Brexit border controls coming into effect today will force up price of food and flowers

Food and fresh flower imports from the European Union are subject to new Brexit customs controls from today, adding more than £300m a year to the price of trading with the continent and forcing up the price of food for British consumers.

Under the new Brexit red tape, imports of chilled and frozen meat and fish, cheese and dairy products, and five common varieties of cut flowers will require an export health certificate, signed off by a European vet or plant inspector, before they can enter the UK.

From 30 April the same categories of goods will face physical inspections at the border, raising the prospect of delays and shortages in fast turnaround supply chains.

New Brexit rules impacting flowers

The new rules come four years after similar checks were imposed on UK exporters to Europe, and have already been delayed five times because of concerns about disruption and increasing costs to consumers.

The government says the checks are required to protect UK biosecurity and prevent pests and diseases from being imported, and level the playing field for UK exporters.

Its own estimates say the cost of trading with Europe will increase by £330m a year however, and increase food inflation, a key driver of the cost of living crisis, by 0.2% over the next three years.

Goods from Ireland will be subject to controls for the first time but those coming from Northern Ireland will not. Despite being part of the European Customs Union, they are subject to lighter controls under the Windsor Framework, due to be revised as part of a deal to restore power-sharing at Stormont.

Business groups in the UK and Europe have raised concerns about the costs and disruption likely to flow as a consequence.

The UK imports around half of its pork from the EU and the industry says the new rules, particularly physical checks planned for April, are impractical and should be reviewed.

Read more:

UK £311bn worse off by 2035 due to leaving EU, report says

UK car production industry warns of looming Brexit rules ‘threat’

‘We should sit down with the EU’

Peter Hardwick of the British Meat Processors’ Association told Sky News: “This is absolutely anathema to the current government but we should sit down with the European Union, negotiate a comprehensive veterinary agreement based on alignment. That would wipe away this problem overnight.

“It would remove all the costs, and would also significantly resolve the issues in relation to goods moving to Northern Ireland. I know that’s a difficult thing politically but that’s what we believe should be done.”

Disruption is expected to be minimal in the early stages as checks will be restricted to random online paperwork inspections, and officials say they will be pragmatic to avoid delays.

Baroness Lucy Neville-Rolfe, minister of state at the Cabinet Office, said: “Our aim is to have border controls which maximise the protection of the UK population from harms such as drugs and animal and human diseases while minimising the disruption to legitimate trade.

“The new UK system being introduced over the course of this year makes a huge stride towards meeting this objective. We have worked with traders and businesses extensively to design the controls and will continue to listen to their feedback.”

Some of the world’s leading tech companies are betting big on very small innovations.

Last week, Samsung released its Galaxy Z Fold 7 which – when open – has a thickness of just 4.2mm, one of the slimmest folding phones ever to hit the market.

And Honor, a spin-off from Chinese smartphone company Huawei, will soon ship its latest foldable – the slimmest in the world. Its new Honor Magic V5 model is only 8.8mm thick when folded, and a mere 4.1mm when open.

Apple is also expected to release a foldable in the second half of next year, according to a note by analysts at JPMorgan published this week.

The race to miniaturise technology is speeding up, the ultimate prize being the next evolution in consumer devices.

Whether it be wearable devices, such as smartglasses, watches, rings or foldables – there is enormous market potential for any manufacturer that can make its products small enough.

Despite being thinner than its predecessor, Honor claims its Magic V5 also offers significant improvements to battery life, processing power, and camera capabilities.

Hope Cao, a product expert at Honor told Sky News the progress was “due largely to our silicon carbon battery technology”. These batteries are a next-generation breakthrough that offers higher energy density compared to traditional lithium-ion batteries, and are becoming more common in consumer devices.

The Magic V5. Pic: Honor

Honor also told Sky News it had used its own AI model “to precisely test and find the optimum design, which was both the slimmest, as well as, the most durable.”

However, research and development into miniaturisation goes well beyond just folding phones.

A company that’s been at the forefront of developing augmented reality (AR) glasses, Xreal, was one of the first to release a viable pair to the consumer market.

Xreal’s Ralph Jodice told Sky News “one of our biggest engineering challenges is shrinking powerful augmented reality technology into a form factor that looks and feels like everyday sunglasses”.

Xreal’s specs can display images on the lenses like something out of a sci-fi movie – allowing the wearer to connect most USB-C compatible devices such as phones, laptops and handheld consoles to an IMAX-sized screen anywhere they go.

Pic: Xreal

Experts at The Metaverse Society suggest prices of these wearable devices could be lowered by shifting the burden of computing from the headset to a mobile phone or computer, whose battery and processor would power the glasses via a cable.

However, despite the daunting challenge, companies are doubling down on research and making leaps in the area.

Social media giant Meta is also vying for dominance in the miniature market.

Ray-Ban Meta AI glasses are shown off at the annual British Educational Training and Technology conference. Pic: PA

Meta’s Ray-Ban sunglasses (to which they recently added an Oakley range), cannot project images on the lenses like the pair from Xreal – instead they can capture photos, footage and sound. When connected to a smartphone they can even use your phone’s 5G connection to ask Meta’s AI what you’re looking at, and ask how to save a particular type of houseplant for example.

Gareth Sutcliffe, a tech and media analyst at Enders Analysis, tells Sky News wearables “are a green field opportunity for Meta and Google” to capture a market of “hundreds of millions of users if these devices sell at similar rates to mobile phones”.

Li-Chen Miller, Meta’s vice president of product and wearables, recently said: “You’d be hard-pressed to find a more interesting engineering problem in the company than the one that’s at the intersection of these two dynamics, building glasses [with onboard technology] that people are comfortable wearing on their faces for extended periods of time … and willing to wear them around friends, family, and others nearby.”

Mr Sutcliffe points out that “Meta’s R&D spend on wearables looks extraordinary in the context of limited sales now, but should the category explode in popularity, it will be seen as a great strategic bet.”

Facebook founder Mark Zuckerberg’s long-term aim is to combine the abilities of both Xreal and the Ray-Bans into a fully functioning pair of smartglasses, capable of capturing content, as well as display graphics onscreen.

However, despite recently showcasing a prototype model, the company was at pains to point out that it was still far from ready for the consumer market.

This race is a marathon not a sprint – or as Sutcliffe tells Sky News “a decade-long slog” – but 17 years after the release of the first iPhone, people are beginning to wonder what will replace it – and it could well be a pair of glasses.

Business

US trade war: The state of play as Trump signs order imposing new tariffs – but there are more delays

Donald Trump’s trade war has been difficult to keep up with, to put it mildly.

For all the threats and bluster of the US election campaign last year to the on-off implementation of trade tariffs – and more threats – since he returned to the White House in January, the president‘s protectionist agenda has been haphazard.

Trading partners, export-focused firms, customs agents and even his own trade team have had a lot on their plates as deadlines were imposed – and then retracted – and the tariff numbers tinkered.

Money latest: Why your internet feels slower

While the UK was the first country to secure a truce of sorts, described as a “deal”, the vast majority of nations have failed to secure any agreement.

Deal or no deal, no country is on better trading terms with the United States than it was when Trump 2.0 began.

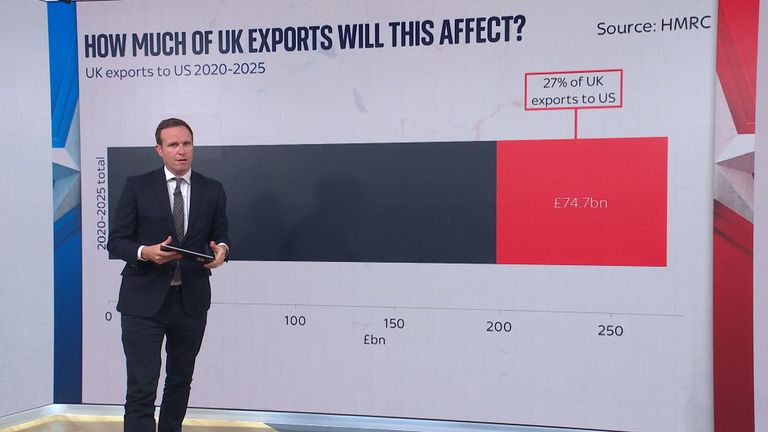

Here, we examine what nations and blocs are on the hook for, and the potential consequences, as Mr Trump’s suspended “reciprocal” tariffs prepare to take effect. That will now not happen until 7 August.

What does the UK-US trade deal involve?

Why was 1 August such an important date?

To understand the present day, we must first wind the clock back to early April.

Then, Mr Trump proudly showed off a board in the White House Rose Garden containing a list of countries and the tariffs they would immediately face in retaliation for the rates they impose on US-made goods. He called it “liberation day”.

The tariff numbers were big and financial markets took fright.

Just days later, the president announced a 90-day pause in those rates for all countries except China, to allow for negotiations.

The initial deadline of 9 July was then extended again to 1 August. Late on 31 July, Mr Trump signed the executive order but said that the tariff rates would not kick in for seven additional days to allow for the orders to be fully communicated.

Since April, only eight countries or trading blocs have agreed “deals” to limit the reciprocal tariffs and – in some cases – sectoral tariffs already in place.

Who has agreed a deal over the past 120 days?

The UK, Japan, Indonesia, the European Union and South Korea are among the eight to be facing lower rates than had been threatened back in April.

China has not really done a deal but it is no longer facing punitive tariffs above 100%.

Its decision to retaliate against US levies prompted a truce level to be agreed between the pair, pending further talks.

There’s a backlash against the EU over its deal, with many national leaders accusing the European Commission of giving in too easily. A broad 15% rate is to apply, down from the threatened 30%, while the bloc has also committed to US investment and to pay for US-produced natural gas.

Millions of EU jobs were in firing line

Where does the UK stand?

We’ve already mentioned that the UK was the first to avert the worst of what was threatened.

While a 10% baseline tariff covers the vast majority of the goods we send to the US, aerospace products are exempt.

Our steel sector has not been subjected to Trump’s 50% tariffs and has been facing down a 25% rate. The government announced on Thursday that it would not apply under the terms of a quota system.

UK car exports were on a 25% rate until the end of June when the deal agreed in May took that down to 10% under a similar quota arrangement that exempts the first 100,000 cars from a levy.

Who has not done a deal?

Canada is among the big names facing a 35% baseline tariff rate. That is up from 25% and covers all goods not subject to a US-Mexico-Canada trade agreement that involves rules of origin.

America is its biggest export market and it has long been in Trump’s sights.

Mexico, another country deeply ingrained in the US supply chain, is facing a 30% rate but has been given an extra 90 days to secure a deal.

Brazil is facing a 50% rate. For India, it’s 25%.

What are the consequences?

This is where it all gets a bit woolly – for good reasons.

The trade war is unprecedented in scale, given the global nature of modern business.

It takes time for official statistics to catch up, especially when tariff rates chop and change so much.

Any duties on exports to the United States are a threat to company sales and economic growth alike – in both the US and the rest of the world. Many carmakers, for example, have refused to offer guidance on their outlooks for revenue and profits.

Apple warned on Thursday night that US tariffs would add $1.1bn of costs in the three months to September alone.

Barriers to business are never good but the International Monetary Fund earlier this week raised its forecast for global economic growth this year from 2.8% to 3%.

Some of that increase can be explained by the deals involving major economies, including Japan, the EU and UK.

US growth figures have been skewed by the rush to beat import tariffs.

Read more:

Trump signs executive order for reciprocal tariffs

Aston Martin outlines plan to ease US tariff hit

The big risk ahead?

It’s a self-inflicted wound.

The elephant in the room is inflation. Countries imposing duties on their imports force the recipient of those goods to foot the additional bill. Do the buyers swallow it or pass it on?

The latest US data contained strong evidence that tariff charges were now making their way down the country’s supply chains, threatening to squeeze American consumers in the months ahead.

It’s why the US central bank has been refusing demands from Mr Trump to cut interest rates. You don’t slow the pace of price rises by making borrowing costs cheaper.

A prolonged period of higher inflation would not go down well with US businesses or voters. It’s why financial markets have followed a recent trend known as TACO, helping stock markets remain at record levels.

The belief is that Trump always chickens out. He may have to back down if inflation takes off.

It is “Liberation Day” III – the third tariff deadline set by Donald Trump.

Countries without bilateral trade agreements will soon face reciprocal tariffs – ranging from 25% to 50% – with a baseline of 15% to 20% for any not making a deal.

He has delayed twice, from April to July and from July to August, but hammered this date home in his trademark caps-on style: “THE AUGUST FIRST DEADLINE STANDS STRONG, AND WILL NOT BE EXTENDED. A BIG DAY FOR AMERICA!!!”

“Will not be extended” for anyone but Mexico, it seems. The country secured a 90-day extension at the last minute, with Mr Trump citing the “complexities” of the border.

Explained: The US-UK trade deal

By close of business on the eve of deadline, he had a handful of framework deals – some significant – including the UK (10%), the EU, Japan and South Korea (15%), Indonesia and the Philippines (19%), Vietnam (20%).

On the EU agreement, which he struck in Scotland, the president said: “It’s a very powerful deal, it’s a big deal, it’s the biggest of all the deals.”

But what happened to the “90 deals in 90 days” touted by the White House earlier this year?

The short answer is they were replaced by letters of instruction to pay a tariff set by the US.

How Trump 2.0 changed the world

Amid of flurry of late activity, the US played hardball with major trading partners like Canada.

“For the rest of the world, we’re going to have things done by Friday,” said US Commerce Secretary Howard Lutnick – the “rest of the world” meaning everyone but China.

There is, apparently, the “framework of a deal” between the world’s two largest economies, but talks between Washington and Beijing are continuing.

Read more US news:

Top Trump officials to visit Gaza

Heavy rain and flash floods batter east coast

Worker begs America for help

In terms of wins, he can claim some significant deals and point to his tariffs having generated an impressive $27bn (£20.4bn) in June, not bad for a single month.

But the legality of the approach is under siege – with the US Court of International Trade ruling that the “Liberation Day” tariffs exceeded the president’s authority, with enforcement paused pending appeal.

The deadline has stirred the pot, forcing a handful of deals onto the table. Whether they stick or survive legal scrutiny is far from settled.

But the playbook remains the same – threaten the world with trade chaos, whittle it down, celebrate the wins, and pray no one checks what’s legal.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike