Klarna scores major payment deal with Uber ahead of hotly anticipated IPO

The Swedish “buy now, pay later” pioneer said Tuesday that its new design would help users find the items they want by using more advanced AI recommendation algorithms, while merchants will be able to target customers more effectively.

Rafael Henrique | SOPA Images | LightRocket via Getty Images

Klarna on Wednesday announced a global partnership with Uber to power payments for the ride-hailing giant’s Uber and Uber Eats apps.

The partnership will see the Swedish financial technology firm added as a payment option in the U.S., Germany, and Sweden, Klarna said in a statement.

In the U.S., Germany, and Sweden, Klarna will roll out its “Pay Now” option, which lets customers pay off an order instantly in one click, in the Uber and Uber Eats apps. Users will be able to track all their Uber purchases in the Klarna app.

The company will also offer an additional payment option for Uber users in Sweden and Germany which allows users to bundle purchases into a single, interest-free payment that gets taken out of their monthly salary.

Interestingly, the company isn’t rolling out installment-based buy now, pay later plans, arguably its most popular service offering, on Uber’s platforms — only immediate payments and monthly payments.

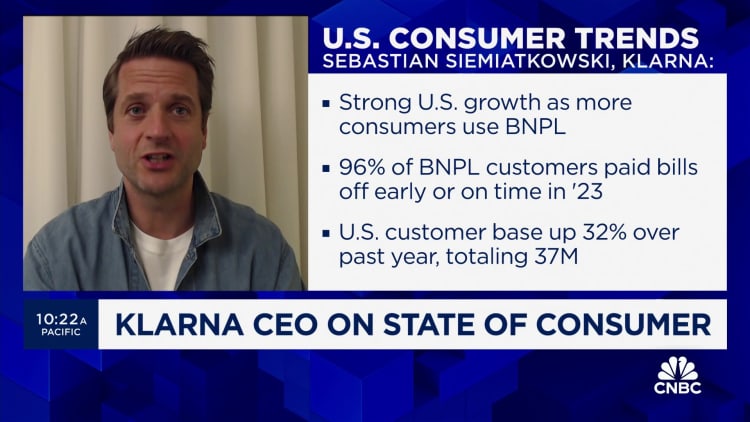

Sebastian Siemiatkowski, CEO and Co-Founder of Klarna, said in a statement Wednesday that the deal represented a “significant milestone” for the company.

“Consumers can Pay Now quickly and securely in full, which already accounts for over one third of Klarna’s global volumes, and more easily manage their finances in one place,” Siemiatkowski said.

Klarna declined to disclose financial terms of its deal with Uber.

Big pre-IPO merchant win

The Uber deal marks one of the most significant merchant wins for Klarna of late, and comes as the European fintech giant is rumored to be gearing up for a blockbuster initial public offering that could value the firm at north of $20 billion.

Klarna began having detailed discussions with investment banks to work on an IPO that could happen as early as the third quarter, Bloomberg News reported in February, citing unnamed sources familiar with the matter.

CNBC could not independently verify the accuracy of the report. Klarna has said that it doesn’t comment on market speculation.

Such a market flotation would mark something of a turnaround for a company that saw $38.9 billion erased from its valuation in 2022, when deteriorating macroeconomic conditions stoked by Russia’s invasion of Ukraine caused a reset of sky-high tech valuations.

Klarna reached an eye-watering $45.6 billion in a 2021 funding round led by SoftBank, before seeing its market value fall to $6.7 billion the following year in a so-called “down round.”

The firm recently launched a monthly subscription plan in the U.S. to lock in “power users” ahead of its anticipated IPO.

The product, called Klarna Plus, costs $7.99 per month, and enables users get their service fees waived, earn double rewards points and access curated discounts from partners including Nike and Instacart.

Last year, Klarna reported its first quarterly profit in four years after cutting its credit losses by 56%.

The company posted operating profit of 130 million Swedish krona in the third quarter of 2023, swinging to a profit for a loss of 2 billion Swedish krona in the same period a year earlier.

Buy now, pay later boom

Klarna is one of many “buy now, pay later” services that allow users to pay off their purchases over a period of monthly installments.

The payment method has become increasingly popular among consumers to pay for online and in-person shopping purchases, as an alternative to credit cards which charge interest and high fees.

However, it has also stoked concerns about the affordability of such services, and whether it is in fact encouraging some consumers — particularly younger people — to spend more than they can afford.

In the U.K., the government has proposed draft laws for regulating the buy now, pay later industry.

The U.S. Consumer Financial Protection Bureau has said previously it plans to subject buy now, pay later lenders to the same oversight as credit card companies.

Meanwhile, the European Union last year passed a revised version of its Consumer Credit Directive to include buy now, pay later services under the scope of the rules.

For its part, Klarna has defended the buy now, pay later model, arguing it offers customers a cheaper way of accessing credit in comparison to traditional credit cards and consumer loans.

The company also says it welcomes regulation of buy now, pay later products.

Chief executive officer of Google Sundar Pichai.

Marek Antoni Iwanczuk | Sopa Images | Lightrocket | Getty Images

Google on Friday made the latest a splash in the AI talent wars, announcing an agreement to bring in Varun Mohan, co-founder and CEO of artificial intelligence coding startup Windsurf.

As part of the deal, Google will also hire other senior Windsurf research and development employees. Google is not investing in Windsurf, but the search giant will take a nonexclusive license to certain Windsurf technology, according to a person familiar with the matter. Windsurf remains free to license its technology to others.

“We’re excited to welcome some top AI coding talent from Windsurf’s team to Google DeepMind to advance our work in agentic coding,” a Google spokesperson wrote in an email. “We’re excited to continue bringing the benefits of Gemini to software developers everywhere.”

The deal between Google and Windsurf comes after the AI coding startup had been in talks with OpenAI for a $3 billion acquisition deal, CNBC reported in April. OpenAI did not immediately respond to a request for comment.

The move ratchets up the talent war in AI particularly among prominent companies. Meta has made lucrative job offers to several employees at OpenAI in recent weeks. Most notably, the Facebook parent added Scale AI founder Alexandr Wang to lead its AI strategy as part of a $14.3 billion investment into his startup.

Douglas Chen, another Windsurf co-founder, will be among those joining Google in the deal, Jeff Wang, the startup’s new interim CEO and its head of business for the past two years, wrote in a post on X.

“Most of Windsurf’s world-class team will continue to build the Windsurf product with the goal of maximizing its impact in the enterprise,” Wang wrote.

Windsurf has become more popular this year as an option for so-called vibe coding, which is the process of using new age AI tools to write code. Developers and non-developers have embraced the concept, leading to more revenue for Windsurf and competitors, such as Cursor, which OpenAI also looked at buying. All the interest has led investors to assign higher valuations to the startups.

This isn’t the first time Google has hired select people out of a startup. It did the same with Character.AI last summer. Amazon and Microsoft have also absorbed AI talent in this fashion, with the Adept and Inflection deals, respectively.

Microsoft is pushing an agent mode in its Visual Studio Code editor for vibe coding. In April, Microsoft CEO Satya Nadella said AI is composing as much of 30% of his company’s code.

The Verge reported the Google-Windsurf deal earlier on Friday.

Technology

Nvidia’s Jensen Huang sells more than $36 million in stock, catches Warren Buffett in net worth

Jensen Huang, CEO of Nvidia, holds a motherboard as he speaks during the Viva Technology conference dedicated to innovation and startups at Porte de Versailles exhibition center in Paris, France, on June 11, 2025.

Gonzalo Fuentes | Reuters

Nvidia CEO Jensen Huang unloaded roughly $36.4 million worth of stock in the leading artificial intelligence chipmaker, according to a U.S. Securities and Exchange Commission filing.

The sale, which totals 225,000 shares, comes as part of Huang’s previously adopted plan in March to unload up to 6 million shares of Nvidia through the end of the year. He sold his first batch of stock from the agreement in June, equaling about $15 million.

Last year, the tech executive sold about $700 million worth of shares as part of a prearranged plan. Nvidia stock climbed about 1% Friday.

Huang’s net worth has skyrocketed as investors bet on Nvidia’s AI dominance and graphics processing units powering large language models.

The 62-year-old’s wealth has grown by more than a quarter, or about $29 billion, since the start of 2025 alone, based on Bloomberg’s Billionaires Index. His net worth last stood at $143 billion in the index, putting him neck-and-neck with Berkshire Hathaway‘s Warren Buffett at $144 billion.

Shortly after the market opened Friday, Fortune‘s analysis of net worth had Huang ahead of Buffett, with the Nvidia CEO at $143.7 billion and the Oracle of Omaha at $142.1 billion.

The company has also achieved its own notable milestones this year, as it prospers off the AI boom.

On Wednesday, the Santa Clara, California-based chipmaker became the first company to top a $4 trillion market capitalization, beating out both Microsoft and Apple. The chipmaker closed above that milestone Thursday as CNBC reported that the technology titan met with President Donald Trump.

Brooke Seawell, venture partner at New Enterprise Associates, sold about $24 million worth of Nvidia shares, according to an SEC filing. Seawell has been on the company’s board since 1997, according to the company.

Huang still holds more than 858 million shares of Nvidia, both directly and indirectly, in different partnerships and trusts.

WATCH: Nvidia hits $4 trillion in market cap milestone despite curbs on chip exports

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike