Having sealed her chancellor’s fate, the markets could seal the prime minister’s fate

So farewell, then, Trussonomics.

The demise of the country’s second shortest-lived chancellor also brings with it the demise of the country’s shortest-lived economic movement.

Liz Truss came into office promising to boost the country’s growth rate through a forensic combination of tax cuts, reforms to the country’s supply side (for which read: things like planning reform) and spending restraint. This was, if you squint a little bit, not dissimilar to the kinds of policies espoused by Ronald Reagan and Margaret Thatcher.

Tory MPs turn on Truss as PM scrambles to save job after sacking chancellor – latest updates

It always looked risky – especially at such a fragile point for the global economy. We are coming to the end of a 12-year period of cheap money, something which is causing a near-nervous breakdown in financial markets. Central banks are in the process of raising interest rates and trying to feed the glut of bonds they bought during the financial crisis back in the market.

As if that weren’t enough, Europe is facing one of its bleakest economic winters in modern memory, with a war raging in Ukraine and energy prices touching historic highs. It is hard to think of many less auspicious periods to attempt an untested new economic manifesto.

Yet Ms Truss and her former chancellor Kwasi Kwarteng pushed on all the same. And unlike Thatcher, whose first few budgets were grisly austerity packages which no one much enjoyed, Ms Truss and Mr Kwarteng aimed to turn Thatcherism on its head. Instead of fixing the public finances first and then cutting taxes second, they opted to spend the fruits of economic growth before that growth had even been achieved.

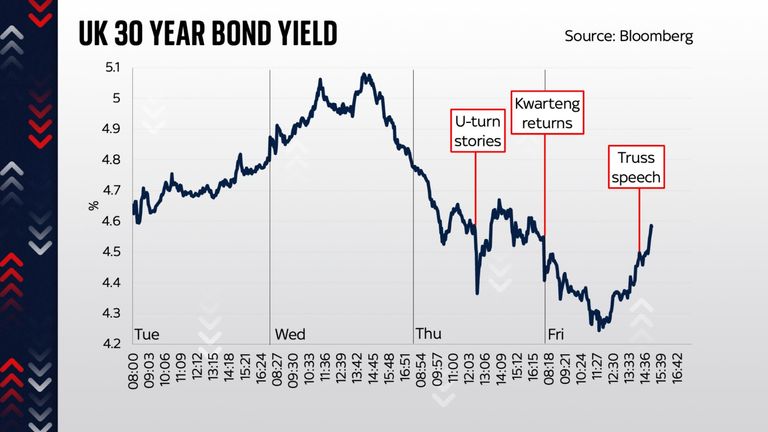

The mini-budget of 23 September was a small document with extraordinarily large consequences. Ironically, the more expensive the measures were, the less controversial they turned out to be. The scheme to cap household energy unit costs will potentially cost hundreds of billions of pounds, yet (and we know this because it was pre-announced long before the mini-budget) investors barely batted an eyelid. They carried on lending to this country at more or less the same or equivalent rates.

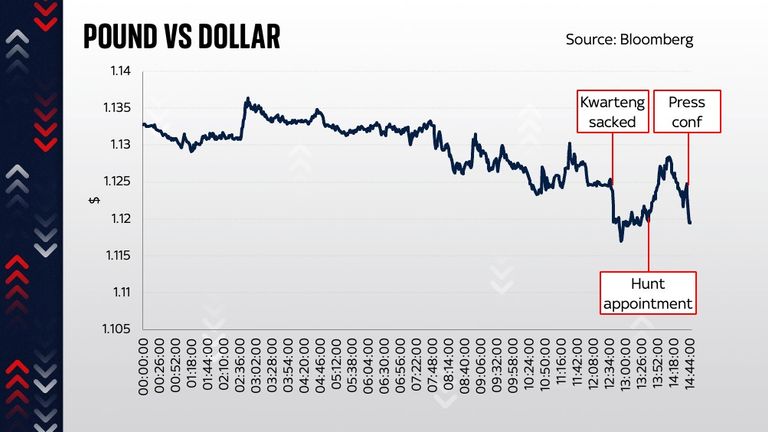

The same was not the case for the rest of the mini-budget’s policies. Shortly after they were announced – everything from the abolition of the 45p rate (actually quite cheap in fiscal terms) to the cancellation of Rishi Sunak’s corporation tax rise – markets began to lurch in what was, for Ms Truss, and most UK households, the wrong direction. The pound sank, the yields on government debt, which determine the interest rates across most of the economy, began to climb.

That was bad enough. When Mr Kwarteng announced gleefully a couple of days later on television that he had more tax cuts up his sleeve, the trot out of the country became a stampede. The pound fell, briefly, to the lowest level against the dollar in the history of, well, the dollar.

Even more worryingly, those interest rates on government bonds rose at an unprecedented rate, causing all sorts of malfunctions throughout the money markets.

The most obvious – and the one that perhaps will have the longest legacy – is the rise in mortgage rates. But the unexpected consequences were even more worrying, among them a crisis in funds used by pension schemes. That sparked a “run dynamic” which compelled the Bank of England to step in with an emergency support scheme.

Even at this point, we were into unprecedented territory. Never before had the Bank been forced to intervene quite like this. Never before had it had to do so as a result of a government’s Budget.

The intervention, however, had some success, bringing down the relevant interest rates and bringing markets back from the edge. But there was a sting in the tail: a deadline. Today, 14 October.

Analysis: PM’s new tax U-turn

In hindsight perhaps it’s obvious that this, then, would always have been the day when the government might face another existential crisis. Investors were always going to be nervous ahead of the Bank’s withdrawal from this neck of the bond market. And that is precisely what happened: after the governor reiterated, on a panel in Washington, that he was indeed serious, all eyes then turned to the chancellor. Could he say something to reassure markets?

In the event, the answer was: no. But something else changed matters: growing rumours of a U-turn. That brings us to this morning. The chancellor, pulled back from Washington early, was dismissed. The U-turn began. The corporation tax freeze is to be abandoned. The coming medium-term fiscal plan will involve austerity and a big dose of fiscal pain. The upshot is that Trussonomics, which was hinged clearly on tax cuts like these, is dead in the water.

However, the bigger question concerns what happens next. Those markets, which Ms Truss said explicitly were the reason for her U-turn, are still pretty frantic. No one knows how they’ll fare on Monday, but, whether right or wrong, another grisly day will almost certainly be seen as a sign of the government’s failure. And, having sealed the fate of her chancellor, the markets could well seal the fate of the prime minister.

But that’s a few days away – a long time in both politics and markets.

Liz Truss appoints Jeremy Hunt as chancellor. Pic: Andrew Parsons / No 10 Downing Street

In the meantime, here is something to dwell on: an alternative version of history. In a parallel universe, Ms Truss and Mr Kwarteng did things slightly less hastily. They decided their emergency Budget would simply deal with the energy price shock coming this winter. They promised an OBR statement and hatched plans for a growth-generating budget in a few months’ time.

In that parallel universe, interest rates probably wouldn’t have risen so high. The rises would, anyway, have been blamed on the Bank of England, not the government. The government would have enjoyed some kudos for having prevented energy-related penury this winter and made merry in their honeymoon. Things could have been oh-so different.

Click to subscribe to the Sky News Daily wherever you get your podcasts

Now, all of this is of course imponderable. But it does rather underline an important point: none of this was inevitable. This wasn’t a crisis like 1992 – where the UK faced monetary pressures suffered by nearly every other nation in Europe. It was simply a succession of very unfortunate decisions at precisely the wrong moment.

At a time of market turmoil and war in Europe, Ms Truss and Mr Kwarteng chose to take a gamble. It did not pay off.

:: The new chancellor, Jeremy Hunt, will talk to Sky News tomorrow morning. Tune in from 7am on Saturday.

The UK economy unexpectedly shrank in May, even after the worst of Donald Trump’s tariffs were paused, official figures showed.

A standard measure of economic growth, gross domestic product (GDP), contracted 0.1% in May, according to the Office for National Statistics (ONS).

Rather than a fall being anticipated, growth of 0.1% was forecast by economists polled by Reuters as big falls in production and construction were seen.

It followed a 0.3% contraction in April, when Mr Trump announced his country-specific tariffs and sparked a global trade war.

A 90-day pause on these import taxes, which has been extended, allowed more normality to resume.

This was borne out by other figures released by the ONS on Friday.

Exports to the United States rose £300m but “remained relatively low” following a “substantial decrease” in April, the data said.

Overall, there was a “large rise in goods imports and a fall in goods exports”.

A ‘disappointing’ but mixed picture

It’s “disappointing” news, Chancellor Rachel Reeves said. She and the government as a whole have repeatedly said growing the economy was their number one priority.

“I am determined to kickstart economic growth and deliver on that promise”, she added.

But the picture was not all bad.

Growth recorded in March was revised upwards, further indicating that companies invested to prepare for tariffs. Rather than GDP of 0.2%, the ONS said on Friday the figure was actually 0.4%.

It showed businesses moved forward activity to be ready for the extra taxes. Businesses were hit with higher employer national insurance contributions in April.

Read more:

Trump plans to hit Canada with 35% tariff – warning of blanket hike for other countries

Woman and three teenagers arrested over M&S, Co-op and Harrods cyber attacks

The expansion in March means the economy still grew when the three months are looked at together.

While an interest rate cut in August had already been expected, investors upped their bets of a 0.25 percentage point fall in the Bank of England’s base interest rate.

Such a cut would bring down the rate to 4% and make borrowing cheaper.

Is Britain going bankrupt?

Analysts from economic research firm Pantheon Macro said the data was not as bad as it looked.

“The size of the manufacturing drop looks erratic to us and should partly unwind… There are signs that GDP growth can rebound in June”, said Pantheon’s chief UK economist, Rob Wood.

Why did the economy shrink?

The drops in manufacturing came mostly due to slowed car-making, less oil and gas extraction and the pharmaceutical industry.

The fall was not larger because the services industry – the largest part of the economy – expanded, with law firms and computer programmers having a good month.

It made up for a “very weak” month for retailers, the ONS said.

Monthly Gross Domestic Product (GDP) figures are volatile and, on their own, don’t tell us much.

However, the picture emerging a year since the election of the Labour government is not hugely comforting.

This is a government that promised to turbocharge economic growth, the key to improving livelihoods and the public finances. Instead, the economy is mainly flatlining.

Output shrank in May by 0.1%. That followed a 0.3% drop in April.

Ministers were celebrating a few months ago as data showed the economy grew by 0.7% in the first quarter.

Hangover from artificial growth

However, the subsequent data has shown us that much of that growth was artificial, with businesses racing to get orders out of the door to beat the possible introduction of tariffs. Property transactions were also brought forward to beat stamp duty changes.

Read more:

Trump to hit Canada with 35% tariff

Woman and three teens arrested over cyber attacks

In April, we experienced the hangover as orders and industrial output dropped. Services also struggled as demand for legal and conveyancing services dropped after the stamp duty changes.

Many of those distortions have now been smoothed out, but the manufacturing sector still struggled in May.

Signs of recovery

Manufacturing output fell by 1% in May, but more up-to-date data suggests the sector is recovering.

“We expect both cars and pharma output to improve as the UK-US trade deal comes into force and the volatility unwinds,” economists at Pantheon Macroeconomics said.

Meanwhile, the services sector eked out growth of 0.1%.

A 2.7% month-to-month fall in retail sales suppressed growth in the sector, but that should improve with hot weather likely to boost demand at restaurants and pubs.

Struggles ahead

It is unlikely, however, to massively shift the dial for the economy, the kind of shift the Labour government has promised and needs in order to give it some breathing room against its fiscal rules.

The economy remains fragile, and there are risks and traps lurking around the corner.

Is Britain going bankrupt?

Concerns that the chancellor, Rachel Reeves, is considering tax hikes could weigh on consumer confidence, at a time when businesses are already scaling back hiring because of national insurance tax hikes.

Inflation is also expected to climb in the second half of the year, further weighing on consumers and businesses.

Business

Government to announce new scheme as it ramps up AI adoption with backing from Facebook owner Meta

The government is speeding up its adoption of AI to try and encourage economic growth – with backing from Facebook parent Meta.

It will today announce a $1m (£740,000) scheme to hire up to 10 AI “experts” to help with the adoption of the technology.

Sir Keir Starmer has spoken repeatedly about wanting to use the developing technology as part of his “plan for change” to improve the UK – with claims it could produce tens of billions in savings and efficiencies.

Politics live: Follow the latest updates

The government is hoping the new hires could help with problems like translating classified documents en masse, speeding up planning applications or help with emergency responses when power or internet outages occur.

The funding for the roles is coming from Meta, through the Alan Turing Institute. Adverts will go live next week, with the new fellowships expected to start at the beginning of 2026.

Technology Secretary Peter Kyle said: “This fellowship is the best of AI in action – open, practical, and built for public good. It’s about delivery, not just ideas – creating real tools that help government work better for people.”

He added: “The fellowship will help scale that kind of impact across government, and develop sovereign capabilities where the UK must lead, like national security and critical infrastructure.”

The projects will all be based on open source models, meaning there will be a minimal cost for the government when it comes to licensing.

Meta describes its own AI model, Llama, as open source, although there are questions around whether it truly qualifies for that title due to parts of its code base not being published.

The owner of Facebook has also sponsored several studies into the benefits of government adopting more open source AI tools.

Minister reveals how AI could improve public services

Read more:

UK to be AI ‘maker not taker’ – PM

Govt AI adviser stands down

Mr Kyle’s Department for Science and Technology has been working on its mission to increase the uptake of AI within government, including through the artificial intelligence “incubator”, under which these fellowships will fall.

The secretary of state has pointed to the success of Caddy – a tool that helps call centre workers search for answers in official documents faster – and its expanding use across government as an example of an AI success story.

He said the tool, developed with Citizens Advice, shows how AI can “boost productivity, improve decision-making, and support frontline staff”. A trial suggested it could cut waiting times for calls in half.

My Kyle also recently announced a deal with Google to provide tech support to government and assist with modernisation of data.

👉Listen to Politics at Sam and Anne’s on your podcast app👈

Joel Kaplan, the chief global affairs officer from Meta, said: “Open-source AI models are helping researchers and developers make major scientific and medical breakthroughs, and they have the potential to transform the delivery of public services too.

“This partnership with ATI will help the government access some of the brightest minds and the technology they need to solve big challenges – and to do it openly and in the public interest.”

Jean Innes, the head of the Alan Turing Institute, said: “These fellowships will offer an innovative way to match AI experts with the real world challenges our public services are facing.”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike