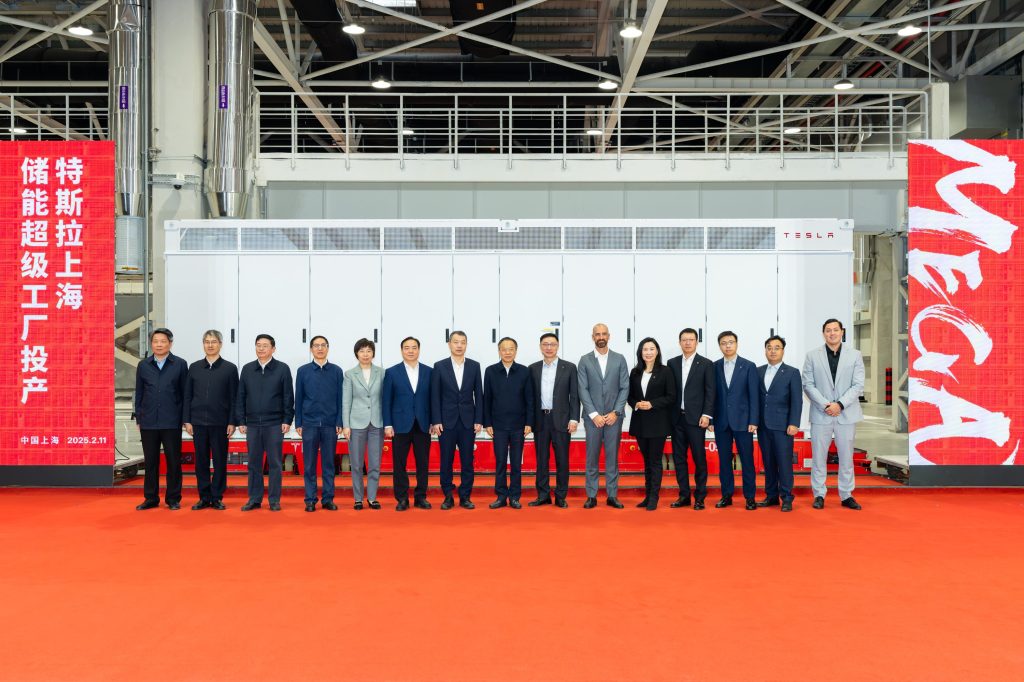

Tesla starts production at Megafactory in Shanghai

Tesla has started production at its new Megafactory in Shanghai, its second such factory, and it is starting to ship to its first customer.

Energy storage has been Tesla’s silver lining over the last few quarters.

While its main business, the automotive business, has been shrinking in both revenue and margins, its energy storage business has been growing at an impressive pace.

That’s mainly due to its Megapacks, its popular utility-scale energy storage systems, and the production ramp at its Megafactory in California, where it produces those battery packs.

Tesla has ramped up production at the plant with a capacity of 40 GWh.

The company has also been building its second Megafactory, this one in Shanghai, China.

Today, Tesla announced that it has produced its first Megapack at the Shanghai factory and released these pictures:

Tesla also said that it will soon ship the first Megapacks to Australia from this factory.

Australia has been one of Tesla’s earliest customers of large-scale energy storage systems and it will make more sense to ship Megapacks from China than from the US.

This second Megafactory will help the logistics of Tesla’s energy storage business.

While Tesla’s energy storage volumes are ramping up, the company has had to slash Megapack prices over the last year, which is resulting in lower margins.

The company is also facing stronger competition. Its own battery cell suppliers, BYD and CATL, have released similar products as Megapacks.

FTC: We use income earning auto affiliate links. More.

Locals call him the “Bicycle hero,” but Texas man Evan Wayne says he’s just doing what he can to help his community after it was cut off due to the recent devastating and deadly flooding tragedy.

When the local Sandy Creek flooded following torrential rains in Texas, it destroyed the only bridge into one community. Residents were cut off from access to supplies, including everything from necessities like food, water, and medicine to basic comforts.

Although the bridge was impassable to cars, volunteers who quickly organized to help the stranded residents found that the damaged bridge could still be traversed on foot. Or in the case of Evan Wayne, it could be covered by an electric bike.

Evan joined hundreds of volunteers who answered the call of grassroots organizers by working together without any official capacity. While many started by hand-pulling garden carts of supplies uphill to reach the stricken community, Evan jury-rigged a trailer to an e-bike and took on as much of the load as he could, helping shuttle much-needed food and gear into the community over hundreds of round-trip journeys.

“This was a dog trailer 48 hours ago. I had a hacksaw, hacked the top off, grabbed some bungee cords, and here we are,” explained Evan in an interview with CBS Austin, while waiting for the next load of gear to be stacked on his trailer.

In the first two days of the operation, he made around 100 round trips each day, shuttling food and water as well as critical rescue supplies. “Right now, I’m waiting on a couple of chainsaws that I’ll bring in for a crew that’s been going at it with handsaws so far.”

In addition to delivering needed supplies, Evan has often found himself moving something even more important: information. “I’ve flagged down medics. I’ve been the guy that goes between Austin EMT and STAR Flight because I’m quicker than cell phones sometimes, people don’t have signal a lot of the time.”

Evan quickly points out that he isn’t the only one helping. “I’ve got an e-bike, but other people are pulling carts. People are walking, people are carrying things. Everyone is doing what they can.” But there’s no doubt that his ability to carry more gear at higher speeds and make hundreds of round-trip journeys so far in and out of the stricken neighborhood has helped impact countless lives.

“This is all volunteers here. They’re just taking it upon themselves to get people where they need to go. I think there’s an umbrella company coming in, taking over tomorrow, but until they get here, people are just taking care of people, which is what you’ve got to do.”

E-bikes proving their worth in emergencies

While many people consider electric bicycles just another form of recreation, they’ve proven to be potent transportation alternatives after natural disasters worldwide.

Not only do their small and efficient batteries make performing hundreds of rescue trips like Evans’ possible, but recharging can be done simply and easily with a solar panel when electricity is out after a disaster. And when gas stations are out of fuel (or simply can’t pump it with the power grid down), e-bikes can keep running while gasoline-powered motorcycles or ATVs run dry.

Electric bicycle batteries have also proven to be a handy source of emergency power after hurricanes and other disasters, often helping owners keep their phones charged up for days to remain in contact with family or rescue services.

While most hope to never need theirs for emergency purposes, electric bicycles have proven their worth in countless disaster scenarios, adding benefits far beyond just alternative transportation, recreation, or fitness riding.

Image credits: CBS Austin (screenshots), used under fair use

FTC: We use income earning auto affiliate links. More.

Twitter CEO Jack Dorsey testifies during a remote video hearing held by subcommittees of the U.S. House of Representatives Energy and Commerce Committee on “Social Media’s Role in Promoting Extremism and Misinformation” in Washington, U.S., March 25, 2021.

Handout | Via Reuters

Block jumped more than 5% on Monday, leading a rally in shares of fintech companies as analysts downplayed the threat of JPMorgan Chase’s reported plan to charge data aggregators for access to customer financial information.

The recovery followed steep declines on Friday, after Bloomberg reported that JPMorgan had circulated pricing sheets outlining potential fees for aggregators like Plaid and Yodlee, which connect fintech platforms to users’ bank data.

In a note to clients on Monday, Evercore ISI analysts said the potential new expenses were “far from a ‘business model-breaking’ cost increase.”

In addition to Block’s rise, PayPal climbed 3.5% on Monday after sliding Friday. Robinhood and Shift4 recorded modest gains.

Broader market momentum helped fuel some of the rebound. The Nasdaq closed at a record, and crypto rallied, with bitcoin climbing past $123,000. Ether, solana, and other altcoins also gained.

Evercore ISI’s analysts said that even if JPMorgan’s changes were implemented, the most immediate effect would be a slight bump in the cost of one-time account setups — perhaps 50 to 60 cents.

Morgan Stanley echoed that view, writing that any impact would be “negligible,” especially for large fintechs that rely more on debit, credit, or stored balances than bank account pulls for transactions.

PayPal doesn’t anticipate much short-term impact, according to a person with knowledge of the issue. The person, who asked not to be named in order to speak about private financial matters, noted that PayPal relies on aggregators primarily for account verification and already has long-term pricing contracts in place.

While smaller fintechs that depend heavily on automated clearing house (ACH) rails or Open Banking frameworks for onboarding and compliance may face real pressure if the fees take effect, analysts said the larger platforms are largely insulated.

WATCH: Congress moves to redraw $3.7 trillion crypto market rules, opening door to Wall Street

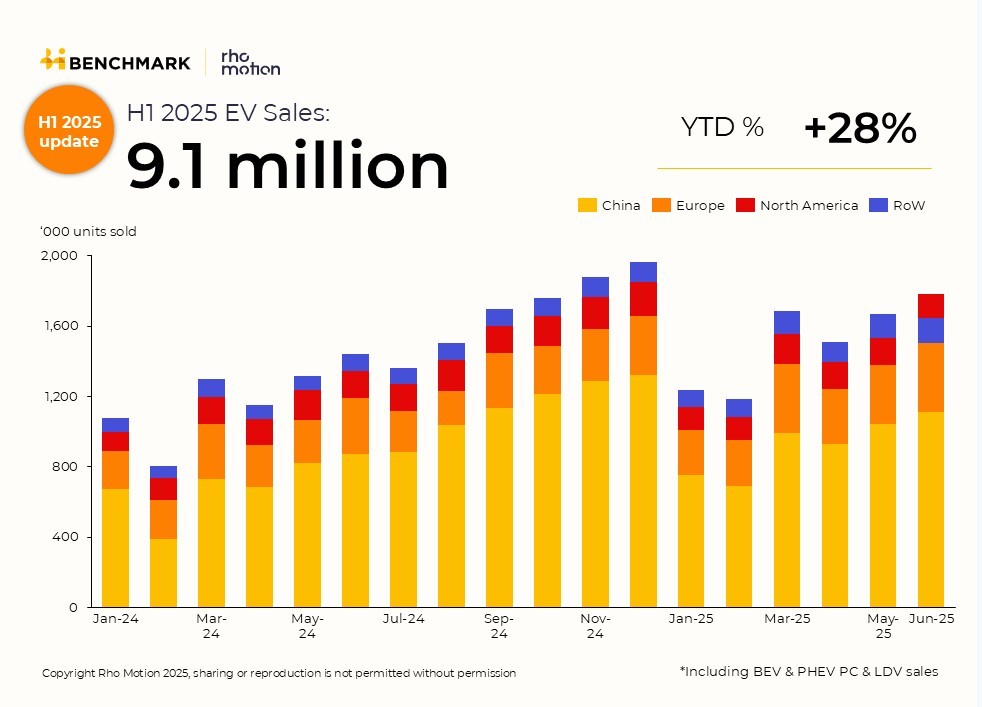

The global EV market is still charging ahead. According to new numbers from global research firm Rho Motion, 9.1 million EVs were sold worldwide in the first half of 2025, up 28% compared to the same period last year. But not every region is accelerating at the same pace.

China and Europe are doing the heavy lifting

More than half of the world’s EVs this year have been bought in China. That market hit 5.5 million sales in the first six months of 2025 – a 32% jump year-over-year. Around half of new cars bought in China are now electric.

While some Chinese cities’ subsidies have dried up, Rho Motion expects momentum to pick back up later in the year as more funding is released.

In Europe, 2 million EVs were sold in the first half of the year, up 26%. Battery electric vehicle (BEV) sales also rose 26%, thanks in part to affordable models like the Renault 4 (pictured) and 5 entering the market. Plug-in hybrids (PHEVs) weren’t far behind, growing 27% year-to-date. Chinese automakers are leaning into PHEVs as a way to work around the EU’s new tariffs on BEVs.

Spain is leading the pack with EV sales soaring 85% so far this year. Its generous MOVES III incentive program was extended in April and has kept sales strong. The UK and Germany are also seeing solid growth – 32% and 40%, respectively. France, however, is slumping. With subsidies cut, EV sales there have dropped 13%.

North America is stuck in the slow lane

Things aren’t looking quite as bright in North America. EV sales in the US, Canada, and Mexico are up just 3% so far this year.

Mexico is the one bright spot, with a 20% boost. The US is up 6%. But Canada is down a whopping 23%.

And things could get bumpier. On July 4, Trump signed Congress’s big bill into law, which axes all the Inflation Reduction Act EV tax credits. Those consumer credits for EVs now officially end on September 30.

Just over half of the EVs sold in the US this year qualified for those credits. Rho Motion predicts a rush in Q3 before the subsidies disappear – and a decline in sales after that.

Rho Motion data manager Charles Lester said, “With Trump’s latest cuts in his ‘Big Beautiful Bill,’ the US could struggle to see any growth in the EV market overall in 2025.”

Global EV sales snapshot, H1 2025 vs H1 2024

- Global: 9.1 million (+28%)

- China: 5.5 million (+32%)

- Europe: 2.0 million (+26%)

- North America: 0.9 million (+3%)

- Rest of world: 0.7 million (+40%)

Read more: China breaks records as global EV sales hit 7.2 million in 2025

The 30% federal solar tax credit is ending this year. If you’ve ever considered going solar, now’s the time to act. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike