Rate of inflation eases to 3.4% in February, official figures show

The rate of inflation slowed sharply to an annual rate of 3.4% in February, according to official figures charting a big contribution from food costs.

Data from the Office for National Statistics (ONS) showed an easing in the headline measure from the 4% rate recorded the previous month to a level last seen almost two-and-a-half years ago.

It was led, the report said, by food prices being almost flat this year compared with a large rise last year, while restaurant and café price rises also slowed.

Money latest: Reaction as UK inflation eases by more than expected

“These falls were only partially offset by price rises at the [fuel] pump and a further increase in rental costs,” ONS chief economist Grant Fitzner said.

The data marks further progress in the battle against energy-led price growth that followed Russia’s war in Ukraine and inflation is forecast to fall back below the Bank of England‘s target rate of 2% in the next few months.

However, the Bank’s interest rate-setting committee is widely expected to hold off on removing the medicine it has dished out to tackle inflation, possibly until the summer.

Its latest rate decision is due on Thursday.

Will the UK come out of recession?

Interest rate cuts would provide relief to millions of borrowers who have faced hefty increases to their costs as a consequence of higher interest rates.

But committee members are wary of starting the process as it’s feared inflation may tick back up in the second half of the year.

While there was some comfort in the latest data from core inflation figures, which strip out volatile elements such as food and energy costs, they are waiting for visibility on many price pressures including the pace of wage growth, disruption to shipping in the Red Sea and rising global oil costs.

Regular pay rises, according to separate ONS data last week, were still running above 6% – a level that could help drive demand in the flatlining economy and force up the pace of price increases.

Brent crude oil costs hit levels not seen since October last year earlier this week at $87 per barrel.

Interest rate cuts would help put more money back in people’s pockets over time, boosting the economy which officially entered recession in the second half of last year.

The economy is predicted to be the main battleground in the looming election so the timing of such action, by the politically neutral Bank, could be crucial.

‘I’m frustrated, I want an election’

London Stock Exchange Group (LSEG) data suggests the market expects the first cut to come in June but there is a growing school of thought that inflation may remain stickier than expected by that time, leaving August more in the frame.

Chancellor Jeremy Hunt said of the inflation data: “The plan is working. Inflation has not just fallen decisively but is forecast to hit the 2% target within months.

“This sets the scene for better economic conditions which could allow further progress on our ambition to boost growth and make work pay by bringing down national insurance as we work towards abolishing the double tax on work – but only if we can do so without increasing borrowing or cutting funding for public services.”

Rachel Reeves, Labour’s shadow chancellor, responded: “After fourteen years of chaos and uncertainty under the Conservatives working people are worse off. Prices are still high, the tax burden is the highest it has been in seventy years and mortgage payments are going up.

“Now Rishi Sunak is putting forward a reckless £46bn unfunded tax plan to abolish National Insurance that would risk crashing the economy and re-running the disastrous Liz Truss experiment.

“Britain cannot afford another five years of this failed Conservative government. It’s time for change and it’s time for Rishi Sunak to set the date for the election.”

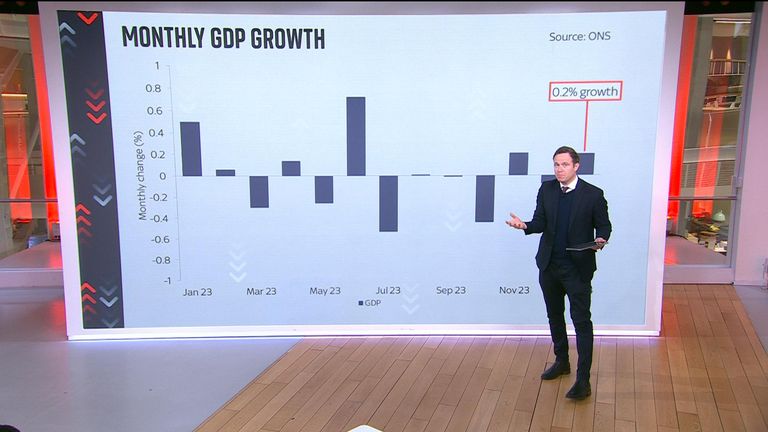

The UK economy unexpectedly shrank in May, even after the worst of Donald Trump’s tariffs were paused, official figures showed.

A standard measure of economic growth, gross domestic product (GDP), contracted 0.1% in May, according to the Office for National Statistics (ONS).

Rather than a fall being anticipated, growth of 0.1% was forecast by economists polled by Reuters as big falls in production and construction were seen.

It followed a 0.3% contraction in April, when Mr Trump announced his country-specific tariffs and sparked a global trade war.

A 90-day pause on these import taxes, which has been extended, allowed more normality to resume.

This was borne out by other figures released by the ONS on Friday.

Exports to the United States rose £300m but “remained relatively low” following a “substantial decrease” in April, the data said.

Overall, there was a “large rise in goods imports and a fall in goods exports”.

A ‘disappointing’ but mixed picture

It’s “disappointing” news, Chancellor Rachel Reeves said. She and the government as a whole have repeatedly said growing the economy was their number one priority.

“I am determined to kickstart economic growth and deliver on that promise”, she added.

But the picture was not all bad.

Growth recorded in March was revised upwards, further indicating that companies invested to prepare for tariffs. Rather than GDP of 0.2%, the ONS said on Friday the figure was actually 0.4%.

It showed businesses moved forward activity to be ready for the extra taxes. Businesses were hit with higher employer national insurance contributions in April.

Read more:

Trump plans to hit Canada with 35% tariff – warning of blanket hike for other countries

Woman and three teenagers arrested over M&S, Co-op and Harrods cyber attacks

The expansion in March means the economy still grew when the three months are looked at together.

While an interest rate cut in August had already been expected, investors upped their bets of a 0.25 percentage point fall in the Bank of England’s base interest rate.

Such a cut would bring down the rate to 4% and make borrowing cheaper.

Is Britain going bankrupt?

Analysts from economic research firm Pantheon Macro said the data was not as bad as it looked.

“The size of the manufacturing drop looks erratic to us and should partly unwind… There are signs that GDP growth can rebound in June”, said Pantheon’s chief UK economist, Rob Wood.

Why did the economy shrink?

The drops in manufacturing came mostly due to slowed car-making, less oil and gas extraction and the pharmaceutical industry.

The fall was not larger because the services industry – the largest part of the economy – expanded, with law firms and computer programmers having a good month.

It made up for a “very weak” month for retailers, the ONS said.

Monthly Gross Domestic Product (GDP) figures are volatile and, on their own, don’t tell us much.

However, the picture emerging a year since the election of the Labour government is not hugely comforting.

This is a government that promised to turbocharge economic growth, the key to improving livelihoods and the public finances. Instead, the economy is mainly flatlining.

Output shrank in May by 0.1%. That followed a 0.3% drop in April.

Ministers were celebrating a few months ago as data showed the economy grew by 0.7% in the first quarter.

Hangover from artificial growth

However, the subsequent data has shown us that much of that growth was artificial, with businesses racing to get orders out of the door to beat the possible introduction of tariffs. Property transactions were also brought forward to beat stamp duty changes.

Read more:

Trump to hit Canada with 35% tariff

Woman and three teens arrested over cyber attacks

In April, we experienced the hangover as orders and industrial output dropped. Services also struggled as demand for legal and conveyancing services dropped after the stamp duty changes.

Many of those distortions have now been smoothed out, but the manufacturing sector still struggled in May.

Signs of recovery

Manufacturing output fell by 1% in May, but more up-to-date data suggests the sector is recovering.

“We expect both cars and pharma output to improve as the UK-US trade deal comes into force and the volatility unwinds,” economists at Pantheon Macroeconomics said.

Meanwhile, the services sector eked out growth of 0.1%.

A 2.7% month-to-month fall in retail sales suppressed growth in the sector, but that should improve with hot weather likely to boost demand at restaurants and pubs.

Struggles ahead

It is unlikely, however, to massively shift the dial for the economy, the kind of shift the Labour government has promised and needs in order to give it some breathing room against its fiscal rules.

The economy remains fragile, and there are risks and traps lurking around the corner.

Is Britain going bankrupt?

Concerns that the chancellor, Rachel Reeves, is considering tax hikes could weigh on consumer confidence, at a time when businesses are already scaling back hiring because of national insurance tax hikes.

Inflation is also expected to climb in the second half of the year, further weighing on consumers and businesses.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike