Goldman Sachs jumps into bitcoin ETFs and one hedge fund gets bullish on miners

When the SEC opened the door in January for bitcoin exchange-traded funds to hit the mainstream, many traditional financial institutions across Wall Street and beyond finally had the opportunity to buy into crypto. Since then, money has poured in, but in fits and starts.

On Wednesday, banks and hedge funds with more than $100 million in assets hit a deadline to file their second-quarter 13F reports, disclosing their investments and what they bought and sold over a three-month stretch.

Goldman Sachs went big in the quarter, while rival Morgan Stanley trimmed its crypto holdings. JPMorgan has yet to make a big splash.

There are no shortage of opportunities for firms that want to take their time getting into the market. Following an array of public ETF listings in January tied to bitcoin, the Securities and Exchange Commission went a step further last month, clearing the way for spot ether ETFs, allowing investors to get access to the second-largest cryptocurrency. Those new holdings will start showing up in third-quarter reports.

In the period from March through June, Goldman Sachs made its debut in the crypto ETF market, purchasing $418 million worth of bitcoin funds. Its biggest position is a $238 million ownership in shares of BlackRock’s iShares Bitcoin Trust. The bank also owns shares in spot funds from Grayscale, Invesco, Fidelity and others.

Morgan Stanley was the first among the big players on Wall Street to give the green light to its 15,000 financial advisors to start pitching clients, who have a net worth north of $1.5 million, bitcoin ETFs, specifically those issued by BlackRock and Fidelity. Up to this point, wealth management businesses have only facilitated trades if customers requested exposure to the new spot crypto funds.

Of Morgan Stanley’s $1.5 trillion in assets under management, the bank disclosed in its filing that it trimmed its position in spot bitcoin ETFs to around $189 million from roughly $270 million. Most of those cuts were due to sales of almost all of its shares in the Grayscale Bitcoin Trust, which has a much higher management fee than other ETFs. The vast majority of the bank’s spot bitcoin holdings are now through the iShares trust.

JP Morgan reported minimal crypto exposure of around $42,000 worth of shares in Grayscale’s bitcoin fund and another $18,000 worth of the ProShares Bitcoin Strategy ETF. HSBC has nearly $3.6 million worth of spot bitcoin holdings, all from the fund issued by Ark 21Shares, UBS has around $300,000 worth of spot bitcoin ETF holdings, and Bank of America has collective holdings of around $5.3 million, mostly from BlackRock and Fidelity.

For most of the banks, the vast majority, if not all, of the ETF flows can be attributed to wealth management clients asking for exposure, rather than a decision by the firm to hold the assets on its balance sheet.

While Wall Street investment banks are coming in slowly, hedge funds are taking a more aggressive approach.

Millennium Management, which oversees $62 billion, now holds over $1.1 billion worth of shares in at least five Bitcoin ETFs, and is the single largest holder of shares in BlackRock’s bitcoin fund, with shares worth more than $371 million according to its August filing.

That’s down substantially from the $844 million worth of shares it held as of its May filing, having cut its stake in BlackRock’s fund by about half, and in Grayscale’s by more than half.

London-based Capula Investment Management, one of the top hedge funds in Europe with $30 billion under management, disclosed in a recent SEC filing that it holds more than $464 million in spot bitcoin ETFs, including the funds offered by BlackRock and Fidelity.

Point72 Asset Management and Apollo Management have also jumped into the market as have firms including Citadel Advisors, Jane Street and Fortress Investment Group.

Since launching in January, spot bitcoin funds have seen net flows of around $17.5 billion, bringing total assets in the funds to $53.5 billion as of mid-August. Grayscale’s fund, which existed previously and was converted to an ETF, has seen $19.4 billion in outflows since the change, though its new budget product has seen net inflows of $274 million.

Spot ether ETFs hold more than $7.6 billion as of Tuesday. Barclays analysts noted that trading volume across all spot crypto ETF products has declined, compared to spot exchange volumes.

Still, the new ETF activity has helped lift bitcoin prices, which hit a record above $73,000 in March. The price has since dropped sharply, to under $58,000, alongside volatility in the boarder markets, though it’s still up more than 30% this year.

“The crypto markets are strong because we have the sentiment shift,” Galaxy Digital chief Mike Novogratz told CNBC in May. “Crypto is now an asset class. It will be next year, it will be forever. And it wasn’t that way two years ago. There was risk around the asset class, and it’s been de risked.”

Bitcoin mining lures new investors

ETFs aren’t the only way investors are playing the market.

Daniel Sundheim’s D1 Capital built up a bitcoin mining position in the latest quarter, taking advantage of a shift as miners retrofit their facilities to service artificial intelligence clients. Like crypto mining, artificial intelligence workloads require immense amounts of power.

D1, which managed about $19 billion at the beginning of the year, bought nearly $5.4 million worth of Bitdeer Technologies, $17.3 million of Iris Energy, and nearly $17.4 million in shares of Hut 8 Corp.

Hut 8 said in its first-quarter earnings report that it had purchased Nvidia’s AI processors and secured a customer agreement with a venture-backed AI cloud platform as part of its expansion. Iris Energy expects to generate up to $17 million in annual revenue from its AI cloud services.

The combined market capitalization of the 14 major U.S.-listed bitcoin miners hit a record high of $22.8 billion on June 15, according to a note from JPMorgan, which has also been investing capital into an ETF of miners and individual companies. UBS has added shares of Bitdeer, Bitfarms, Bit Digital, Hut 8, as well as more than $5 million in Iris Energy, as of its latest 13F filing.

Sundheim, who previously built up a reputation as a savvy investor during his 15-year tenure at Viking Global Investors, has changed his tune on bitcoin. In 2019, he equated Canadian pot companies to the closest thing to a bubble since bitcoin.

Environment

All-new ALLPOWERS R1500 LITE station $405 (49% off), Gotrax F1 2.0 e-bike new $560 low, EcoFlow 35L GLACIER bundle low, more

, Gotrax F1 2.0 e-bike new 0 low, EcoFlow 35L GLACIER bundle low, more")

We’ve got a jam-packed Green Deals with plenty of low prices in our post-Prime Day market, with today’s edition led by the preorder launch deal on ALLPOWERS’ new R1500 LITE Portable Power Station at $405. Right behind it is Gotrax’s F1 2.0 20-inch Folding e-bike with five add-on accessories hitting a new $560 low, as well as EcoFlow’s 35L GLACIER Classic Portable Fridge/Freezer with an add-on battery at a new $859 low. We also have returning low prices on several Heybike models during its current weekend flash sale, like the Mars 2.0 Folding e-bike coming with $198 in free gear at $899. We’re also seeing EGO’s 56V 25-inch Cordless Hedge Trimmer Kit back at its $269 low, and have a special one-day-only low price on Birdfy’s Feeder 2 Duo with dual cameras at $330. Plus, there’s all the hangover Prime Day savings in our Prime Day Green Deals hub at the bottom of the page, as well as yesterday’s Tenways e-bike sale, the new low price hitting DJI’s latest Power 2000 station, and more.

Head below for other New Green Deals we’ve found today and, of course, Electrek’s best EV buying and leasing deals. Also, check out the new Electrek Tesla Shop for the best deals on Tesla accessories.

ALLPOWERS launches new R1500 LITE 1,056Wh LiFePO4 power station for preorder at $405

ALLPOWERS has launched its latest backup power solution for preorder with a significant discount through July 25. Until shipping begins, you can pick up the R1500 LITE Portable Power Station for $405 shipped, after an additional 10% savings is automatically added in your cart. This all-new unit will carry a full $799 price tag after these pre-sale savings end, with the brand offering a large 49% markdown right out of the gate, giving you $394 in savings and setting the bar for future discounts. On the same landing page, you’ll also find its many bundle options for varying sizes of accompanying solar panels.

ALLPOWERS’ new R1500 LITE station is the latest compact backup power solution from under the brand’s flag, coming with a 1,056Wh LiFePO4 capacity that is rated for over 3,500 life cycles, which would support you for over nine and a half years were you to discharge and recharge it every day. From its 12 output port options, it delivers up to 1,600W of steady juice to your devices, surging as high as 3,200W for hungrier appliances. Following a trend we’re seeing with each new power station that comes out, this one is designed to operate at “whisper-quiet” 35dB, so as not to disturb your sleep should you have it running at night.

The ALLPOWERS R1500 LITE station provides the usual remote smart controls you’d expect, giving you the ability to monitor its charging process and adjust settings all from your smartphone via the companion app. To recharge the station’s battery, you have four options. First, a standard wall outlet can have it back to full in 1.5 hours or you could connect up to its 650W max solar input to reach a full battery in 1.6 hours. There’s also the option to plug it into your car’s auxiliary port, as well as the ability to utilize both AC and solar for hybrid fast-charging that only takes a single hour.

Gotrax’s F1 2.0 20-inch folding e-bike comes with five add-on accessories at a new $560 low

Amazon is now offering the Gotrax F1 2.0 20-inch Folding e-bike at $559.99 shipped. While it carries a $999 MSRP direct from the brand, we see it occasionally keep to $799 in full at Amazon, with discounts so far this year having kept costs down as low as $625. You’re looking at a $239 markdown off the going rate ($439 off its MSRP), giving you a solid budget-friendly commuting option at the best new price we have tracked to date.

If you want to learn more about this e-bike and this deal, you can check out the full breakdown in our original coverage here.

EcoFlow’s 35L GLACIER Classic portable fridge/freezer comes with an add-on battery at its $859 low

EcoFlow’s official Amazon storefront is undercutting its direct pricing on the GLACIER Classic 35L Portable Fridge/Freezer with an add-on battery for $859 shipped at Amazon, while picking it up direct from the brand’s website would cost you an additional $90. This bundle package with the add-on battery usually goes for $1,098 in full, which we’ve been seeing keep down around $949 recently. Prime Day saw it hit the $859 low for the first time before rising back in price over the weekend, until now. You can pick it up here with a $239 markdown, equipping you with an ice-free option for outings at the best price we have tracked.

If you want to learn more about this electric cooler/freezer, be sure to check out our original coverage here.

Heybike summer flash sale drops Mars 2.0 fat tire folding e-bike with $198 in free gear back to its $899 low (Save $798 total)

Heybike has launched a Summer Flash Sale through July 20 that is seeing many of its e-bikes return to their lowest prices alongside solid savings on others. The standout is the popular Mars 2.0 Fat Tire Folding e-bike that comes with $198 in free gear at $899 shipped. The sale is bringing costs down from its $1,499 full price tag, which we regularly see drop between $999 and $1,099 during sales, occasionally falling further to the $899 low in flash events like this one. It’s coming back around again with $798 in total savings (including the free large basket and front basket you’ll get) at the best price we have tracked. Head below for more on this model and the others we’re seeing benefit from savings.

If you want to learn more about this e-bike or the other models seeing discounts during this flash sale, be sure to check out our original coverage here.

EGO’s 56V 25-inch cordless hedge trimmer kit gets larger post-Prime Day savings back to its $269 low

Amazon is offering a post-Prime Day return to the lowest pricing on the EGO Power+ 56V 25-inch Cordless Hedge Trimmer Kit for $269 shipped. Normally costing $349 at full price, we saw this same rate appear a month ago and hold out until the end of June, when it rose back up for the first week of July and only fell to $300 for Prime Day. Now, with that event having ended, the costs are coming back down with $80 in total savings to the best price we have tracked.

You can learn more about this electric lawn care solution by checking our original coverage here.

Get up close and personal with feathered visitors through Birdfy’s Feeder 2 Duo at $330 low (Today only)

As part of its Deals of the Day, Best Buy is offering the Birdfy Feeder 2 Duo with Camera at $329.99 shipped, while matching in price at Amazon. It carries a $430 MSRP direct from the brand, while sitting down lower at $420 at Best Buy. The deal we’re seeing here, which will only last through the rest of the day, gives you a 21% markdown off the going rate (23% off the MSRP), providing you with a $90 price cut ($100 off the MSRP) at the best price we can find. What’s more, this deal is coming in $20 under the direct pricing we’re seeing from the brand’s website, while over at Amazon the price is unmoved from its $

If you want to learn more about this advanced smart feeder system, be sure to check out our original coverage of this one-day-only deal here.

Best Summer EV deals!

- Ford Bronco e-bike (use code PDSG5OFF): $4,000 (Reg. $4,500)

- Ford Mustang e-bike (use code PDSG5OFF): $3,500 (Reg. $4,000)

- Aventon Ramblas Electric Mountain Bike: $2,599 (Reg. $2,899)

- Heybike Hero Carbon Fiber All-Terrain 750W mid-drive e-bike: $2,599 (Reg. $3,099)

- Ride1Up Prodigy v2 Brose Mid-Drive Gates Belt CVT e-bike: $2,595 (Reg. $2,795)

- Velotric Nomad 2X Multi-Terrain Camo e-bike with $50 bundle: $2,499 (No price cut)

- Ride1Up Revv 1 DRT Off-Road Moped-Style e-bike: $2,495 (Reg. $2,595)

- Ride1Up Revv 1 Full Suspension Moped-Style e-bike: $2,395 (Reg. $2,595)

- Heybike Hero Carbon Fiber All-Terrain 1,000W rear-hub e-bike: $2,299 (Reg. $2,599)

- Ride1Up Prodigy v2 Brose Mid-Drive 9-Speed e-bike: $2,095 (Reg. $2,495)

- Velotric Nomad 2 All-Terrain e-bike with $120 bundle (new model): $1,999 (No price cut)

- Rad Power Radster Road Commuter e-bike: $1,999 (Reg. $2,199)

- Rad Power Radster Trail Off-Road e-bike: $1,999 (Reg. $2,199)

- Lectric XPedition 2.0 35Ah Cargo e-bike w/ up to $703 bundle: $1,999 (Reg. $2,702)

- Tenways AGO X All-Terrain e-bike with $307 bundle: $1,899 (Reg. $2,499)

- Velotric Breeze 1 Cruiser e-bike with $150 bundle (new model): $1,799 (No price cut)

- Aventon Pace 4 Smart Cruiser e-bike (new model, first discount): $1,699 (Reg. $1,799)

- Lectric XPedition 2.0 26Ah Cargo e-bike w/ $554 bundle: $1,699 (Reg. $2,253)

- Lectric XPeak 2.0 Long-Range Off-Road e-bike with $316 bundle: $1,699 (Reg. $1,915)

- Aventon Abound Cargo e-bike: $1,599 (Reg. $1,999)

- Aventon Aventure 2 All-Terrain e-bike (2025 low): $1,599 (Reg. $1,999)

- Lectric XPeak 2.0 Standard Off-Road e-bike with $227 bundle: $1,499 (Reg. $1,726)

- Lectric XP Trike2 with $227 preorder bundle (through July 28): $1,499 (Reg. $1,726)

- Tenways CGO600 Pro e-bikes with $118 bundle: $1,499 (Reg. $1,899)

- Velotric Nomad 1 Plus All-Terrain e-bike with $69 bundle : $1,399 (Reg. $1,899)

- Fold 1 Plus e-bike with $120 bundle (new model): $1,499 (No price cut)

- Lectric XP Trike with $405 bundle: $1,499 (Reg. $1,904)

- Lectric XPedition 2.0 13Ah Cargo e-bike with $326 bundle: $1,399 (Reg. $1,725)

- Aventon Level 2 Commuter e-bike (2025 low): $1,399 (Reg. $1,899)

- Ride1Up Roadster V3 Lightweight Premium e-bike: $1,395 (Reg. $1,495)

- Velotric T1 ST Plus e-bike with $82 bundle (2025 low): $1,299 (Reg. $1,649)

- Lectric XPress 750 Commuter e-bikes with $336 bundle: $1,299 (Reg. $1,635)

- Lectric XP4 750 LR Folding Utility e-bikes with $356 bundle: $1,299 (Reg. $1,655)

- Heybike Brawn Off-Road e-bike: $1,299 (Reg. $1,799)

- Velotric Discover 1 Plus Commuter e-bike with $83 bundle (2025 low): $1,199 (Reg. $1,699)

- Lectric XP Lite 2.0 JW Black LR e-bike with $414 bundle: $1,099 (Reg. $1,513)

- Ride1Up Portola Folding e-bike with BOGO accessory promo: $995 (Reg. $1,095)

- Lectric XP4 Standard Folding Utility e-bikes with $79 bundle: $999 (Reg. $1,078)

- Lectric XP 3.0 Long-Range e-bikes (clearance price cut): $999 (Reg. $1,199)

- Lectric XP Lite 2.0 Long-Range e-bikes with up to $414 bundles: $999 (Reg. $1,413)

- Heybike Hauler Single-Battery Cargo e-bike: $999 (Reg. $1,499)

- Rad Power RadExpand 5 Folding e-bike (new low): $999 (Reg. $1,599)

- Segway ZT3 pro eKickScooter (new low): $850 (Reg. $1,300)

- Navee ST3 Pro Electric Scooter (new model): $760 (Reg. $1,014)

- Fold 1 Lite e-bike (new all-time low): $599 (Reg. $1,099)

- Navee GT3 Pro Electric Scooter (new model): $520 (Reg. $714)

Best new Green Deals landing this week

The savings this week are also continuing to a collection of other markdowns. To the same tune as the offers above, these all help you take a more energy-conscious approach to your routine. Winter means you can lock in even better off-season price cuts on electric tools for the lawn while saving on EVs and tons of other gear.

- EcoFlow launches Phase 3 Prime Day Sale with up to 60% discounts, multiple extra savings, free gifts, more from $209

- EcoFlow flash sale takes up to 53% off two power station offers, a WAVE 3 bundle, and an extra battery starting from $1,199

- Tenways AGO T mid-drive e-bike with a 62-mile range and $50 in free gear at $2,399 low in latest sale (Reg. $2,699), more from $1,499

- Score DJI’s latest Power 2000 2,048Wh LiFePO4 station with $900 savings at a new $999 low

- Tackle yard work with 8-in-1 versatility using Worx’s transforming Aerocart at $169.50 (Reg. up to $230)

- Tackle hedge jobs with this Greenworks 40V 20-inch pole trimmer at $114 low (Reg. $170)

- Prune in the thick of it all with Worx’s Nitro 20V 5-inch cordless mini chainsaw at $100 (Reg. $150)

- Prime Day Green Deals hub – Power stations, EVs, lawncare solutions, eco-friendly appliances, more

FTC: We use income earning auto affiliate links. More.

Chevy is bringing back the beloved affordable electric hatch. The new Chevy Bolt EV is expected to arrive later this year, featuring over 300 miles of driving range, faster charging, and more.

When will Chevy launch the new Bolt EV?

Many were sad to hear that GM was ending production of the iconic electric hatch in late 2023, but CEO Mary Barra promised a new Bolt EV was on the way.

Barra claimed the updated model would offer “an even better driving, charging, and ownership experience.” It will be based on GM’s Ultium platform, which powers current Chevy, Cadillac, GMC, and Honda electric vehicles sold in the US.

The platform will offer significantly longer driving range and faster charging speeds than the outgoing Bolt. GM also said it will use LFP batteries to lower costs.

Although LFP batteries typically offer less range compared to NMC, the new Chevy Bolt EV is expected to arrive with over 300 miles of driving range. Given that the Chevy Silverado EV WT offers up to 492 miles of EPA-estimated range, 300 miles for the Bolt EV shouldn’t be too hard, even with LFP batteries.

GM’s president, Mark Reuss, confirmed the new model will be a part of a “family of Bolts,” which will include an even more affordable variant.

After announcing plans to invest $4 billion in ramping up US production last month, GM said a new “next-gen affordable EV” was in development. It will be built in Kansas, alongside the new Chevy Bolt EV. Whether this model is part of the family of Bolt’s or not remains unclear.

With an official debut expected later this year, we’ve seen the new Bolt out for testing. Although it keeps the overall feel of the outgoing Bolt, it appears to have a more crossover-SUV look, similar to the Trax.

According to Edmunds, GM’s Super Cruise hands-free highway tech will be available on the upcoming Bolt EV. In the previous generation, it was only offered on the bigger EUV model.

With some GM electric vehicles now arriving with a built-in NACS port for Tesla Supercharger access, the new Bolt will likely also feature it.

GM is set to begin production later this year, with the new Chevy Bolt EV expected to be available in mid-2026. Prices and final specs will come closer to launch, but the first model from the Bolt EV family is likely to start at a slightly higher price than the $28,785 MSRP of the outgoing model, given the upgrades.

Meanwhile, Chevy already has an affordable model that’s helped it become the fastest-growing EV brand in the US. The Chevy Equinox EV, or “America’s most affordable 315+ range EV,” as GM likes to call it, starts at under $35,000. With the $7,500 EV tax credit, the price of the base LT model drops to just $27,495.

With leases starting at just $289 per month, it’s no wonder the electric SUV is selling like hotcakes. GM expects the Chevy Equinox EV to be among the top-three-selling EVs by the end of 2025.

Ready to test one out for yourself? We’ve got you covered. You can use our link to find deals on the Chevy Equinox EV at a dealer near you (trusted affiliate link).

FTC: We use income earning auto affiliate links. More.

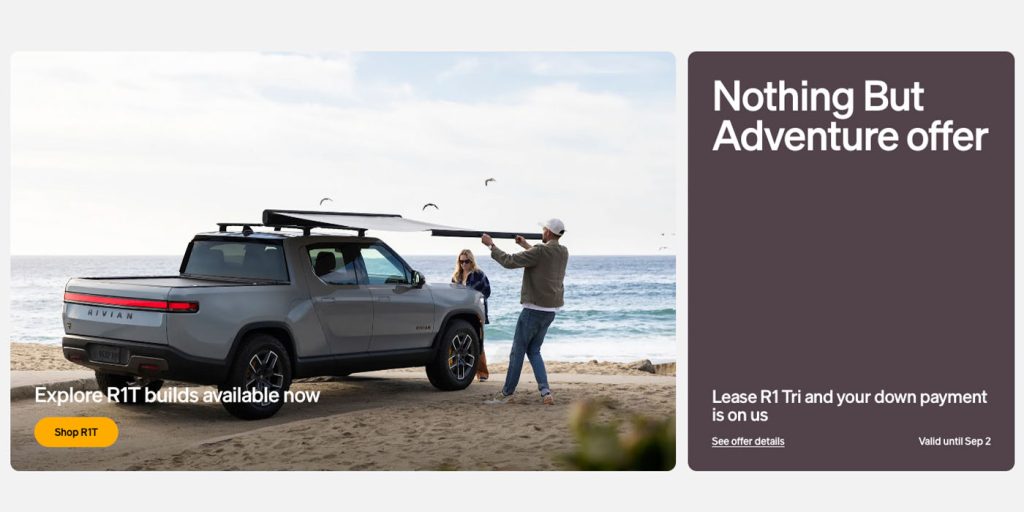

We’ve already reached peak summertime (crazy), and your back patios aren’t the only thing heating up. Rivian has extended its lease deals, which apply to a range of R1S and R1T configurations. Combined with federal tax credits, you could save upwards of $15,000 on a new Rivian EV.

Today’s latest deals update is an extension (and a welcome one at that) of two separate lease deal programs that Rivian announced earlier this summer. In May, we reported that Rivian had begun a “Nothing But Adventure” lease offer, which covered the $6,500 down payment on the lease of any R1 EV with a dual motor configuration with the Max battery pack and performance upgrade package.

However, that deal was originally set to expire on May 31, 2025. In June, Rivian followed up with a second deal called the “Summer Adventure Offer,” which included $5,000 off the purchase or lease of a new Tri-Motor R1 EV if customers took delivery by June 30.

Below, we have broken down Rivian’s latest offers, which include revamped lease deals that have been extended through the rest of the summer.

Rivian lease deals on dual, tri motor R1S and R1T EVs

Rivian sent an email earlier today outlining details of its latest lease offers, which include multiple deals valid through September 1, 2025. That includes the previously mentioned “Nothing But Adventure” offer, which now pertains to any 2025 Tri-Motor R1S or R1T lease.

Similar to the May 2025 deal, Rivian will contribute $6,500 toward the down payment of said lease, as long as you place your order by September 1 and take delivery by September 30. Combined with the $7,500 federal EV lease credit and a $1,500 bonus from Rivian for trading in any vehicle, you can save as much as $15,500. Check out all the terms and conditions here.

Rivian’s “Summer Adventure Offer” expired last month. Still, the American automaker has followed up with a new “Summer Lease Offer” that applies to any 2025 Dual Motor R1 model with the performance upgrade. Combined with the federal credit and Rivian Energy Refresh bonus of $1,500, customers can save up to $14,000 on an R1S or R1T with a Max battery pack, and up to $12,000 with those dual models with the Large pack.

Per Rivian, the summer lease offers between $3,000 and $5,000 will be applied directly to your 2025 Dual Motor order as long as it’s on or before September 1, 2025, and delivery is taken by September 30. To peruse the lease deals, you can connect with a Rivian sales advisor or go to R1 Shop.

FTC: We use income earning auto affiliate links. More.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike