‘We will do better.’ Microsoft CEO Nadella admits company has to rebuild trust with employees

Microsoft CEO Satya Nadella departs following a meeting of the White House Task Force on AI Education in the East Room of the White House in Washington on Sept. 4, 2025.

Eric Lee | Bloomberg | Getty Images

Microsoft CEO Satya Nadella told employees in a meeting on Thursday that the company has work to do to smooth relations with employees after announcing several rounds of layoffs and a mandated partial return to in-person work.

In the meeting that was held online, an employee asked executives to speak about a perceived lack of empathy in the company’s culture as of late and steps Microsoft is taking to rebuild trust with its workforce.

“I deeply appreciate that, the question and the sentiment behind it,” Nadella said, in audio that was obtained by CNBC. “I take it as feedback for me and everyone in the leadership team, because at the end of the day, I think we can do better, and we will do better.”

Nadella’s comments come after Microsoft slashed 9,000 jobs in July, following smaller reductions in the months prior. On Tuesday, Microsoft said workers living near its headquarters in Redmond, Washington, must come into the office three days a week, starting in February, with a broader rollout to follow.

Amy Coleman, Microsoft’s human resources chief, said at Thursday’s meeting that reception to the return-to-office announcement has been mixed, with some workers feeling like they’re losing autonomy. But she said that employees in and around Seattle already come in, on average, 2.4 times each week.

Like most of the tech industry, Microsoft went fully remote during the pandemic, and made particular use of its internal Teams video and chat offerings, which gained rapid adoption during that period. Microsoft has been slower than many of its peers to put a mandate in place for coming back to the office. Amazon, one of Microsoft’s top rivals, called employees back to offices five days a week in January.

While Nadella and the executive team are taking criticism from some staffers, Wall Street is applauding the company’s growth and execution. The stock is up almost 20% this year, outperforming the broader market, pushing Microsoft’s market cap to $3.7 trillion, which trails only Nvidia among the world’s most-valuable companies.

In July, Microsoft reported a 24% increase in net income to $27 billion. The company’s gross margin was under 69%, compared with 71% in late 2023. It’s rapidly building and renting data center infrastructure to meet artificial intelligence demand.

Nadella said at the meeting that with remote work, new employees and those who are early in their careers don’t always feel a sense of apprenticeship or mentorship.

“Management is just mostly all remote, but the interns are all, you know, in one location,” he said. “And so those are things that just will break a social contract.”

Microsoft didn’t immediately provide a comment.

Even with Microsoft’s rapid expansion, Nadella said the company is feeling the pressure. It’s a common theme in the software industry, as concerns proliferate about the impact of AI and its potential to automate work.

“We have some very, very hard work ahead of us, and that hard process of renewal is essentially what we have to do,” Nadella said. “You have to be hardcore in terms of an intellectual honesty about what really needs to happen.”

Microsoft’s Azure cloud business grew 39% in the latest quarter, but revenue in the Windows and devices business increased by just 2.5%.

“Some of the biggest businesses we built may not be as relevant going forward,” Nadella said. “Some of the margin that we love today may not be there tomorrow, and that means you have to be way ahead of all of those going away, right?”

Microsoft, which celebrated its 50th anniversary in April, will retain its core values as it confronts market realities, Nadella said.

“Capital markets have one simple truth,” he said. “There is no permission for any company to exist forever.”

That wasn’t the only contentious topic at the meeting.

Employees are awaiting details from a third-party investigation after The Guardian said in August that Israel’s military used Microsoft’s Azure cloud infrastructure to store Palestinians’ phone calls as part of Israel’s invasion of Gaza. Microsoft has fired five employees following protests at its headquarters in Redmond, according to a statement from the group No Azure for Apartheid.

Microsoft President Brad Smith, whose office the protesters entered, addressed the issue on Thursday. He said that he and Coleman met with Jewish Microsoft employees, who have been harassed and threatened and have seen their public information shared online.

“We don’t get to control what happens outside Microsoft, but we need to be clear about one thing,” Smith said. “There is no room for antisemitism at Microsoft, and as a company and as a community, we will protect this group and defend them from that.”

WATCH: Nebius Co-Founder: $17.4B Microsoft deal highlights surging AI infrastructure demand

Gemini Co-founders Tyler Winklevoss and Cameron Winklevoss attend the company’s IPO at the Nasdaq MarketSite in New York City, U.S., Sept. 12, 2025.

Jeenah Moon | Reuters

Shares of Gemini Space Station soared more than 40% on Thursday after the exchange operator raised $425 million in an initial public offering.

The stock opened at $37.01 on the Nasdaq after its IPO priced at $28. At one point, shares traded as high as $40.71.

The New York-based company priced its IPO late Thursday above this week’s expected range of $24 to $26, and an initial range of between $17 and $19. That valued the company at some $3.3 billion before trading began.

Gemini, which primarily operates as a cryptocurrency exchange, was founded by the Winklevoss brothers in 2014 and held more than $21 billion of assets on its platform as of the end of July. Per its registration with the Securities and Exchange Commission, Gemini posted a net loss of $159 million in 2024, and in the first half of this year, it lost $283 million.

The company also offers a U.S. dollar-backed stablecoin, credit cards with a crypto-back rewards program and a custody service for institutions.

The Winklevoss brothers were among the earliest bitcoin investors and first bitcoin billionaires. They have long held that bitcoin is a superior store of value than gold. On Friday morning, they told CNBC’s “Squawk Box” they see its price reaching $1 million a decade from now.

In 2013, they were the first to apply to launch a bitcoin exchange-traded fund, more than 10 years before the first bitcoin ETFs would eventually be approved. The Securities and Exchange Commission’s rejection of the application, which cited risk of fraud and market manipulation, set the stage for the bitcoin ETF debate in the years to come.

Even in the early days, when bitcoin was notorious for its extreme volatility and anti-establishment roots and shunned by Wall Street, the Winklevoss brothers were outspoken about the need for smart regulation that would establish rules for the crypto-led financial revolution.

(Learn the best 2026 strategies from inside the NYSE with Josh Brown and others at CNBC PRO Live. Tickets and info here.)

Opendoor co-founder and newly minted board chair Keith Rabois said remote work and a “bloated” workforce have been a drag on the company’s culture, as he vowed to slash headcount.

“There’s 1,400 employees at Opendoor. I don’t know what most of them do. We don’t need more than 200 of them,” Rabois told CNBC’s “Squawk on the Street” on Friday.

The online real-estate platform on Wednesday appointed former Shopify executive Kaz Nejatian as its new CEO after investor pressure caused his predecessor, Carrie Wheeler, to resign last month. Opendoor also named Rabois as chairman and said Eric Wu, who served as the company’s first CEO before stepping down in 2023, would return to the board.

The announcement sent Opendoor shares soaring 78% on Thursday, before the stock slid more than 12% on Friday. It is still up almost 500% this year, after an army of retail investors pushed up the stock price when hedge fund manager Eric Jackson began touting the company.

Opendoor year-to-date stock chart.

Opendoor’s business involves using technology to buy and sell homes, pocketing the gains.

Nothing has fundamentally improved for the company since Jackson bought shares of Opendoor in July. Opendoor remains a cash-burning, low-margin business with meager near-term growth prospects.

Rabois said he has a “high level view of the strategy” that’s needed to transform Opendoor, and that the headcount reductions are necessary to resolve the company’s cash burn.

“The culture was broken,” Rabois said. “These people were working remotely. That doesn’t work. This company was founded on the principle of innovation and working together in person. We’re going to return to our roots.”

He added that Opendoor “went down this DEI path,” referring to diversity, equity and inclusion.

“We’re gonna fix all that,” Rabois said.

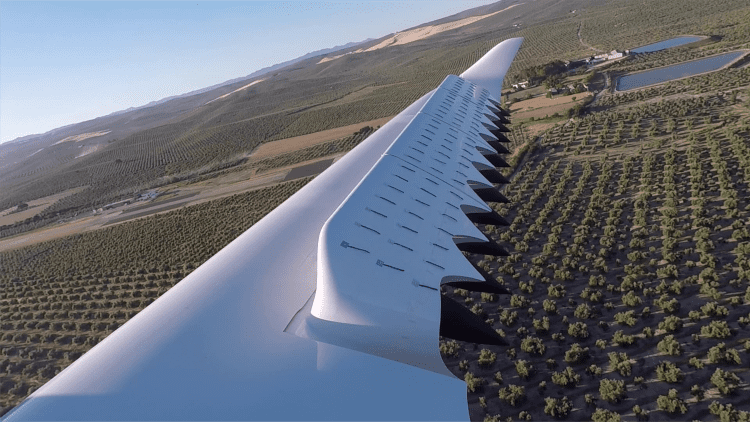

![]()

Courtesy: Archer Aviation

The Federal Aviation Administration said Friday it is launching a pilot program to speed up the rollout of air taxis.

Archer Aviation and Joby Aviation, major players in the electric vertical takeoff and landing, or eVTOL, space, said they are participating in the program. Shares of each were higher on Friday.

The program will establish at least five projects through public-private partnerships with state and local governments to promote safe usage of eVTOL aircraft.

“The next great technological revolution in aviation is here,” said U.S. Transportation Secretary Sean Duffy in a release. “The United States will lead the way, and doing so will cement America’s status as a global leader in transportation innovation.”

Archer said supervised trials could begin in the U.S. as soon as next year, ahead of FAA certification. Joby is set to begin FAA flight testing early next year.

The announcement follows President Donald Trump‘s executive order in June that included the creation of an eVTOL pilot program to foster safe development and deployment in the U.S.

Proponents of eVTOL have touted the technology as a method to slash emissions and ease traffic. Archer, Joby and their competitors have been steadily working toward FAA approval.

Joby called the program a “critical step” in the path toward widespread air taxi service in the U.S. Archer CEO Adam Goldstein dubbed the announcement a “landmark moment” that allows the company to work with partners such as United Airlines to trial aircraft.

“These early flights will help cement American leadership in advanced aviation and set the stage for scaled commercial operations in the U.S. and beyond,” he wrote.

Both companies have made strides testing their products through partnerships in the Middle East.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment11 months ago

Environment11 months agoHere are the best electric bikes you can buy at every price level in October 2024