Budget 2024: How fiscal rules are impeding long-term investments – and what Rachel Reeves can do about it

Before we get onto the budget and what Rachel Reeves might do to fiddle her fiscal rules and give herself a little more room to spend, I want you to ponder, for a moment, a recent report from the Office for Budget Responsibility (OBR).

This wasn’t one of those big OBR reports that get lots of attention – such as the documents and numbers it produces alongside each budget, full of the forecasts and analyses on the state of the economy and the public finances.

Instead, it was a chin-scratchy working paper that asked the question: if the government invests in something – say, a road or a railway, or a new school building – how long does it generally take for that investment to come good?

The answer, according to the report, was: actually quite a long time. Imagine the government spends a chunk of money – 1% of national income – on investment this year. In five years’ time that investment will only have created 0.4 per cent of GDP. In other words, in net terms, it’s costed us 0.6% of GDP.

But, and this is the important thing, look a little further off. A high-speed rail network is designed to last decades, and as those decades go on, it gradually improves people’s lives – think of the time saved by each commuter each day – small amounts each day, but they gradually mount up. So while the investment costs money in the short run, in the longer run, the benefits gradually mount.

The OBR’s calculation was that while a 1% of GDP public investment would only deliver 0.4% of GDP in five years, by the time 10 or 12 years had passed, the investment would be responsible for approaching 1% of GDP. In other words, it would have broken even. The money put in at the start would be fully earned back in benefits.

And by the time that investment was 50 years old, it would have delivered a whopping 2.5% of GDP in economic benefits. Future generations would benefit enormously – or so said the OBR’s sums.

Having laid that out, I want you now to ponder the fiscal rules Rachel Reeves is confronted with at this, her first budget. Most pressingly, ponder the so-called debt rule, which insists that the chancellor must have the national debt – well, technically it’s “public sector net debt excluding Bank of England interventions” – falling within five years.

There is, it’s worth underlining at this point, nothing fundamental about this rule. Reeves inherited it from the Conservative Party, who only dreamed it up a few years ago, after COVID. Back before then, there have been countless rules that were supposed to prevent the national debt falling and, frankly, rarely ever succeeded.

But since Reeves wanted everyone to know, ahead of the election, just how serious Labour was about managing the public finances, she decided she would keep those Tory rules. One can understand the politics of this; the economics, less so – then again, I confess I’ve always been a bit sceptical about all these rules.

The upshot is, to meet this rule, she needs the national debt to be falling between the fourth and fifth year of the OBR’s five-year forecast. And according to the last OBR forecasts, which date back to Jeremy Hunt‘s last budget, it is. But not by much: only by £8.9bn. If that number rings a bell, it is because this is the much-vaunted, but not much understood, “headroom” figure a lot of people in Westminster like to drone on about.

Read more from Sky News:

Abolishing national insurance ‘could take several parliaments’

UK has no ‘credible’ plan to fund military equipment

And – if you’re taking these rules very literally, which everyone in Westminster seems to be doing – then the takeaway is that the chancellor really doesn’t have much room left to spend in the coming budget. She only has £8.9bn extra leeway to borrow!

Every spending decision – whether on investment, on the NHS, on benefits or indeed on anything else, happens in the shadow of this terrifying £8.9bn headroom figure. And since the chancellor has already explained, in her “black hole” event earlier this year, that the Conservatives promised a lot of extra spending they hadn’t budgeted for – not, perhaps, the entire £22bn figure she likes to cite but still a fair chunk – then it stands to reason there’s really “no money left”.

Or is there? So far we’ve been taking the fiscal rules quite literally but at this stage it’s worth asking the question: why? First off, there’s nothing gospel about these rules. There’s no tablet of stone that says the national debt needs to be falling in five years’ time.

Second, remember what we learned from that OBR paper. Sometimes investments in things can actually generate more money than they cost. Yet fixating on a debt rule means the money you borrow to fund those investments is always counted as a negative – not a positive. And since the debt rule only looks five years into the future, you only ever see the cost and not the breakeven point.

Third, the debt rule used by this government actually focuses on a measure of the national debt which might not necessarily be the right one. That might sound odd until you realise there are actually quite a few different ways of expressing the scale of UK national debt.

The measure we currently use excludes the Bank of England, which seemed, a few years ago, to be a sensible thing to do. The Bank has been engaged in a policy called quantitative easing which involves buying and selling lots of government debt – which distorts the national debt. Perhaps it’s best to exclude it.

Except that recently those Bank of England interventions have actually been serving to drive up losses for the state. I won’t go into it in depth here for risk of causing a headache, but the upshot is most economists think focusing on a debt measure which is mostly being affected right now not by government decisions but by the central bank reversing a monetary policy exercise seems pretty perverse.

In other words, there’s a very strong argument that instead of focusing on the ex-BoE measure of net debt, the fiscal rules should instead be focusing on the overall measure of net debt. And here’s the thing: when you look at that measure of net debt, lo and behold it’s falling more between year four and five. In other words, there’s considerably more headroom: just under £25bn rather than just under £9bn based on that other Bank-excluding measure of debt.

Keep up with all the latest news from the UK and around the world by following Sky News

Might Reeves declare, at the budget or in the run-up, that it makes far more sense to focus on overall PSND from now on? Quite plausibly. And while in one respect it’s a fiddle, in her defence it’s a fiddle from one silly rule to an ever so slightly less silly rule.

It would also mean she has more room to borrow to invest – if that’s what she chooses to do. But it doesn’t resolve the deeper issue: that both of these measures fixate on the short-term cost of debt without taking into account the long-term benefits of investment – back to that OBR paper.

If Reeves is determined to stick to the, some would say arbitrary, five-year deadline to get debt falling but wants to incorporate some measure of the benefits of investment, she could always choose one of two other measures for this rule.

She could focus on something called “public sector net financial liabilities” or “public sector net worth”. Both of these measures include some of the assets owned by the state as well as its debts – the upshot being that hopefully they reflect a little more of the benefits of investing more money.

The problem with these measures is they are subject to quite a lot of revision when, say, accountants change their opinion about the value of the national road or rail network. So some would argue these measures are prone to more volatility and fiddling than simple net debt.

Even so, these measures would dramatically transform the “headroom” picture. All of a sudden, Reeves would have over £60bn of headroom to play with. More than enough to splurge on loads of investments without breaking her fiscal rule.

There’s one other change to the rule that would probably make more sense than any of the above: changing that five-year deadline to a 10 or even 15-year deadline. At that kind of horizon, a pound spent on a decent investment would suddenly look net positive for the economy rather than a drain.

Whether Reeves wants to do any of the above depends, ultimately, on how she wants to begin her term in office. Does she want to establish herself as a tough, fiscally conservative Chancellor – with a view, perhaps, to relaxing in later years? Or does she feel it’s more important to begin investing early, so some of the potential benefits might be obvious within a decade or so?

Really, there’s nothing in the economics to stop her choosing either path. Certainly not a set of fiscal rules which are riddled with flaws.

The nine largest US banks restricted financial services to politically contentious industries, including cryptocurrency, between 2020 and 2023, according to the preliminary findings of the Office of the Comptroller of the Currency (OCC).

The banking regulator said on Wednesday that its early findings show that major banks “made inappropriate distinctions among customers in the provision of financial services on the basis of their lawful business activities” across the three-year period.

The banks either implemented policies restricting access to banking or required escalated reviews and approvals before giving financial services to certain customers, the OCC said, without giving specific details.

The OCC initiated its review after President Donald Trump signed an executive order in August, directing a review of whether banks had debanked or discriminated against individuals based on their political or religious beliefs.

Crypto issuers and exchanges caught in restrictions

The OCC’s report found that in addition to crypto, the sectors that faced banking restrictions included oil and gas exploration, coal mining, firearms, private prisons, tobacco and e-cigarette manufacturers and adult entertainment.

Banks’ actions toward crypto included restrictions on “issuers, exchanges, or administrators, often attributed to financial crime considerations,” the OCC said.

“It is unfortunate that the nation’s largest banks thought these harmful debanking policies were an appropriate use of their government-granted charter and market power,” said Comptroller of the Currency Jonathan Gould.

“While many of these policies were undertaken in plain sight and even announced publicly, certain banks have continued to insist that they did not engage in debanking,” he added.

The OCC examined JPMorgan Chase, Bank of America, Citibank, Wells Fargo, US Bank, Capital One, PNC Bank, TD Bank and BMO Bank, the largest national banks it regulates.

The OCC reported that it is continuing its investigation and could refer its findings to the Justice Department.

OCC debanking report leaves “much to be desired”

Nick Anthony, a policy analyst at libertarian think tank the Cato Institute, said in an emailed statement to Cointelegraph that the OCC’s report “leaves much to be desired” and didn’t mention “the most well-known causes of debanking.”

“The report criticizes banks for severing ties with controversial clients, but it fails to mention that regulators explicitly assess banks on their reputation,” he said.

Related: ‘Grow up… We debank Democrats, we debank Republicans:’ JPMorgan CEO

“Making matters worse, the report appears to blame banks for cutting ties with cryptocurrency companies, yet makes no mention of the fact that the [Federal Deposit Insurance Corporation] explicitly told banks to stay away from these companies,” Anthony added.

Republicans on the House Finance Committee reported earlier this month that the FDIC’s so-called “pause letters” it sent to banks under the Biden administration helped to spur “the debanking of the digital asset ecosystem.”

Caitlin Long, the founder and CEO of the crypto-focused Custodia Bank, said the “worst culprits” of crypto-related debanking under the Biden administration were the FDIC and Federal Reserve, “not OCC.”

“In OCC’s defense, this report covers large banks only. Crushing crypto wasn’t a supervisory priority for large banks like it was for small [and] mid-sized banks,” she added.

Magazine: Quitting Trump’s top crypto job wasn’t easy: Bo Hines

Politics

Live music venues warn of ‘devastating consequences’ of budget tax changes in letter to Sir Keir Starmer

Tax changes announced in the budget could have “devastating, unintended consequences” on live music venues, including widespread closures and job losses, trade bodies have warned.

The bodies, representing nearly 1,000 live music venues, including grassroots sites as well as arenas such as the OVO Wembley Arena, The O2, and Co-op Live, are calling for an urgent rethink on the chancellor’s changes to the business rates system.

If not, they warn that hundreds of venues could close, ticket prices could increase, and thousands could lose their jobs across the country.

Politics latest: Ex-Olympic swimmer nominated for peerages

Business rates, which are a tax on commercial properties in England and Wales, are calculated through a complex formula of the value of the property, assessed by a government agency every three years. That is then combined with a national “multiplier” set by the Treasury, giving a final cash amount.

The chancellor declared in her budget speech that although she is removing the business rates discount for small hospitality businesses, they would benefit from “permanently lower tax rates”. The burden, she said, would instead be shifted onto large companies with big spaces, such as Amazon.

But both small and large companies have seen the assessed values of their properties shoot up, which more than wipes out any discount on the tax rate for small businesses, and will see the bills of arena spaces increase dramatically.

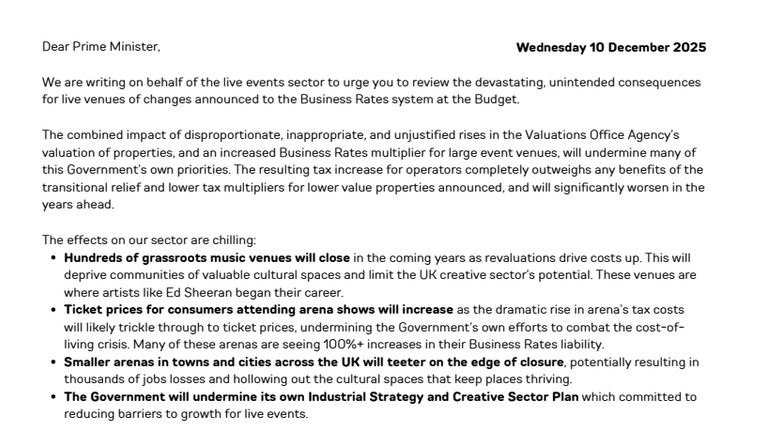

In the letter, coordinated by Live, the trade bodies write that the effect of Rachel Reeves’s changes are “chilling”, saying: “Hundreds of grassroots music venues will close in the coming years as revaluations drive costs up. This will deprive communities of valuable cultural spaces and limit the UK creative sector’s potential. These venues are where artists like Ed Sheeran began their career.

“Ticket prices for consumers attending arena shows will increase as the dramatic rise in arena’s tax costs will likely trickle through to ticket prices, undermining the government’s own efforts to combat the cost of living crisis. Many of these arenas are seeing 100%+ increases in their business rates liability.

“Smaller arenas in towns and cities across the UK will teeter on the edge of closure, potentially resulting in thousands of jobs losses and hollowing out the cultural spaces that keep places thriving.”

The full letter from trade bodies to the prime minister.

They go on to warn that the government will “undermine its own Industrial Strategy and Creative Sector Plan which committed to reducing barriers to growth for live events”, and will also reduce spending in hotels, bars, restaurants and other high street businesses across the country.

To mitigate the impact of the tax changes, they are calling for an immediate 40% discount on business rates for live venues, in line with film studios, as well as “fundamental reform” to the system used to value commercial properties in the UK, and a “rapid inquiry” into how events spaces are valued.

Sky’s Jess Sharp explains how the budget could impact your money

In response, a Treasury spokesperson told Sky News: “With Covid support ending and valuations rising, some music venues may face higher costs – so we have stepped in to cap bills with a £4.3bn support package and by keeping corporation tax at 25% – the lowest rate in the G7.

“For the music sector, we are also relaxing temporary admission rules to cut the cost of bringing in equipment for gigs, providing 40% orchestra tax relief for live concerts, and investing up to £10m to support venues and live music.”

The warning from the live music industry comes after small retail, hospitality and leisure businesses warned of the potential for widespread closures due to the changes to the business rates system.

Sky’s political editor Beth Rigby challenged Prime Minister Sir Keir Starmer on the tax rises in the budget.

Sky News reported after the budget that the increase in business rates over the next three years following vast increases in the assessed values of commercial properties has left small retail, hospitality and leisure businesses questioning whether their businesses will be viable beyond April next year.

Analysis by UK Hospitality, the trade body that represents hospitality businesses, has found that over the next three years, the average pub will pay an extra £12,900 in business rates, even with the transitional arrangements, while an average hotel will see its bill soar by £205,200.

Read more: Hospitality pleads for ‘lifeline’

A Treasury spokesperson said their cap for small businesses will see “a typical independent pub pay around £4,800 less next year than they otherwise would have”.

“This comes on top of cutting licensing costs to help more venues offer pavement drinks and al fresco dining, maintaining our cut to alcohol duty on draught pints, and capping corporation tax,” they added.

The Chancellor Rachel Reeves has acknowledged there were “too many leaks” in the run-up to last month’s budget.

The flow of budget content to news organisations was “very damaging”, Ms Reeves told MPs on the Treasury select committee on Wednesday.

“Leaks are unacceptable. The budget had too much speculation. There were too many leaks, and much of those leaks and speculation were inaccurate, very damaging”, she said.

Money blog: Nine-year-old set up Christmas tree business to pay for university

The cost of UK government borrowing briefly spiked after news reports that income taxes would not rise as first expected and Labour would not break its manifesto pledge.

An inquiry into the leaks from the Treasury to members of the media is to take place. But James Bowler, the Treasury’s top official, who was also giving evidence to MPs, would not say the results of it would be published.

Committee chair Dame Meg Hillier asked if the group of MPs could see the full inquiry.

“I’d have to engage with the people in the inquiry about the views on that”, replied Mr Bowler, permanent secretary to the Treasury.

OBR leak ‘a mistake of such gravity’

The entire contents of the budget ended up being released 40 minutes early via independent forecasters, the Office for Budget Responsibility (OBR).

A report into this error found the OBR had uploaded documents containing their calculations of budget numbers to a link on the watchdog’s website it had mistakenly believed was inaccessible to the public.

Tax rises ruled out

The chancellor ruled out future revenue-raising measures, including applying capital gains tax to primary residences and changing the state pension triple.

Committee member and former chair Dame Harriet Baldwin had noted that the chancellor’s previous statement to the MPs when she said she would not overhaul council tax and look at road pricing, turned out to be inaccurate.

During the budget, an electric vehicle charge per mile was introduced, as was an additional council tax for those with properties worth £2m or more.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024