Budget 2023: UK economy will avoid recession in 2023 and inflation set to plummet, says chancellor

Jeremy Hunt said the British economy is “proving the doubters wrong” and will avoid recession, as he delivered his first full budget speech to Parliament.

The chancellor said the government’s plan for the economy was “working” as he announced what he called a “budget for growth”.

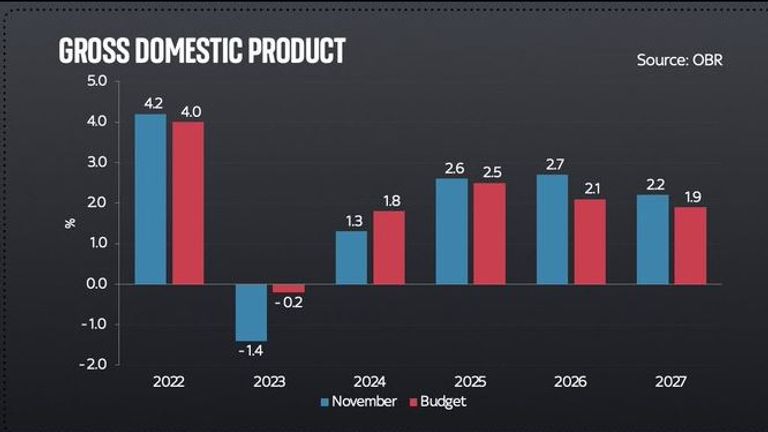

He said forecasts from the Office for Budget Responsibility (OBR) showed the UK would avoid recession – two-quarters of negative growth – in 2023, despite previous predictions.

But the economy will still contract overall this year by 0.2%, and the OBR has warned living standards are still expected to fall by the largest amount since records began.

More on Budget 2023:

Politics live: The budget as it happened and reaction

The key points of the budget at a glance

The forecaster said the drop would be lower than previously expected but that real households’ disposable income per person would still tumble 5.7% over the two financial years 2022-23 and 2023-24.

Households will therefore feel the pinch more than at any point since 1957, according to the OBR.

Click here for our budget calculator to see if you are better or worse off

The OBR forecasts also said inflation in the UK would fall from 10.7% in the final quarter of last year to 2.9% by the end of 2023.

Mr Hunt said it showed Rishi Sunak’s goal of halving inflation this year would be met, but he added: “We remain vigilant and will not hesitate to take whatever steps are necessary for economic stability”.

However, Labour leader Sir Keir Starmer said the chancellor’s “boasts” about lower inflation were “ridiculous”, adding: “The idea that it’s a tax cut, British people can see through that.

“They see their tax burden at its highest level for 70 years and they know it’s not the government that’s lowering inflation.

“It’s working people, earning less, enjoying less. It’s their sacrifice that is helping to bring inflation down and they deserve better than another cheap trick from the government of gimmicks, making them pay whilst trying to claim the credit.”

Read more:

No big bangs, but there still could be blow ups: Beth Rigby’s political analysis

No feel-good factor: Ed Conway’s economic analysis

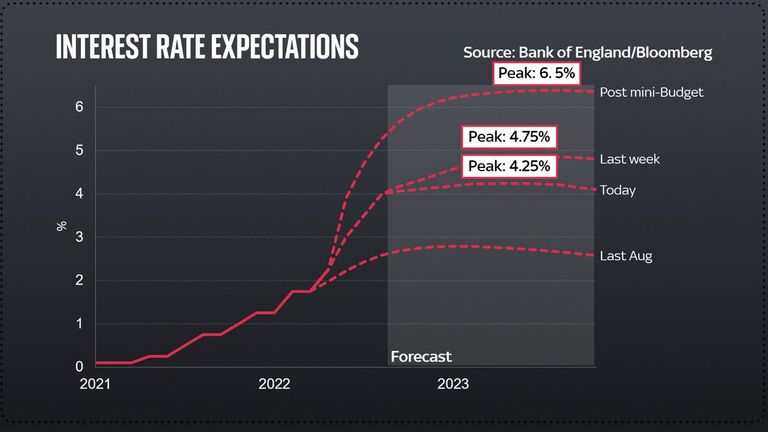

Interest Rate Expectations

A number of other plans were unveiled by Mr Hunt, including:

• Bringing charges for prepayment meters in line with direct debit charges, impacting over four million households and saving them an average of £45 per year

• Making duty on draught products in pubs up to 11p lower than supermarkets

• Maintaining the freeze in fuel duty

The chancellor also said £11bn will be added to the defence budget over the next five years – following an announcement earlier this week – saying it would be nearly 2.25% of GDP by 2025. The government’s ambition is for it to reach 2.5%, he added.

And after reports he would increase the pensions lifetime allowance to £1.8m in an attempt to encourage doctors and other high earners back to work, Mr Hunt decided to scrap the limit entirely, as well as increasing the pensions annual tax-free allowance from £40,000 to £60,000.

He told the Commons: “In the face of enormous challenges I report today on a British economy which is proving the doubters wrong.

“In the autumn we took difficult decisions to deliver stability and sound money. Since mid-October, 10-year gilt rates have fallen, debt servicing costs are down, mortgage rates are lower and inflation has peaked.

“The International Monetary Fund says our approach means the UK economy is on the right track.”

But Sir Keir said the only permanent tax cut in the budget was for “the richest 1%”, adding: “How can that possibly be a priority for this government?”

‘This a failure you can measure not just in the figures but in the empty pockets of working people,’ says the Labour leader.

The Labour leader continued: “Again we see a failure to grip the long-term challenges. No determination to create growth that unlocks the potential of the many – working people being made to pay for Tory choices and Tory mistakes.”

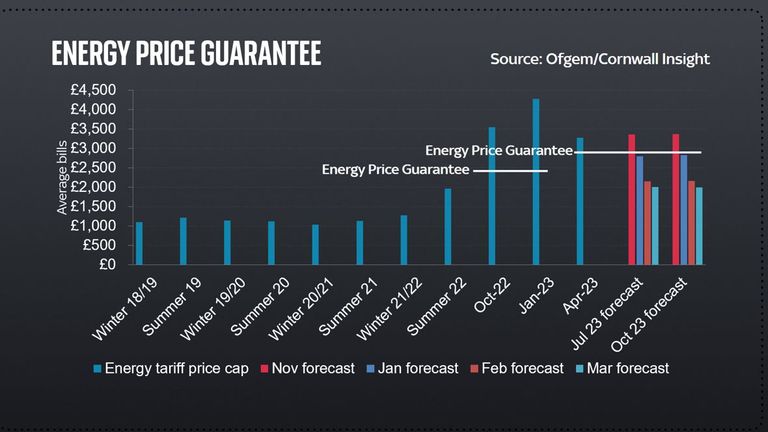

Some policies were revealed ahead of the chancellor’s speech, including keeping the cap on energy prices at £2,500 for a further three months, despite a planned rise to £3,000 in April, and 12 new investment zones.

Sky News also reported last night his promise to provide 30 hours of childcare a week to parents of one and two-year-olds, and to give a further cash injection to the sector to increase the availability of existing free childcare for three to four-year-olds.

But Mr Hunt went further on this measure, saying the care would be available from September 2024 when a child reaches nine months, as well as promising to increase funding for nurseries and pay those on Universal Credit upfront for the childcare they need to get.

However, he also confirmed the ratio for how many children each staff member looks after can be raised from one per four to one per five – though he said it was optional for both providers and parents.

Hunt explains childcare delay

There were more announcements to fit with Mr Hunt’s “three E’s” philosophy – enterprise, employment and education.

They included:

• Incentive payments of up to £1,200 for childminders who sign up to the profession

• Enhanced credit for small and medium businesses, and creative firms

• An extension to relief for theatres, orchestras and museums

• Tax relief on energy efficient measures in firms

• £900m investment into supercomputing

The chancellor also confirmed widely reported plans to abolish the Work Capability Assessment for disabled people to “separate benefit entitlement from an individual’s ability to work”.

Mr Hunt promised a new programme called Universal Support, describing it as “a new, voluntary employment scheme for disabled people where the government will spend up to £4,000 per person to help them find appropriate jobs and put in place the support they need”.

And he said there would be a £400m fund to help those who are forced to leave work because of a health condition to get support in the workplace.

Chancellor Jeremy Hunt MP has announced that the energy price guarantee will remain at £2,500 until the end of June.

Mr Hunt confirmed he would keep the incoming rise in corporation tax – from 19% to 25% – despite anger from some of his own backbenchers.

But in a bid to keep businesses happy, he introduced a new benefit where every pound a company invests in equipment can be deducted in full and immediately from taxable profits – “a corporation tax cut worth an average of £9bn a year for every year it is in place”.

Click to subscribe to the Sky News Daily wherever you get your podcasts

In what appeared to echo recent Labour policy, the chancellor announced continued state-financed investment in nuclear power and the launch of Great British Nuclear, saying the public body will “bring down costs and provide opportunities across the nuclear supply chain to help provide up to one quarter of our electricity by 2050”.

And he said nuclear energy would be reclassified as “environmentally sustainable” to give it the same access to investment incentives as renewables.

Today’s statement was Mr Hunt’s first full budget as chancellor – having been brought in by Liz Truss to reverse a number of measures from her disastrous mini-budget last October and kept on by Rishi Sunak after he took over as prime minister.

It came against a backdrop of mass industrial action, with hundreds of thousands of workers today staging what is believed to be the biggest walkout since the current wave of unrest began.

Teachers, university lecturers, civil servants, junior doctors, London Underground drivers and BBC journalists are among those taking to picket lines around the country amid widespread anger over pay, job security, pensions and conditions.

Labour’s shadow chancellor, Rachel Reeves, said ahead of the budget that it was “an opportunity for the government to get us off their path of managed decline”.

She added, if her party were in power, their focus would be on securing the highest growth in the G7.

“Our plan will help us lead the pack again, by creating good jobs and productivity growth across every part of our country, so everyone, not just a few, feel better off,” she added.

A greater proportion of electric cars were sold last month than at any point this year, industry data shows.

More than a quarter (26.5%) of cars sold in August were electric vehicles (EVs), according to figures from motor lobby group the Society for Motor Manufacturers and Traders (SMMT).

It’s the largest amount of sales since December 2024 and comes as the government introduced financial incentives to help drivers make the move to zero tailpipe emission cars.

Money blog: KFC rival coming to UK

The full suite of grants were not available during the month, however, with a further 35 models eligible for £1,500 off early in September.

Throughout August more models became eligible for price reductions, meaning more consumers could be tempted to purchase an EV in September.

New EV grants to drive sales came into effect in July

The increased percentage of EV sales came despite an overall 2% drop in buying, compared to a year earlier, in what is typically the quietest month for car purchases.

What are the rules?

The numbers suggest the car industry could be on course to meet the government’s zero-emission vehicle (ZEV) mandate, the thinktank Energy & Climate Intelligence Unit (ECIU) has said.

It stipulates that new petrol and diesel cars may not be sold from 2030.

Read more:

Bank lobby chief warns Reeves over budget tax raid

Tax the rich to thwart Reform, TUC chief urges Labour

Amid pressure from industry, the government altered the mandate in April to allow for hybrid vehicles, which are powered by both fuel and a battery, to be sold until 2035.

Sales of new petrol and diesel vans are also permitted until 2035.

Until then, 28% of cars sold must be electric this year, with the share rising to 33% in 2026, 38% in 2027 and 66% in 2029, the final year before the new combustion engine ban.

Manufacturers face fines for not meeting the targets.

Last year, the objective of making 22% of all car sales purely EVs was surpassed, with EVs comprising 24.3% of the total sold in 2024.

Why?

The increased portion of EV sales can be attributed to increased model choice and discounting, on top of the government reductions, the SMMT said.

Savings from running an electric car are also enticing motorists, the ECIU said. “Demand for used EVs is already surging because they can offer £1,600 a year in savings in owning and running costs.”

“This matters for regular families as the pipeline of second-hand EVs is dependent on new car sales, which hit the used market after around three to four years.

Businesses have cut jobs at the fastest pace in almost four years, according to a closely-watched Bank of England survey which also paints a worrying picture for employment and wage growth ahead.

Its Decision Maker Panel (DMP) data, taken from chief financial officers across 2,000 companies, showed employment levels over the three months to August were 0.5% lower than in the same period a year earlier.

It amounted to the worst decline since autumn 2021 as firms grappled with the implementation of budget measures in the spring that raised their national insurance contributions and minimum wage levels, along with business rates for many.

Money latest: Eight supermarkets ranked for price

The start of April also witnessed the escalation in Donald Trump’s global trade war which further damaged sentiment, especially among exporters to the United States.

The survey showed no improvement in hiring intentions in the tough economy, with companies expecting to reduce employment levels by 0.5% over the coming year.

That was the weakest outlook projection since October 2020.

At the same time, the panel also showed that participants planned to raise their own prices by 3.8% over the next 12 months. That is in line with the current rate of inflation.

The news on wages was no better as the central forecast was for an average rise of 3.6% – down from the 4.6% seen over the past 12 months.

If borne out, it would mean private sector wages rising below the rate of inflation – erasing household and business spending power.

The Bank of England has been relying on data such as the DMP amid a lack of confidence in official employment figures produced by the Office for National Statistics due to low response rates.

August: Tax rises playing ’50:50′ role in rising inflation

Bank governor Andrew Bailey told a committee of MPs on Wednesday that he was now less sure over the pace of interest rate cuts ahead owing to stubborn inflation in the economy.

The consumer prices index measure is expected to peak at 4% next month – double the Bank’s target rate – from the current level.

Higher interest rates only add to company costs and make them less likely to borrow for investment purposes.

At the same time, employers are fearful that the coming budget, set for late November, may contain no relief.

Why aren’t we hearing about the budget ‘black hole’?

Sky News revealed on Thursday how the head of the banking sector’s main lobby group had written to the chancellor to warn that any additional levy on bank profits, as suggested by a think-tank last week, would only damage her search for growth.

Rachel Reeves is believed to be facing a black hole in the public finances amounting to £20bn-£40bn.

Tax rises are believed to be inevitable, given her commitment to fiscal rules concerning borrowing by the end of the parliament.

Heightened costs associated with servicing such debts following recent bond sell-offs across Western economies have made more borrowing even less palatable.

Why did UK debt just get more expensive?

Ms Reeves is expected to raise some form of wealth tax, while other speculation has included a shake-up of council tax.

She has consistently committed not to target working people but the Bank of England data, and official ONS figures, would suggest that businesses have responded to 2024 budget measures by cutting jobs since April, with hospitality and retail among the worst hit.

Commenting on the data, Rob Wood, chief UK economist at Pantheon Macroeconomics, said: “The DMP survey shows stubborn wage and price pressures despite falling employment, continuing to suggest that structural economic changes and supply weakness are keeping inflation high.

“The MPC [monetary policy committee of the Bank of England] will have to be cautious, so we remain comfortable assuming no more rate cuts this year.”

“That said, the increasing signs of labour market weakness suggest dovish risks,” he concluded.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment11 months ago

Environment11 months agoHere are the best electric bikes you can buy at every price level in October 2024