Sam Bankman-Fried could face years in prison over FTX’s $32 billion meltdown — if the U.S. ever gets around to arresting him

FTX CEO Sam Bankman-Fried attends a press conference at the FTX Arena in downtown Miami on Friday, June 4, 2021.

Matias J. Ocner | Miami Herald | Tribune News Service | Getty Images

Sam Bankman-Fried, the disgraced former CEO of FTX — the bankrupt cryptocurrency exchange that was worth $32 billion a few weeks ago — has a real knack for self-promotional PR. For years, he cast himself in the likeness of a young boy genius turned business titan, capable of miraculously growing his crypto empire as other players got wiped out. Everyone from Silicon Valley’s top venture capitalists to A-list celebrities bought the act.

But during Bankman-Fried’s press junket of the last few weeks, the onetime wunderkind has spun a new narrative – one in which he was simply an inexperienced and novice businessman who was out of his depth, didn’t know what he was doing, and crucially, didn’t know what was happening at the businesses he founded.

It is quite the departure from the image he had carefully cultivated since launching his first crypto firm in 2017 – and according to former federal prosecutors, trial attorneys and legal experts speaking to CNBC, it recalls a classic legal defense dubbed the “bad businessman strategy.”

At least $8 billion in customer funds are missing, reportedly used to backstop billions in losses at Alameda Research, the hedge fund he also founded. Both of his companies are now bankrupt with billions of dollars worth of debt on the books. The CEO tapped to take over, John Ray III, said that “in his 40 years of legal and restructuring experience,” he had never seen “such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here.” This is the same Ray who presided over Enron’s liquidation in the 2000s.

In America, it is not a crime to be a lousy or careless CEO with poor judgement. During his recent press tour from a remote location in the Bahamas, Bankman-Fried really leaned into his own ineptitude, largely blaming FTX’s collapse on poor risk management.

At least a dozen times in a conversation with Andrew Ross Sorkin, he appeared to deflect blame to Caroline Ellison, his counterpart (and one-time girlfriend) at Alameda. He says didn’t know how extremely leveraged Alameda was, and that he just didn’t know about a lot of things going on at his vast empire.

Bankman-Fried admitted he had a “bad month,” but denied committing fraud at his crypto exchange.

Fraud is the kind of criminal charge that can put you behind bars for life. With Bankman-Fried, the question is whether he misled FTX customers to believe their money was available, and not being used as collateral for loans or for other purposes, according to Renato Mariotti, a former federal prosecutor and trial attorney who has represented clients in derivative-related claims and securities class actions.

“It sure looks like there’s a chargeable fraud case here,” said Mariotti. “If I represented Mr. Bankman-Fried, I would tell him he should be very concerned about prison time. That it should be an overriding concern for him.”

But for the moment, Bankman-Fried appears unconcerned with his personal legal exposure. When Sorkin asked him if he was concerned about criminal liability, he demurred.

“I don’t think that — obviously, I don’t personally think that I have — I think the real answer is it’s not — it sounds weird to say it, but I think the real answer is it’s not what I’m focusing on,” Bankman-Fried told Sorkin. “It’s — there’s going to be a time and a place for me to think about myself and my own future. But I don’t think this is it.”

Comments such as these, paired with the lack of apparent action by regulators or authorities, have helped inspire fury among many in the industry – not just those who lost their money. The spectacular collapse of FTX and SBF blindsided investors, customers, venture capitalists and Wall Street alike.

Bankman-Fried did not respond to a request for comment. Representatives for his former law firm, Paul, Weiss, did not immediately respond to comment. Semafor reported earlier that Bankman-Fried’s new attorney was Greg Joseph, a partner at Joseph Hage Aaronson.

Both of Bankman-Fried’s parents are highly respected Stanford Law School professors. Semafor also reported that another Stanford Law professor, David Mills, was advising Bankman-Fried.

Mills, Joseph and Bankman-Fried’s parents did not immediately respond to requests for comment.

What kind of legal trouble could he be in?

Bankman-Fried could face a host of potential charges – civil and criminal – as well as private lawsuits from millions of FTX creditors, legal experts told CNBC.

For now, this is all purely hypothetical. Bankman-Fried has not been charged, tried, nor convicted of any crime yet.

Richard Levin is a partner at Nelson Mullins Riley & Scarborough, where he chairs the fintech and regulation practice. He’s been involved in the fintech industry since the early 1990s, and has represented clients before the Securities and Exchange Commission, Commodity Futures Trading Commission and Congress. All three of those entities have begun probing Bankman-Fried.

There are three different, possibly simultaneous legal threats that Bankman-Fried faces in the United States alone, Levin told CNBC.

First is criminal action from the U.S. Department of Justice, for potential “criminal violations of securities laws, bank fraud laws, and wire fraud laws,” Levin said.

A spokesperson for the U.S. Attorney’s Office for the Southern District of New York declined to comment.

Securing a conviction is always challenging in a criminal case.

Mariotti, the former federal prosecutor is intricately familiar with how the government would build a case. He told CNBC, “prosecutors would have to prove beyond a reasonable doubt that Bankman-Fried or his associates committed criminal fraud.”

“The argument would be that Alameda was tricking these people into getting their money so they could use it to prop up a different business,” Mariotti said.

“If you’re a hedge fund and you’re accepting customer funds, you actually have a fiduciary duty [to the customer],” Mariotti said.

Prosecutors could argue that FTX breached that fiduciary duty by allegedly using customer funds to artificially stabilize the price of FTX’s own FTT coin, Mariotti said.

But intent is also a factor in fraud cases, and Bankman-Fried insists he didn’t know about potentially fraudulent activity. He told Sorkin that he “didn’t knowingly commingle funds.”

“I didn’t ever try to commit fraud,” Bankman-Fried said.

Beyond criminal charges, Bankman-Fried could also be facing civil enforcement action. “That could be brought by the Securities Exchange Commission, and the Commodity Futures Trading Commission, and by state banking and securities regulators,” Levin continued.

“On a third level, there’s also plenty of class actions that can be brought, so there are multiple levels of potential exposure for […] the executives involved with FTX,” Levin concluded.

Who is likely to go after him?

The Department of Justice is most likely to pursue criminal charges in the U.S. The Wall Street Journal reported that the DOJ and the SEC were both probing FTX’s collapse, and were in close contact with each other.

That kind of cooperation allows for criminal and civil probes to proceed simultaneously, and allows regulators and law enforcement to gather information more effectively.

But it isn’t clear whether the SEC or the CFTC will take the lead in securing civil damages.

An SEC spokesperson said the agency does not comment on the existence or nonexistence of a possible investigation. The CFTC did not immediately respond to a request for comment.

“The question of who would be taking the lead there, whether it be the SEC or CFTC, depends on whether or not there were securities involved,” Mariotti, the former federal prosecutor, told CNBC.

SEC Chairman Gary Gensler, who met with Bankman-Fried and FTX executives in spring 2022, has said publicly that “many crypto tokens are securities,” which would make his agency the primary regulator. But many exchanges, including FTX, have crypto derivatives platforms that sell financial products like futures and options, which fall under the CFTC’s jurisdiction.

“For selling unregistered securities without a registration or an exemption, you could be looking at the Securities Exchange Commission suing for disgorgement — monetary penalties,” said Levin, who’s represented clients before both agencies.

“They can also sue, possibly, claiming that FTX was operating an unregistered securities market,” Levin said.

Then there are the overseas regulators that oversaw any of the myriad FTX subsidiaries.

The Securities Commission of The Bahamas believes it has jurisdiction, and went as far as to file a separate case in New York bankruptcy court. That case has since been folded into FTX’s main bankruptcy protection proceedings, but Bahamian regulators continue to investigate FTX’s activities.

Court filings allege that Bahamian regulators have moved customer digital assets from FTX custody into their own. Bahamian regulators insist that they’re proceeding by the book, under the country’s groundbreaking crypto regulations — unlike many nations, the Bahamas has a robust legal framework for digital assets.

But crypto investors aren’t sold on their competence.

“The Bahamas clearly lack the institutional infrastructure to tackle a fraud this complex and have been completely derelict in their duty,” Castle Island Ventures partner Nic Carter told CNBC. (Carter was not an FTX investor, and told CNBC that his fund passed on early FTX rounds.)

“There is no question of standing. U.S. courts have obvious access points here and numerous parts of Sam’s empire touched the U.S. Every day the U.S. leaves this in the hands of the Bahamas is a lost opportunity,” he continued.

Investors who have lost their savings aren’t waiting. Class-action suits have already been filed against FTX endorsers, like comedian Larry David and football superstar Tom Brady. One suit excoriated the celebrity endorsers for allegedly failing to do their “due diligence prior to marketing [FTX] to the public.”

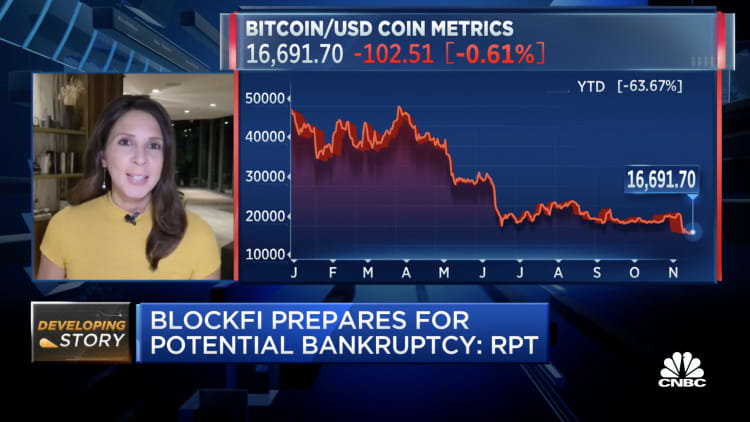

FTX’s industry peers are also filing suit against Bankman-Fried. BlockFi sued Bankman-Fried in November, seeking unnamed collateral that the former billionaire provided for the crypto lending firm.

FTX and Bankman-Fried had previously rescued BlockFi from insolvency in June, but when FTX failed, BlockFi was left with a similar liquidity problem and filed for bankruptcy protection in New Jersey.

Bankman-Fried has also been sued in Florida and California federal courts. He faces class-action suits in both states over “one of the great frauds in history,” a California court filing said.

The largest securities class-action settlement was for $7.2 billion in the Enron accounting fraud case, according to Stanford research. The possibility of a multibillion-dollar settlement would come on top of civil and criminal fines that Bankman-Fried faces.

But the onus should be on the U.S. government to pursue Bankman-Fried, Carter told CNBC, not on private investors or overseas regulators.

“The U.S. isn’t shy about using foreign proxies to go after Assange — why in this case have they suddenly found their restraint?”

What penalties could he face?

Wire fraud is the most likely criminal charge Bankman-Fried would face. If the DOJ were able to secure a conviction, a judge would look to several factors to determine how long to sentence him.

Braden Perry was once a senior trial lawyer for the CFTC, FTX’s only official U.S. regulator. He’s now a partner at Kennyhertz Perry, where he advises clients on anti-money laundering, compliance and enforcement issues.

Based on the size of the losses, if Bankman-Fried is convicted of fraud or other charges, he could be behind bars for years — potentially for the rest of his life, Perry said. But the length of any potential sentence is hard to predict.

“In the federal system, each crime always has a starting point,” Perry told CNBC.

Federal sentencing guidelines follow a numeric system to determine the maximum and minimum allowable sentence, but the system can be esoteric. The scale, or “offense level,” starts at one, and maxes out at 43.

A wire fraud conviction rates as a seven on the scale, with a minimum sentence ranging from zero to six months.

But mitigating factors and enhancements can alter that rating, Perry told CNBC.

“The dollar value of loss plays a significant role. Under the guidelines, any loss above $550 million adds 30 points to the base level offense,” Perry said. FTX customers have lost billions.

“Having 25 or more victims adds 6 points, [and] use of certain regulated markets adds 4,” Perry continued.

In this hypothetical scenario, Bankman-Fried would max out the scale at 43, based on those enhancements. That means Bankman-Fried could be facing life in federal prison, without the possibility of supervised release, if he’s convicted on a single wire fraud offense.

But that sentence can be reduced by mitigating factors – circumstances that would lessen the severity of any alleged crimes.

“In practice, many white-collar defendants are sentenced to lesser sentences than what the guidelines dictate,” Perry told CNBC, Even in large fraud cases, that 30-point enhancement previously mentioned can be considered punitive.

By way of comparison, Stefan Qin, the Australian founder of a $90 million cryptocurrency hedge fund, was sentenced to more than seven years in prison after he pleaded guilty to one count of securities fraud. Roger Nils-Jonas Karlsson, a Swedish national accused by the United States of defrauding over 3,500 victims of more than $16 million was sentenced to 15 years in prison for securities fraud, wire fraud and money laundering.

Bankman-Fried could also face massive civil fines. Bankman-Fried was once a multibillionaire, but claimed he was down to his last $100,000 in a conversation with CNBC’s Sorkin at the DealBook Summit last week.

“Depending on what is discovered as part of the investigations by law enforcement and the civil authorities, you could be looking at both heavy monetary penalties and potential incarceration for decades,” Levin told CNBC.

How long will it take?

Whatever happens won’t happen quickly.

In the most famous fraud case in recent years, Bernie Madoff was arrested within 24 hours of federal authorities learning of his multibillion-dollar Ponzi scheme. But Madoff was in New York and admitted to his crime on the spot.

The FTX founder is in the Bahamas and hasn’t admitted wrongdoing. Short of a voluntary return, any efforts to apprehend him would require extradition.

With hundreds of subsidiaries and bank accounts, and thousands of creditors, it’ll take prosecutors and regulators time to work through everything.

Similar cases “took years to put together,” said Mariotti. At FTX, where record keeping was spotty at best, collecting enough data to prosecute could be much harder. Expenses were reportedly handled through messaging software, for example, making it difficult to pinpoint how and when money flowed out for legitimate expenses.

In Enron’s bankruptcy, senior executives weren’t charged until nearly three years after the company went under. That kind of timeline infuriates some in the crypto community.

“The fact that Sam is still walking free and unencumbered, presumably able to cover his tracks and destroy evidence, is a travesty,” said Carter.

But just because law enforcement is tight-lipped, that doesn’t mean they’re standing down.

“People should not jump to the conclusion that something is not happening just because it has not been publicly disclosed,” Levin told CNBC.

Could he just disappear?

“That’s always a possibility with the money that someone has,” Perry said, although Bankman-Fried claims he’s down to one working credit card. But Perry doesn’t think it’s likely. “I believe that there has been likely some negotiation with his attorneys, and the prosecutors and other regulators that are looking into this, to ensure them that when the time comes […] he’s not fleeing somewhere,” Perry told CNBC.

In the meantime, Bankman-Fried won’t be resting easy as he waits for the hammer to drop. Rep. Maxine Waters extended a Twitter invitation for him to appear before a Dec. 13 hearing.

Bankman-Fried responded on Twitter, telling Waters that if he understands what happened at FTX by then, he’d appear.

Correction: Caroline Ellison is Bankman-Fried’s counterpart at Alameda. An earlier version misspelled her name.

U.S. President Donald Trump (L) listens as Nvidia CEO Jensen Huang speaks in the Cross Hall of the White House during an event on “Investing in America” on April 30, 2025 in Washington, DC.

Andrew Harnik | Getty Images

President Donald Trump on Monday said that he initially asked Nvidia for a 20% cut of the chipmaker’s sales to China, but the number came down to 15% after CEO Jensen Huang negotiated with him.

The comments came after news broke over the weekend that Nvidia agreed to pay the federal government a 15% cut in return for receiving export control licenses that will allow it to once again sell the H20 chip to China and Chinese companies. Nvidia’s Huang visited Trump in the White House on Friday.

“I said, ‘listen, I want 20% if I’m going to approve this for you, for the country,'” Trump said in a press conference in Washington.

Trump said that Nvidia’s H20 is an “old chip that China already has” and is “obsolete.” He compared the H20 chip to Nvidia’s current fastest artificial intelligence chip, which is called Blackwell, and said that he wouldn’t allow those to be sold to China without significant downgrades, such as a 30% to 50% reduction in performance.

“The Blackwell is super-duper advanced. I wouldn’t make a deal with that,” Trump said, adding that it was possible to make a deal for a “somewhat enhanced in a negative way” version of Blackwell.

“That’s the latest and the greatest in the world. Nobody has it. They won’t have it for five years,” Trump said.

One reason for the U.S. export controls is fear that providing advanced chips to China could allow the foreign power to leapfrog the U.S. in AI capabilities. Many have said that could pose a threat to the national security of the U.S.

Trump said that China already has chips with some similar capabilities to the H20.

Huang has said that it is better for U.S. national security if Chinese AI developers use U.S. technology, and that denying them access to Nvidia chips would actually encourage the Chinese chip industry to develop and catch up.

“He’s selling a essentially old chip,” Trump said. “Huawei has a similar chip.”

The H20 is a Chinese-specific chip that has had its performance slowed down. It is related to Nvidia’s H100 and H200 chips that are used in the U.S. The H20 was introduced after the Biden administration implemented export controls on AI chips in 2023.

In April, the Trump administration said it would require a license to export the H20 chip, and in May, Huang said that “effectively closed” the market off to Nvidia. Huang said that Nvidia was expecting to sell about $8 billion in H20 chips in the July quarter before sales were stopped.

“While we haven’t shipped H20 to China for months, we hope export control rules will let America compete in China and worldwide,” an Nvidia spokesperson told CNBC on Monday.

Trump on Monday also said that Huang plans to visit him again to negotiate export licenses for the Blackwell chips.

“I think he’s coming to see me again about that,” Trump said.

A White House official confirmed to CNBC that AMD, the second-place AI chip maker, will also pay 15% to receive an export license for its China-focused AI chip, the Instinct MI308.

WATCH: Nvidia, AMD to pay U.S. 15% of AI chip sales in China to secure export licenses

After four previous scrubs or delays in a row since August 7th SpaceX launches Amazon KF-02 Kuipeer Satellites after the 5th attempt August 11th 2025 at 8:35 AM SLC-40 Cape Canaveral, Brevard County, Florida USA.

Scott Schilke| SipaUSA |AP

Amazon shipped another batch of internet-beaming satellites into orbit on Monday atop a SpaceX Falcon 9 rocket, after four previous launch attempts were interrupted by weather issues.

Monday’s launch is the fourth Kuiper mission, and Amazon now has 102 satellites in orbit.

The Falcon 9 rocket lifted off from Cape Canaveral, Florida, at 8:35 a.m. ET. Roughly an hour after launch, SpaceX confirmed all 24 of Amazon’s Kuiper satellites were successfully deployed.

The mission was originally scheduled for last Thursday, but SpaceX was forced to scrub the launch, along with three more attempts over the past few days due to rainfall.

For the second time, Amazon turned to Elon Musk‘s SpaceX, its chief competitor in the low-earth orbit satellite market, for help building out its constellation.

SpaceX’s Starlink is currently the dominant provider of low-earth orbit satellite internet, with a constellation of roughly 8,000 satellites and about 5 million customers worldwide.

Amazon is racing to get more of its Kuiper satellites into space to meet a deadline set by the Federal Communications Commission.

The FCC requires that Amazon have about 1,600 satellites in orbit by the end of July 2026, with the full 3,236-satellite constellation launched by July 2029.

Amazon has booked up to 83 launches, including three rides with SpaceX.

While the company is still in the early stages of building out its constellation, Amazon has already inked deals with governments as it hopes to begin commercial service later this year.

WATCH: Amazon launches first Kuiper internet satellites into space

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike