OBR slashes UK growth forecast for 2025 but upgrades it for rest of parliament

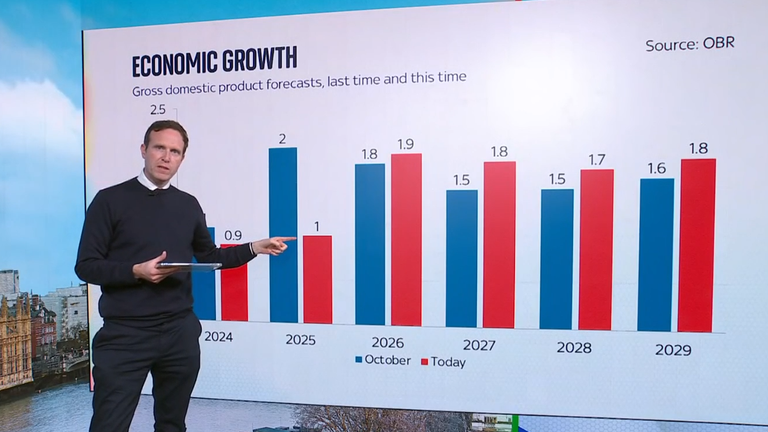

The Office for Budget Responsibility has halved the UK growth forecast for 2025 from 2% to 1%, Chancellor Rachel Reeves has said.

However, the fiscal watchdog said that while growth has been downgraded for this year, it had been upgraded for every year after for the rest of this parliament – which is due to end in 2029.

The chancellor said she is “not satisfied with the numbers” for this year as she delivered her long-awaited spring statement in the House of Commons.

Politics latest: Follow live updates

But, she explained, the OBR has forecast growth to hit 1.9% in 2026, 1.8% in 2027, 1.7% in 2028, and 1.8% in 2029.

Some tough forecasts beyond headline figures

The independent forecaster also published its economic outlook on Wednesday, showing there’s a 54% chance the chancellor will not break her self-imposed fiscal rules to bring down government debt and balance the budget by 2030.

Living standards, as measured by household disposable income, will fall after this year to almost no growth in 2027-28 before rising again due to firms rebuilding profit margins, wage growth slowing, taxes rising, and welfare measures taking effect.

The OBR also raised its expectation for unemployment and net migration – the number of people immigrating to the UK minus those emigrating.

The unemployment rate, the percentage of people out of work, will rise to 4.5% this year. This is 0.4 percentage points or 160,000 people higher than first thought in the October forecast.

Net migration will fall sharply, the OBR said, due to a tightening of visa policies and higher levels of emigration. But the forecast has been upped by 25,000 since October as a higher share of immigrants are staying in the UK under the new migration system.

The Chancellor said the OBR has downgraded the UK growth forecast for 2025 from 2% to 1%.

At the same time, there will be a reduction in people neither in work nor looking for work due to a reduction in caring as birth rates fall and childcare provision is expanded.

But there are also fewer people in this position, classed as “economically inactive” than previously thought, the OBR said. The government launched its welfare cuts in an effort to reduce this economic inactivity.

Further cuts are to come, the OBR said, as “unprotected” government departments such as local government justice, the environment, Home Office and culture may need to be cut by 0.8% a year from 2026-27 “to accommodate assumed commitments in other areas”.

Prices overall will go up even higher than initially anticipated, according to the OBR, which now forecasts inflation will rise to 3.8% in July due to higher energy, food and water bills. This will fall rapidly, however, from next year.

‘No shortcuts to growth’

Ms Reeves told MPs: “There are no shortcuts to economic growth. It will take long-term decisions. It will take hard yards. It will take time for the reforms we are introducing to be felt in the everyday economy.

“It is right that the Office for Budget Responsibility consider the evidence and look carefully at measures before recognising a growth impact in their forecast.”

The chancellor pointed to changes to the National Planning Policy Framework, saying mandatory housing targets and bringing “grey belt” land into scope for development will “permanently increase the level of real GDP by 0.2% by 2029-30”.

This will bring an “additional £6.8bn in our economy and by 0.4% of GDP within the next 10 years”, she said.

Ms Reeves also highlighted reforms to the pension system and a national wealth fund, adding it was part of a “serious plan” for economic growth.

Also announced in the spring statement today:

- The budget will move from a deficit of £36.1bn in 2025/26 and £13.4bn in 2026/27, to a surplus of £6bn in 2027/28, £7.1bn in 2028/29 and £9.9bn in 2029/30;

- The Office for Budget Responsibility estimates Labour’s cuts to the welfare budget will save £4.8bn, with changes going further than initially thought;

- Reeves says the health element of universal credit will be cut by half and frozen for new claimants;

- There are no more tax rises today, but the chancellor claims she’ll raise an extra billion pounds by cracking down more on tax evasion;

- Day-to-day spending will be protected, other than the aid budget, with spending increasing above inflation every year;

- The defence budget will get a £2.2bn boost for next year, paving the way for spending eventually hitting 2.5% of GDP;

- House building will hit a 40-year-high thanks to Labour’s planning reforms.

The chancellor confirmed that a voluntary redundancy scheme is set to launch for civil servants as part of her mission to “make government leaner”. She said this will deliver £3.5bn in “day-to-day savings by 2029-30”.

Ed Conway examines chancellor’s numbers

Political reaction

Shortly afterwards, Conservative leader Kemi Badenoch accused Labour of financial “chaos”.

She said the spring statement was “all smoke and mirrors”, adding: “I remember the last budget when Rachel Reeves said she was smashing glass ceilings, now it feels like the roof is falling over all our heads.”

A handful of Labour MPs were unimpressed with the moves around welfare, with Debbie Abrahams – the MP for Oldham East and Saddleworth – claiming “all the evidence points to cuts in welfare leading to severe poverty and worsened health conditions”.

An impact assessment into Labour’s welfare reforms, which include narrowing the eligibility criteria for personal independence payments (PIP), found there could be an additional 250,000 people in “relative poverty” by 2030 due to the changes.

Richard Burgon, the Labour MP for Leeds East, said “taking away the personal independence payments” from disabled people is an “especially cruel choice”.

New Hampshire has approved the issuance of a $100 million municipal bond backed by Bitcoin, in what appears to be the first structure of its kind at the US state level.

Minutes from a Nov. 17 meeting of the New Hampshire Business Finance Authority (BFA), the state’s business financing agency, show the board planned “to consider approving a resolution authorizing up to $100,000,000 bonds for a project to acquire and hold digital currency.”

Minutes from the following day record that directors voted to “approve the preliminary official intent, with no reservation, to issue a taxable conduit revenue bond for WaveRose Depositor, LLC of up to $100,000,000.”

According to a Wednesday Crypto in America report, the bond is backed by Bitcoin (BTC) and would let companies borrow against overcollateralized BTC held by a private custodian. The state or taxpayers do not back the bond; instead, BFA approves and oversees a private deal, while Bitcoin — reportedly held in custody by BitGo — covers investors.

According to the report, asset manager Wave Digital Assets and bond specialist Rosemawr Management designed the bond to utilize Bitcoin as collateral under the same rules that govern municipal and corporate bonds. Wave co-founder Les Borsai said the goal is to “bridge traditional fixed income with digital assets” for institutional investors.

Related: New Hampshire, North Dakota introduce bills for Strategic Bitcoin Reserve

“We believe this structure shows how public and private sectors can collaborate to responsibly unlock the value of digital assets and digital asset reserves,” he added.

The borrower is expected to post approximately 160% of the bond’s value in Bitcoin as collateral, and if the price of BTC drops below roughly 130%, a liquidation would ensure that bondholders stay whole. According to BFA Executive Director James Key-Wallace, fees from the transaction will fund the local innovation and entrepreneurship program, the Bitcoin Economic Development Fund.

New Hampshire dives headfirst into crypto

The news follows New Hampshire becoming the first US state to allow its government to invest in cryptocurrencies in May after Governor Kelly Ayotte signed a bill allowing the municipality to “invest in cryptocurrency and precious metals.”

Related: US won’t start Bitcoin reserve until other countries do: Mike Alfred

New Hampshire is also working on a bill to deregulate local cryptocurrency mining operations. In late October, a committee voted 4–2 to send the measure for further review in an interim study after it had been deadlocked in the State Senate twice.

The local administration is viewed as particularly welcoming to the cryptocurrency industry. In early February, Brendan Cochrane, an Anti-Money Laundering specialist at YK Law in New York City, argued that it could become an alternative for crypto companies relocating to the Bahamas.

The latest moves build on a longer history of crypto engagement. Back in 2015, New Hampshire was already working on a bill that would have allowed the state government to accept tax and fee payments in Bitcoin.

The bill ultimately failed in 2016, but it shows how early the local administration began to show interest in this asset class. Additionally, as early as 2016, some advocates were already arguing that New Hampshire was among the world’s most Bitcoin-friendly communities.

Magazine: Quitting Trump’s top crypto job wasn’t easy: Bo Hines

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024