Next two years will be ‘challenging’, says Chancellor Jeremy Hunt – as disposable incomes are set to fall to record lowest level

The UK’s economic outlook will be “challenging” for the next two years, Jeremy Hunt says.

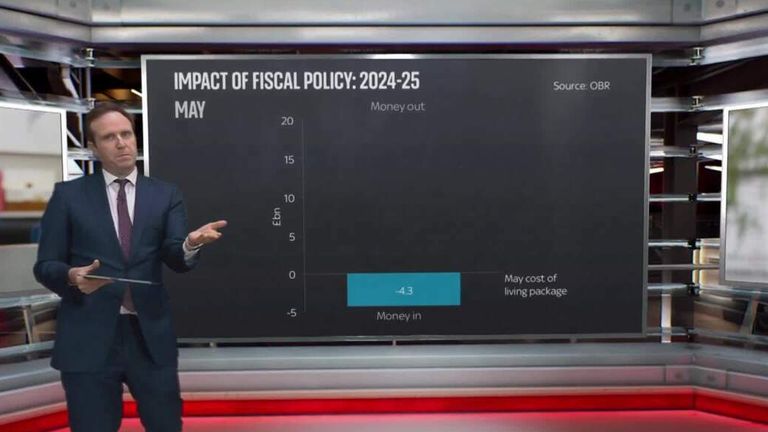

The chancellor presented his autumn statement to parliament on Thursday, littered with stealth taxes and curbs on government spending amounting to £55bn in an attempt to plug the black hole in the public finances.

But the independent Office for Budget Responsibility (OBR) warned the disposable incomes of UK households would fall by 7.1% over the next two years – the lowest level since records began in 1956/7, and taking incomes down to 2013 levels.

Politics live: Tax burden reaches highest level since WWII

Speaking to Sky News, Mr Hunt said it was “a difficult time for everyone” but tax hikes and spending cuts are needed to get the economy “on an even keel”.

“Over the next two years it is going to be challenging,” he said.

“But I think people want a government that is taking difficult decisions, has a plan that will bring down inflation, stop those big rises in the cost of energy bills and the weekly shop, and at the same time is taking measures to get through this difficult period.”

The chancellor insisted that his autumn statement is a “very Conservative package” following criticism from some Tory MPs.

“The Office for Budgetary Responsibility said yesterday that what we’re doing is actually recession shallow, it’s saving jobs,” he said.

“But what I would say to my Conservative colleagues is there is nothing Conservative about spending money that you haven’t got, there is nothing Conservative about not tackling inflation, there is nothing Conservative about ducking difficult decisions that put the economy on track.

“And we’ve done all of those things and that is why this is a very Conservative package to make sure we sort out the economy.

“None of this is easy, but it’s the right thing to do.”

Former business secretary Jacob Rees-Mogg accused the chancellor of taking the “easy option” in Thursday’s autumn statement rather than bearing down harder on public spending.

He said the country needed lower taxes to drive up growth.

Hunt questioned over autumn statement

Probed on how it can be fair that pensions will go up by inflation when public sector workers will not see pay increase alongside prices, Mr Hunt said the elderly do not have the ability to work more to improve their take home pay.

“Well, I think the truth is, first of all, pensioners have retired. They don’t have the ability to work more or work longer hours in the way that people of working age do,” the chancellor said.

“But I think it is wrong to say that only the poorest pensioners are feeling the squeeze at the moment.

“I think this is something that’s affecting everyone and I think it’s right.

“Having made that promise to pensioners in our manifesto that we would have this triple lock, I think this is exactly the kind of tough time that people want it to kick in.

“And so that’s why I think it’s the right thing to do.”

The chancellor added: “We’re not pretending that this isn’t going to be a difficult time for everyone. But what we have is a plan.”

’12 weeks of Conservative chaos’ – Rachel Reeves

In yesterday’s autumn statement, Mr Hunt announced economic policies which the government hopes will help to rebalance the nation’s finances after the economic turmoil which followed former chancellor Kwasi Kwarteng’s mini-budget.

These included:

• Income tax thresholds being frozen for two more years until April 2028

• Top level of income tax now being paid on earnings over £125,140 instead of £150,000

• Pensions triple lock will remain – with pensioners to see a 10.1% increase in weekly payments in line with inflation

• Benefits to also rise in line with inflation – by 10.1%

• Energy cap to rise from £3,000 a year to £2,500 a year beyond April

• UK minimum wage to rise from £9.50 to £10.42 an hour for those aged over 23

• Windfall tax on oil giants’ profits to rise from 25% to 35% and be extended by two years until March 2028

• Additional cost of living payments of £900 for those on benefits and £300 for pensioners

• Spending on public services in England to rise slower than planned

Click to subscribe to the Sky News Daily wherever you get your podcasts

As a result of Mr Hunt’s announcements, the tax burden in the UK will also now be at its highest since the Second World War, and there are stark warnings about increased bills and higher unemployment as the recession takes hold – as well as predictions the economy will still shrink 1.4% in 2023.

But most of the difficult decisions on spending have been postponed until after the next general election, due in 2024.

Treasury analysis suggests around 55% of households will be worse off as a result of the measures.

Read more: Jeremy Hunt’s autumn statement had all the hallmarks of a Labour budget

Labour has blamed “12 weeks of Conservative chaos” and “12 years of Conservative economic failure” for the bleak outlook.

Shadow chancellor Rachel Reeves accused the government of forcing the UK economy into a “doom loop where low growth leads to higher taxes, lower investments and squeezed wages, with the running down of public services”.

Ms Reeves told Sky News she is “really worried about what’s going to happen to people’s living standards next year from April” and said a Labour government would have done more “to alleviate some of that pressure on the ordinary working person”.

What does the autumn statement mean?

As Mr Hunt took part in the broadcast round Friday morning, economic think-tank the Resolution Foundation published analysis suggesting his autumn statement’s tax rises would deliver a 3.7% income hit to typical households.

The foundation said the statement had piled further pressure on the “squeezed middle” and that the focus on “stealthy” tax threshold freezes to raise revenue would extend far beyond high earners.

The think tank also found that the budget would reverse much of the government’s levelling up agenda.

“The £15 billion of cuts to capital investment announced yesterday will undo 80% of the remaining increases in public investment announced by previous chancellor Rishi Sunak, which underpinned the levelling-up agenda,” it said.

Tens of thousands of Vodafone users are reporting problems with their internet

The outages began on Monday afternoon, according to the monitoring website DownDetector, which reported more than 130,000 issues with Vodafone connections.

A spokeswoman for the company said: “We are aware of a major issue on our network currently affecting broadband, 4G and 5G services.

“We appreciate our customers’ patience while we work to resolve this as soon as possible.”

The company has more than 18 million UK customers, with nearly 700,000 of those using Vodafone’s home broadband connection.

Vodafone users vented their frustration on social media.

“It’s like Vodafone has just been wiped off the earth. Not a single thing works,” said one X user.

Vodafone users were shown an error message when trying to access the internet provider’s app

The Vodafone app also appeared to be down for users, with the company’s website briefly going down too.

The ‘network status checker’ on the website was also down, and when Sky News tried to test the customer helpline, it did not ring.

“There’s Vodafone down and then there’s Vodafone wiped off the face of the f***ing planet,” posted another X user.

Read more from Sky News:

Gaza deal latest: Drones reveal devastation

Madagascar president says coup under way

Jake Moore, global cybersecurity advisor at ESET, said the outage shows how reliant we are on modern infrastructure like mobile networks.

“Outages will always naturally raise early suspicions of a potential cyber incident, though current evidence points more towards an internal network failure than a confirmed attack,” said Mr Moore.

“The sudden outage, combined with the inability to access customer service lines, mirrors classic symptoms of a distributed denial-of-service (DDoS) attack, where attackers overwhelm the network so the site or systems collapse.

“However, malicious or not, this once again highlights our heavy reliance on digital infrastructure, especially in an age where we increasingly depend on mobile networks for everything,” he said.

“Ultimately, resilience is essential, whether the cause is a direct cyberattack, a supply chain issue or a critical internal error.”

Lloyds Banking Group has set aside a further £800m to cover estimated costs associated with the car finance mis-selling scandal.

The bank said the sum took its total provision to £1.95bn.

It had been assessing the impact since the Financial Conduct Authority (FCA) revealed last week it was consulting on a compensation scheme, with up to 14.2 million car finance agreements potentially eligible for payouts.

The regulator had previously found that many lenders failed to disclose commission paid to brokers, which could have led to customers paying more than they should have between April 2007 and November 2024.

Money latest: How much a private investigator costs

Eligible customers could receive an average of £700 each under the proposals.

Lloyds said on Monday that it would be contributing to the consultation to argue a number of points.

It said: “The Group remains committed to ensuring customers receive appropriate redress where they suffered loss, however the Group does not believe that the proposed redress methodology outlined in the consultation document reflects the actual loss to the customer. Nor does it meet the objective of ensuring that consumers are compensated proportionately and reasonably where harm has been demonstrated.

“In addition, the approach to unfairness in the redress scheme does not align with the legal clarity provided by the recent Supreme Court judgment in Johnson, in which unfairness was assessed on a fact specific basis and against a non-exhaustive list of multiple factors. The Group will make representations to the FCA accordingly.”

Car finance: ‘Don’t use a claims firm – here’s why’

Shares in Lloyds, which fell last week when the bank warned of a potential “material” increase in its provisions, gained more than 0.5% on Monday.

The estimated compensation figure came in below the sum some financial analysts had predicted.

The shares remain more 50% up in the year to date.

Another listed lender exposed to car loan mis-selling is also expected to raise the amount it has set aside.

Close Brothers, which has a £165m provision currently, saw its shares tumble 7% when it admitted an increase was likely once its analysis of the compensation consultation documents was completed.

Car finance makes up approximately a quarter of its total loan book.

The budget may still be more than six weeks away, but rumours of U-turns and changes are already in full swing.

Over the last few days, there have been multiple reports that those inside Whitehall are considering tweaks to the controversial inheritance tax (IHT) reforms on farms announced this time last year.

Plans to introduce a 20% tax on estates worth more than £1m drew tens of thousands to protest in London, many fearing huge tax bills that would force small farms to sell up for good.

Now there are reports the tax threshold could be increased from £1m to £5m (£10m for a married couple) – a shift that would remove smaller farms from being liable to pay.

From February: Farmers continue tax protest

Senior figures in farming have long believed a rise could be the solution to save the smaller farms and it would satisfy most.

However under the proposals, the 50% relief on IHT would be removed for farms above the new threshold.

That means bigger farms, responsible for producing a large amount of produce in our supermarkets, could bear the brunt of the tax burden with the Treasury potentially increasing revenues.

Two senior farming figures told me today that while a threshold increase is welcome, it does nothing to solve an “insolvable” problem.

Read more: What’s the beef with farmers’ inheritance tax?

Big farms have more land to sell, but then they become smaller farms and either produce less, or even divide up, to avoid the tax entirely.

Richard Cornock runs a small dairy farm in south Gloucestershire, which has been in his family since 1822.

Richard Cornock plans to pass his farm on to his son

He hopes to pass it on to his son Harry, who is now 14 and training to become a farm manager.

“I’ve been under so much stress like most farmers worrying about this tax,” he said. “And I really hope they do push the boundaries on the thresholds, because the million pounds they propose at the moment is ridiculous.

“It’s been on my mind the whole time to be honest. I even looked into getting life insurance to insure my life and I can’t get it because I had a heart condition. And that was one way I thought I might be able to cover my kids…”

We paused our chat as he was too upset to continue – an illustration of the stress farmers like him have been under over the last 12 months.

Tens of thousands from the farming community took part in protests in London. Pic: Reuters

The government says it won’t comment on “speculation” about any possible changes, but it has previously defended the IHT reform, saying most estates would not pay and that those who will be liable can spread payments over a decade.

Labour is under pressure to do something to appease the angry farmers, a rural vote that turned from the Conservatives at the last election.

I ask Richard whether any tweak or row back on IHT will restore faith in Labour?

“The damage has been done,” he says.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024