission vehicle mandate.

Under the rules, at least 28% of new cars sold by each manufacturer in the UK this year must be zero emission.

The figure stood at 21.6% during the first half of the year.

The car industry has long complained that it has had to foot a multi-billion pound bill to woo buyers for electric cars through “unsustainable” discounting.

Mike Hawes, chief executive of the Society of Motor Manufacturers and Traders, said the grants sent a “clear signal to consumers that now is the time to switch”.

He went on: “Rapid deployment and availability of this grant over the next few years will help provide the momentum that is essential to take the EV market from just one in four today, to four in five by the end of the decade.”

But the Conservatives questioned whether taxpayers should be footing the bill.

Shadow transport secretary Gareth Bacon said: “Last week, the Office for Budget Responsibility made clear the transition to EVs comes at a cost, and this scheme only adds to it.

“Make no mistake: more tax rises are coming in the autumn.”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike