Why is Rishi Sunak casting such a sombre mood? It’s more about politics than economics

Rishi Sunak says we are facing a “profound economic crisis”. Big words, not to mention depressing. But do they really stack up?

Is the UK really facing something unique? Can he really blame much of it (as was implicit in his speech) on his predecessor? Or is something else going on?

Let’s start at the start.

There is no doubt that the UK is facing tough economic times right now. We are quite plausibly in the teeth of a recession. Look at measures like the purchasing manager’s index from S&P Global – a measure of how businesses are faring right now – and it is contraction territory. This is a recession warning, and no mistake.

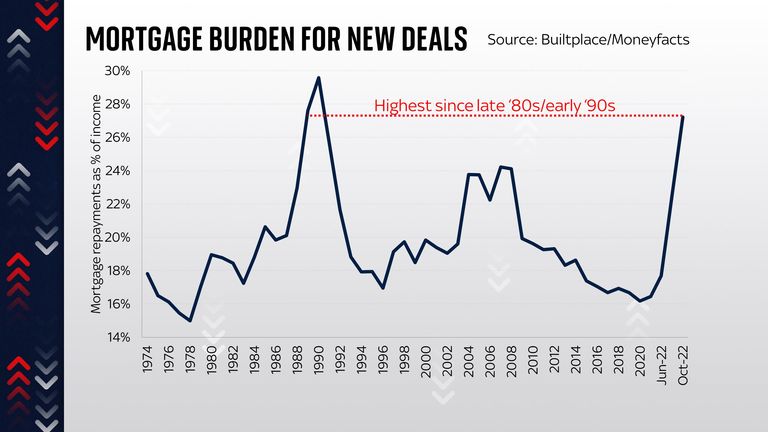

And there are certainly some factors which will make this a grim year or two for households. For one thing, mortgage costs are rising, and rising fast. The average two-year fixed rate mortgage is currently up above 6%, a level which implies the highest repayments as a percentage of household incomes since the late 1980s or early 1990s. This is clearly not good news.

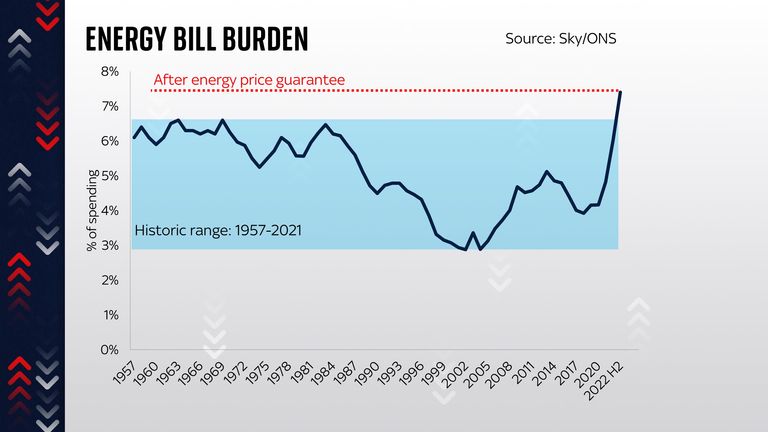

And it’s a similar story for energy bills. Even after you account for the energy price guarantee introduced by Liz Truss, the amount the average household spends on energy this winter will still be the highest we’ve seen since at least the 1950s. Again, not good news – and note that since the scheme has been shortened from two years to six months, it’s quite plausible the costs are even greater next year.

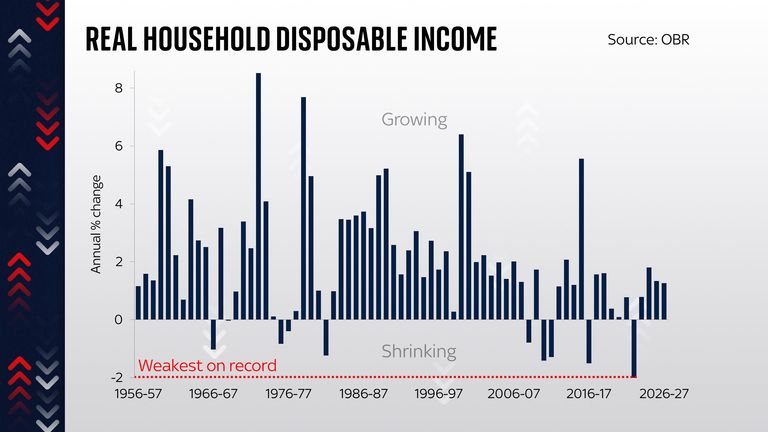

Put it all together and any measure of our collective standard of living suggests an astonishing fall this year. We are all going to be much poorer, relative to what we typically want to spend our money on. And that, in large part, is down to the impact of higher energy prices, which creep into every part of our lives.

But these are not the only issues facing the government.

The UK is not the only major economy facing a potential recession

One problem which no previous prime minister has been able to address successfully is Britain’s productivity malaise. Output per hour is perhaps the single most important yardstick of our economic wellbeing and it has essentially flatlined since the financial crisis, making (and this is not an exaggeration) everything worse: our incomes, our quality of life, the level of taxes and national debt.

And this is before you consider the deeper issues facing the global economy right now. Most glaringly we seem to be in the early stages of a new Cold War, which could result in the creation of trading blocs rather than a fully globalised world. And this prognosis is, frankly, more optimistic than many. This will have enormous economic implications.

But here’s the thing. None of these challenges are necessarily Britain’s alone. The UK is not the only major economy facing a potential recession: others in Europe will probably have even deeper contractions this winter. Disappointing productivity is something many developed economies struggle with. Interest rates are rising everywhere (even if the UK’s recent increase in borrowing costs outpaced other nations).

Many of the current problems pre-date Liz Truss

Nor is it especially fair to blame all these problems on Liz Truss: they pretty much all pre-date her. And here’s the really interesting thing: the spike in government bond yields which followed her and Kwasi Kwarteng’s mini-budget has now been almost completely erased.

Those gilt yields are now nearly back to where they were before. So too are expectations for Bank of England interest rates next year. This is an extraordinary turnaround – a consequence of the fact that the Truss government is no more.

But it means that actually much of the damage has now been erased. It’s worth pondering this for a moment. Remember: that rise in gilt yields as international investors looked askance at the UK pushed up the potential cost of borrowing both for households and for governments. It meant that if the government carried on having to issue debt at those kinds of interest rates then its debt interest bill would have been a lot higher. The IFS calculated the ongoing cost at about £10 billion a year. That’s a big deal.

‘Credibility premium’ on government debt is shrinking

But now that the “credibility premium” on government debt is shrinking, that problem is no longer, well, a problem. It may soon have disappeared altogether.

Which raises a question: why did Rishi Sunak try to cast such a sombre mood on the steps of Downing Street? My suspicion is that it’s about 60% politics and about 40% economics.

The politics first: if he can convince the public (and his MPs) that things are grim, it means less resistance for the inevitable cuts. Much as Covid united the party, perhaps, he thinks, the threat of economic contagion could do something similar.

If he can persuade the public that the bad news he’s meting out is down to Liz Truss rather than his own policies as chancellor (most of these problems were problems when he was in Downing Street and had responsibility for doing something about them) then, well, that would obviously suit him. Even if it’s not entirely accurate.

Sunak’s warnings are only 40% economics

The 40% economics is intriguing, because there’s a virtuous circle here. If he can deploy phrases like “profound economic crisis” and “difficult decisions” he can persuade markets that he’s really serious about cutting debt, which in turn should push down gilt yields even lower. Which means the hole in the public finances suddenly gets smaller too.

Talking tough could actually mean he doesn’t have to act quite so tough in the coming austerity mini-budget or whatever we’ll call it.

Not that much of this will be detectable when the fiscal statement lands. We are clearly in for some tough cuts for the economy. But most of the challenges they are intended to address were baked in long before Liz Truss ever reached Downing Street.

Business

Basic questions unanswered by Shein at Business and Trade Committee despite firm eyeing London listing

A representative for one of the world’s biggest fast fashion retailers, Shein was unable to answer questions from MPs over where it sources its cotton from.

Shein’s general counsel for Europe Middle East Africa (EMEA) Yinan Zhu was asked if the company sells products containing cotton from China, mainly the region of Xinjiang, where China has been accused of subjecting members of the Uyghur ethnic group to forced labour.

Speaking at the Business and Trade Committee, Ms Zhu was asked several times whether the company uses cotton supplied from China.

After being pressed on the matter, she said she would have to write to the committee with an answer.

She said: “For detailed operational information and other aspects, I am not able to assist. I will have to write back to the committee afterwards.”

She added: “Obviously, we comply with laws and regulations everywhere we do business in the role. And we have supplier code of conducts, we have robust systems and procedures in place and policies in place.

“We also have very strong enforcement measures in place to ensure we adhere to these standards that are expected in our supply chain.”

Read more

UK long-term borrowing costs highest this century

Rising evidence of price hike threat as Next is latest to warn of challenges

When asked if the company believed forced labour took place in Xinjiang, Ms Zhu reminded MPs of the “agenda of the committee, as I understand it, we’re looking at upholding standards”, before adding: “I’m only able to answer the questions that are relating to our business.”

Shein was founded in China in 2012 and is now a leader in fast fashion, shipping to 150 countries.

Committee chairman Liam Byrne challenged Ms Zhu, but she repeated she would have to write to the committee afterwards.

Mr Byrne said the parliamentary committee was “horrified” by the lack of information provided and said Zhu’s statements gave lawmakers “zero confidence” in the integrity of Shein’s supply chains.

“The reluctance to answer basic questions has frankly bordered on contempt,” Mr Byrne said.

The top lawyer’s responses were said to be “ridiculous” and “very unhelpful and disrespectful” by committee member Charlie Maynard.

Shein listing would ‘wake up London capital markets’

When Ms Zhu said she was answering to the best of her ability, the Lib Dem MP said: “That is simply not true. We’ve asked you some very, very, very simple questions and you are not giving us straight answers.”

Ms Zhu also said she was unable to say anything about reports the online giant was preparing to list as a public company on the London Stock Exchange.

Sky News reported exclusively in June that Shein had prepared to file a prospectus with the Financial Conduct Authority for approval ahead of a potential float on the exchange.

But when asked on Tuesday if this was true, and why the company had stopped pursuing a New York Stock Exchange float, Ms Zhu said she was unable to comment on any IPO (initial public offering) speculation as it was not her remit.

UK long-term borrowing costs have hit their highest level since 1998.

The unwanted milestone for the Treasury’s coffers was reached ahead of an auction of 30-year bonds, known as gilts, this morning.

The yield – the effective interest rate demanded by investors to hold UK public debt – peaked at 5.21%.

At that level, it is even above the yield seen in the wake of the mini-budget backlash of 2022 when financial markets baulked at the Truss government’s growth agenda which contained no independent scrutiny from the Office for Budget Responsibility.

Money latest: Do I need to pay five-year old parking fine?

The premium is up, market analysts say, because of growing concerns the Bank of England will struggle to cut interest rates this year.

Just two cuts are currently priced in for 2025 as investors fear policymakers’ hands could be tied by a growing threat of stagflation.

The jargon essentially covers a scenario when an economy is flatlining at a time of rising unemployment and inflation.

Growth has ground to a halt, official data and private surveys have shown, since the second half of last year.

Critics of the government have accused Sir Keir Starmer and his chancellor, Rachel Reeves, of talking down the economy since taking office in July amid their claims of needing to fix a “£22bn black hole” in the public finances.

Chancellor reacts to inflation rise

Both warned of a tough budget ahead. That first fiscal statement put businesses and the wealthy on the hook for £40bn of tax rises.

Corporate lobby groups have since warned of a hit to investment, pay growth and jobs to help offset the additional costs.

At the same time, consumer spending has remained constrained amid stubborn price growth elements in the economy.

UK economy showed no growth

Read more:

Growing threat to finances from rising bills

Why UK energy bills could rise further this year

Higher borrowing costs also reflect a rising risk premium globally linked to the looming return of Donald Trump as US president and his threats of universal trade tariffs.

The higher borrowing bill will pose a problem for Ms Reeves as she seeks to borrow more to finance higher public investment and spending.

Tuesday’s auction saw the Debt Management Office sell £2.25bn of 30-year gilts to investors at an average yield of 5.198%.

It was the highest yield for a 30-year gilt since its first auction in May 1998, Refinitiv data showed.

This extra borrowing could mean Ms Reeves is at risk of breaking the spending rules she created for herself, to bring down debt, and so she may have less money to spend, analysts at Capital Economics said.

“There is a significant chance that the Office for Budget Responsibility (OBR) will judge that the Chancellor Rachel Reeves is on course to miss her main fiscal rule when it revises its forecasts on 26 March. To maintain fiscal credibility, this may mean that Ms Reeves is forced to tighten fiscal policy further,” said Ruth Gregory, the deputy chief UK economist at Capital Economics.

-

Sports2 years ago

Sports2 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports9 months ago

Sports9 months agoStory injured on diving stop, exits Red Sox game

-

Sports1 year ago

Sports1 year agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports3 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike

-

Business2 years ago

Business2 years agoBank of England’s extraordinary response to government policy is almost unthinkable | Ed Conway