The small pipeline playing an oversized role in the energy crisis

The chances are you haven’t heard of the BBL pipeline.

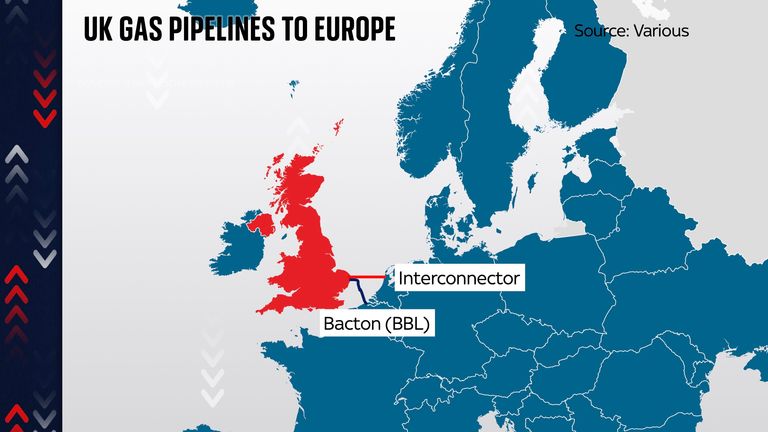

It’s a 235km steel tube which runs under the North Sea between Balgzand in the northern tip of the Netherlands and Bacton in Great Britain.

It’s one of those bits of innocuous infrastructure which, most of the time, no-one except energy analysts pay all that much attention to.

But let’s spend a moment pondering this pipe, because it could prove enormously consequential for all of us in the coming months.

Indeed, BBL has already played a silent but essential role in the Ukraine war and, for that matter, the fate of Europe, because this is one of the two main pipelines transporting gas between the UK and Northern Europe.

Actually, BBL is the smaller of the two pipes, the other of which is the rather unimaginatively-named “Interconnector” pipe. But the reason it’s worth focusing on BBL is because in the past few days something rather interesting happened there.

Before we get to that, though, it’s worth reminding ourselves of the big picture here, the challenge facing Europe: a desperate shortage of energy.

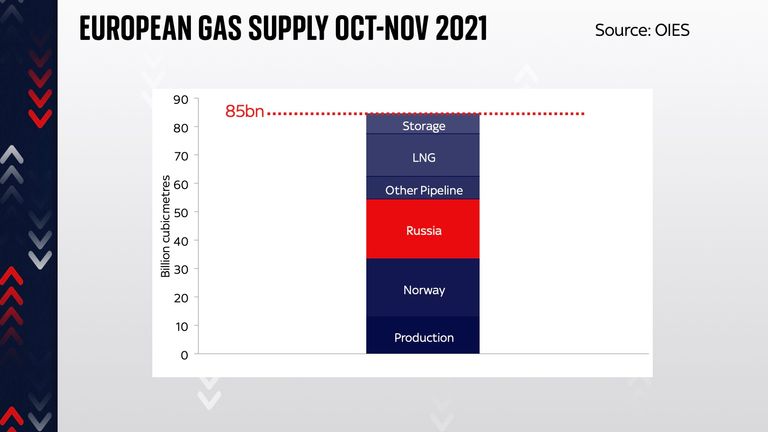

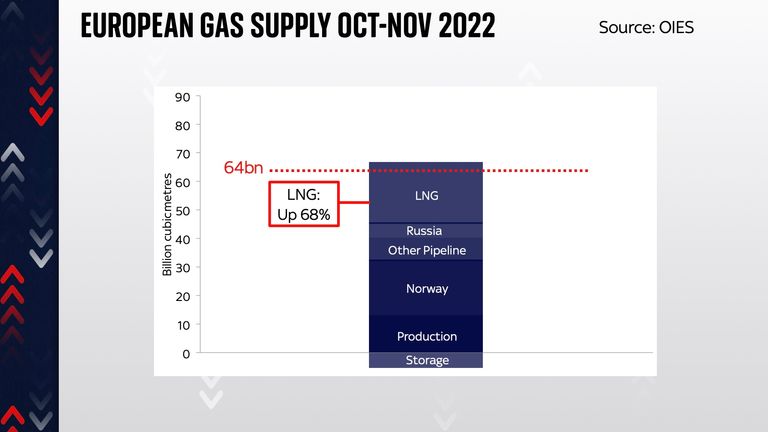

Here’s the best way of understanding it: this time last year, Europe (including the UK) was consuming roughly 85 billion cubic metres of natural gas a month. Of that, about 21 billion cubic metres (bcm) – roughly a quarter – came via Russian pipelines.

That gas didn’t just go into our boilers and gas-fired power stations.

It was a feedstock which helped us manufacture chemicals and fertilisers.

It fed us, it fuelled industry, it helped keep the lights on.

In the wake of the Russian invasion of Ukraine, suddenly Europe couldn’t take that 25% of its energy for granted any more. And indeed, most of the Russian supply has since dwindled (it’s now down 81% to about 4bcm a month).

And so much of what might today be categorised as economic news – the rocketing rate of inflation, the squeeze on household incomes and the recession we’re now sliding into – really comes back to this gap, between the gas we used to consume and the gas we can now lay our hands on.

And the short answer is that getting hold of that extra gas isn’t easy at all.

Partly that’s because most of the non-Russian sources which are already pumping gas into European pipelines (which is to say: mainly Norway but, to a lesser extent, the UK, Netherlands and Algeria) are already producing about all they can.

These days you can ship gas (in the form of Liquefied Natural Gas (LNG), a supercooled liquid) across the ocean from Qatar and the US, but that depends on a few things.

The first is actually getting hold of that gas. The UK on Wednesday published details of a new “US-UK Energy Security and Affordability Partnership” which aims to provide more LNG to the UK. That matters because Britain and Europe are essentially competing with China and other Asian nations on global markets for these cargoes.

The second (and perhaps even more important) factor is having terminals where you can receive and re-gasify the LNG and then feed it into your domestic pipeline network.

But there are only so many of these ports and regasification facilities in Europe. Germany, for instance, has none (though it’s got some temporary capacity coming up soon). The UK has lots. Indeed, it has more LNG capacity in its three ports (two at Milford Haven, one at Isle of Grain) than Belgium and the Netherlands have in total.

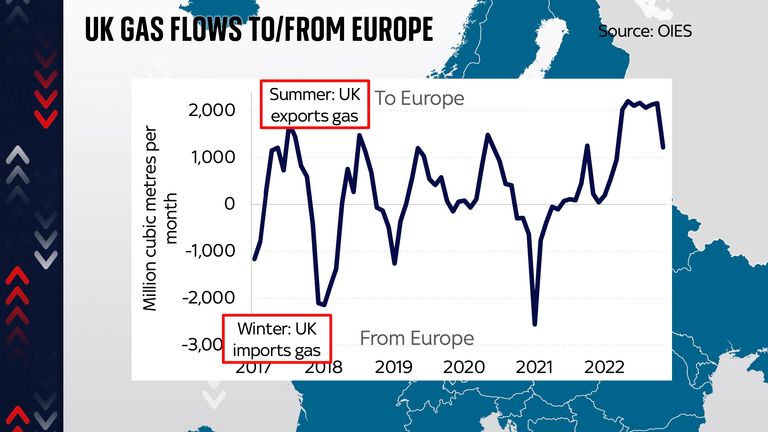

The logic of this was that back at the start of the conflict, it looked quite plausible that the UK would become a sort of energy “land bridge” across which gas could be transited to Europe. And that indeed is precisely what happened, which brings us back to the pipeline crossing from the UK to the north of Europe.

Over the past year, a stupendous amount of LNG has been coming into UK ports, drawn in by the stupendously high gas price, from where it has been transferred across the UK’s pipeline network and thence into the European system.

To put this into perspective, in the four summers since 2017, the average amount of natural gas transferred from the UK was around 5.7 trillion cubic metres. This past summer the total was 20.5 trillion cubic metres.

It’s worth dwelling on this for a moment, for it represents one of the under appreciated stories of the Russia-Ukraine war.

Much of the gas which replenished the storage facilities in Europe, which should help them survive the coming winter while keeping homes heated, despite the absence of Russian gas, came via the UK – via the BBL and Interconnector pipelines.

And that’s actually understating it, because those pipelines were only so wide, and so could only carry a certain proportion of the LNG flowing into the UK, but what also happened this summer is that UK gas power plants went into overdrive, burning that gas and turning it into electricity, which was also fed via undersea cables into Europe.

This mattered. Much of France’s nuclear power fleet was out of action this summer as water levels in French rivers ran too low to provide the necessary coolant. British electrons were part of the explanation for why the lights never went out in France.

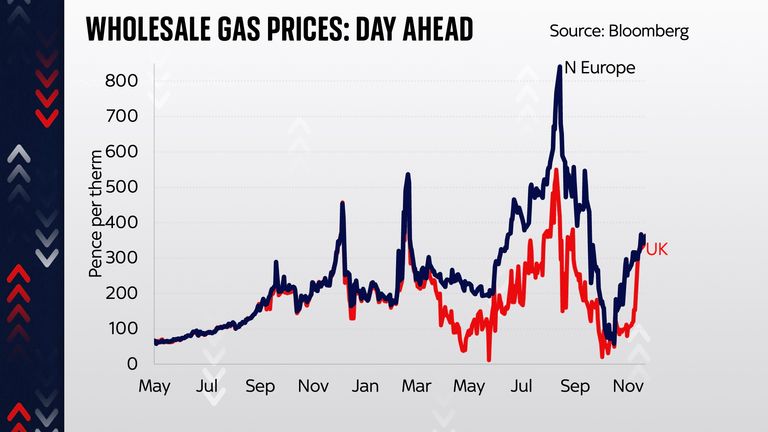

This astounding flow of gas (which of course has its own climactic consequences) caused some interesting price fluctuations this past year. As we reported earlier in the summer, it helped suppress UK day-ahead gas prices down to surprisingly low levels.

For a period in May and June, the UK wholesale gas price was less than half the level in continental Europe – because the UK was awash with all these natural gas molecules trying to fit themselves into these steel pipes coming out of Bacton.

But in recent weeks those flows have begun to drop, which brings us to the interesting thing that changed in the past few days.

For the first time since the Russian invasion of Ukraine and the extraordinary rollercoaster in the gas market, a small quantity of natural gas begun to flow back into the UK.

It’s important not to overstate this. The numbers are very small indeed. But it’s a reminder that actually, in “normal” times, these pipelines serve a very different purpose from the one they’ve served in recent months.

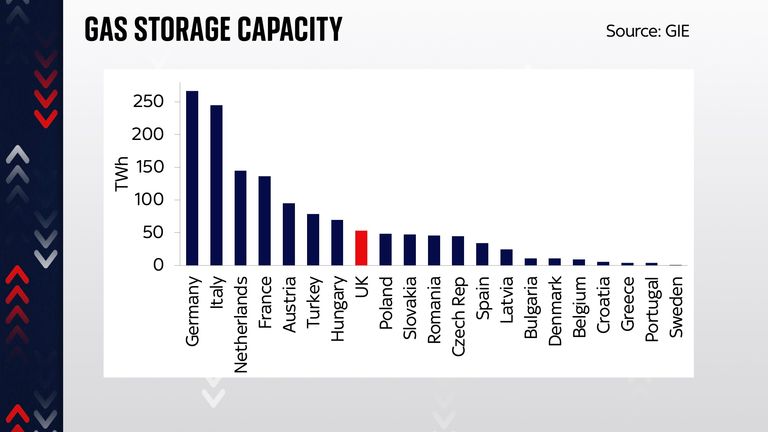

Britain doesn’t have much domestic storage for natural gas. While Germany has about 266 terawatt-hours of storage capacity, the UK has only 53, barely enough to keep boilers going for more than a week or two.

However, the UK strategy in recent years has been to use Europe as a kind of storage system. Think of these underground caverns as a kind of bank.

You deposit gas in them in the warm months and take it out when it gets cold. And in “normal” times the UK has “deposited” its gas in Europe in the summer, sending much of the stuff that came out of the North Sea (and some stuff from those LNG terminals) across the two pipelines and those molecules went into European storage.

And in winter, the UK would typically “withdraw” the gas from Europe when it got cold and it needed a little more for peoples’ boilers. Into Europe in the summer; out of Europe in the winter.

But that brings us to this winter. The UK has put an extraordinary amount of gas into European storage in the summer. What happens if it gets really cold? In any normal winter, it would need to get that gas out of Europe via those pipelines. But this, of course, is not a normal winter. There is a chance that the remaining flows of gas from Russia dry up further, meaning there could be a real shortage. In such circumstances, what happens?

If the market carries on working, then that would push up prices high on continental Europe, but the logic is that in order to attract that gas across the channel, the UK would have to pay even higher prices than continental Europe. In other words, while prices in the UK have been lower than Europe for most of the summer, they could well be higher than Europe for most of the winter.

There is a sign that this is already happening.

In the past couple of days, those prices have converged. But there is also a scarier question: what if the market doesn’t function, because of political interference? What if European nations decide that storage in, say Germany (or for that matter the European Union) cannot leave? Where does that leave the UK, which tends to rely on those pipeline flows from Europe in the event of a cold snap.

The short answer is that no-one really knows. What we do know is that this story isn’t over yet. Gas prices are already eye-wateringly high, especially when you consider that the Government is effectively subsidising them. It’s not implausible that they get even higher.

Business

In Halifax’s night-time economy, no one is holding back over what is required in the budget

In the upstairs bar of a slick new brewery, the cheese-lovers of Halifax are paying “homage to fromage”.

It is one of the first events in the historic West Yorkshire town for the monthly cheese club and there is a decent turn-out.

Sky News visited Halifax’s clubs, bars and restaurants to get an insight into people’s priorities

The night-time economy in Halifax is a useful measure of how the landscapes of our town and cities have changed

Discussion of Wednesday’s budget is not as popular as an accompaniment to the cheese as the selection of wines. But no one holds back on what is required of the chancellor.

Natalie Rogers, who runs her own small business with her partner, said there needs to be focus.

Small business owner Natalie Rogers wants to see more investment in local industries

“I think investing in small businesses, investing in these northern towns, where at one time we were making all the money for the country, can we not get back to that? We’re not investing in local industries.”

At the next table, with a group of friends, Ali Fletcher said there needs to be bigger targets.

“I think wealth inequality is a major problem. The divide is getting wider. For me, a wealth tax is absolutely critical. We need to address this question of ‘Is there any money left?’. There’s plenty of money, it’s all about choices that government make.”

At this monthly cheese club, people told us about their priorities ahead of the budget

The evening’s cheese tasting was being marshalled by Lisa Kempster. “The impression I get from talking to people is there’s a lot of uncertainty, but when you ask them what they’re uncertain about, they’re not really sure, there’s just a general feeling of uncertainty and being cautious.”

Ali Fletcher reckons wealth inequality is a major problem

Read more:

Budget will be big – and Starmer has some serious convincing to do

Reeves vows to ‘grip the cost of living’

What tax rises could chancellor announce?

This corner of Halifax, close to the town’s historic Piece Hall, is buzzing with clubs, bars and restaurants, trying hard to defy the crunch in the night-time economy. It is a useful measure of how the landscapes of our town and cities has changed.

“Whenever there’s a budget, for a few days afterwards, there’s a drop off in trade,” said Michael Ainsworth, owner of the Graystone Unity, a bar and music venue in the town.

“I accept the government needs to raise money but, in this day and age, there’s better ways to go about doing that, like closing tax loopholes for the huge businesses to operate up with banking arrangements outside the UK.”

Michael Ainsworth owns a bar and music venue and thinks the chancellor needs to close tax loopholes

In the bar, a folk singer is going through a quirky and caustic set. In the basement, a punk band called Edward Molby is considerably louder.

On a sofa in the main bar, recent graduates Josh Kinsella and Ruby Firth, newly arrived in Halifax because of its more affordable housing, pinpoint what they want on Wednesday.

“Can we stop triple-locking the pensions, please? Stop giving pensioners everything. For God’s sake, I know they have hard times in the 70s and the 80s, but it just feels like we’re now paying for everyone else.”

Josh Kinsella and Ruby Firth feel there’s too much focus on pensioners

Ben Randm is a familiar face at the bar and well known on the music scene with his band, Silver Tongued Rascals.

“Everyday people are seen as statistics, we’re always the afterthought. When the cuts are done, we’re always impeded and the ramifications that has for people’s livelihoods, for people’s mental health, for people’s passion and drive… it’s such a struggle.”

He, like many in the night-time economy sector, wants extra help for hospitality and venues that, he says, provide a vital community link.

Ben Randm who has his own band reckons everyday people are ‘always the afterthought’

David Van Gestel chose Halifax to open the third branch of MAMIL, a bar in jokey honour of those cycling “middle-aged men in Lycra”. On a busy quiz night, he said venues had to provide something different to get people out of their homes.

“I think the government needs to start putting some initiatives in place. They talk about growth but the reality is that the only thing we’re seeing grow is our costs.”

There’s a lot going on at TikTok right now.

As well as online safety updates and new features, the company is introducing sweeping changes to how it moderates the platform’s content.

At the same time, there’s an intense focus on online safety, particularly here in the UK.

With all that going on, Sky News got a rare, exclusive sit-down with one of TikTok’s senior safety executives, Ali Law.

The increasing role of artificial intelligence

One of the biggest changes happening at TikTok is around artificial intelligence.

Like most social media companies, TikTok has used AI to help moderate its platform for years – it is useful for sifting out content that obviously violates policies, and TikTok says it now removes around 85% of violative content without getting a human involved.

File pic: Reuters

Now, it is increasing its use of AI and will be relying less on human moderators. So what’s changed that means TikTok is confident AI can keep young users safe?

“One of the things that has changed is really the sophistication of those models,” said Mr Law, who is TikTok’s director of public policy and government affairs for northern Europe. He explained that AI is now better able to understand context.

“A great example is being able to identify a weapon.”

Whereas previous models may have been able to identify a knife, newer models can tell the difference between a knife being used in a cooking video and a knife in a graphic, violent encounter, according to Mr Law.

“We set a high benchmark when it comes to rolling out new moderation technology.

“In particular, we make sure that we satisfy ourselves that the output of existing moderation processes is either matched or exceeded by anything that we’re doing on a new basis.

“We also make sure the changes are introduced on a gradual basis with human oversight so that if there isn’t a level of delivery in line with what we expect, we can address that.”

Human moderator jobs being cut

That increasing use of AI means TikTok will rely less on its network of tens of thousands of human moderators around the world.

TikTok moderators and union workers protested outside the company’s London headquarters over job cuts

In London alone, the company is proposing to cut more than 400 moderator jobs, although there are reports a number of those jobs will be rehired in other countries.

On 30 October, Paul Nowak, general secretary of the TUC union, said “time and time again” TikTok had “failed to provide a good enough answer” about how the cuts would impact the safety of UK users.

Ali Law speaks to Sky News from TikTok’s European headquarters in Dublin

When Sky News asked if Mr Law could ensure UK users’ safety after the cuts, he said the company’s focus is “always on outcomes”.

“Our focus is on making sure the platform is as safe as possible.

“We will make deployments of the most advanced technology in order to achieve that, working with the many thousands of trust and safety professionals that we will have at TikTok around the world on an ongoing basis.”

Dame Chi Onwurah speaks at the House of Commons. File pic: Reuters

The UK’s science, technology and innovation committee, led by Labour MP Chi Onwurah, has issued a probe into the cuts, with Ms Onwurah calling them “deeply concerning”.

She said AI “just isn’t reliable or safe enough to take on work like this” and there was a “real risk” to UK users.

However, Mr Law said that, as a parent himself, he is “also highly concerned and highly interested in issues of online safety”.

“That’s why I’m so confident in the changes that we are making at TikTok in terms of content moderation as a whole,” he said.

“The power really comes in the combination of the best technology and human experts working together, and that still is the case at TikTok and it will be going forwards as well.”

UK’s online safety rules: One month on

New wellness tools

The interview came at the end of an online safety event at TikTok’s Dublin office, its European headquarters.

During the conference, the company announced a number of new features designed to increase user safety, including a new in-app Time and Wellbeing hub for TikTok users.

The hub is designed with the Digital Wellness Lab at Boston Children’s Hospital and gamifies mindfulness techniques like affirmations, not using TikTok during the night and lowering your screentime.

Ali Law, TikTok’s director of public policy and government affairs for northern Europe

Read more from Sky News:

Meta to block Instagram and Facebook for users under 16 in Australia

Half of novelists fear AI will replace them entirely, survey finds

How violent extremists are thriving online – and why it’s getting harder to catch them

Cori Stott, executive director of the digital wellness lab, said many people use their phones to “set their wellbeing, to reset their emotions, to find these safe spaces, and also to find entertainment”.

The hub was built as part of the TikTok app because young people want wellness tools “where they already are”, without needing to go to a different app, she said.

Still, there are plenty of reports suggesting that phone use and social media has a damaging effect on young people’s mental health… is TikTok trying to solve a problem of its own creation?

“If you are a teen on the app, you will load up and find that you have, if you’re under 16, a private profile, no access to direct messaging, a screen time limit set at an hour, [and at] 10pm sleep hour suggestion,” said Mr Law.

“So the experience is one that does try and promote a balanced approach to using the app and make sure that people have the options to set their own guardrails around this,” he said.

“I think the other thing I’d say is that the content on TikTok is, in the main, inspiring, surprising, creative.”

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024