Q1 2023 earnings preview: What to expect today")

Tesla (TSLA) Q1 2023 earnings preview: What to expect today

Tesla (TSLA) is about to release Q1 2023 financial results today, Wednesday, April 19, after the markets close. As usual, a conference call and Q&A with Tesla’s management are scheduled after the results.

Here we’ll take a look at what both the street and retail investors are expecting for the quarterly results.

Tesla Q1 2023 deliveries

As usual, Tesla already disclosed its Q1 vehicle delivery and production numbers, which drive the vast majority of the company’s revenue.

Earlier this month, Tesla confirmed that it delivered a new record of over 422,000 electric vehicles during the first quarter of the year.

Tesla also confirmed having produced 440,000 vehicles during the quarter – also a new record.

Delivery and production numbers are always slightly adjusted during earning results.

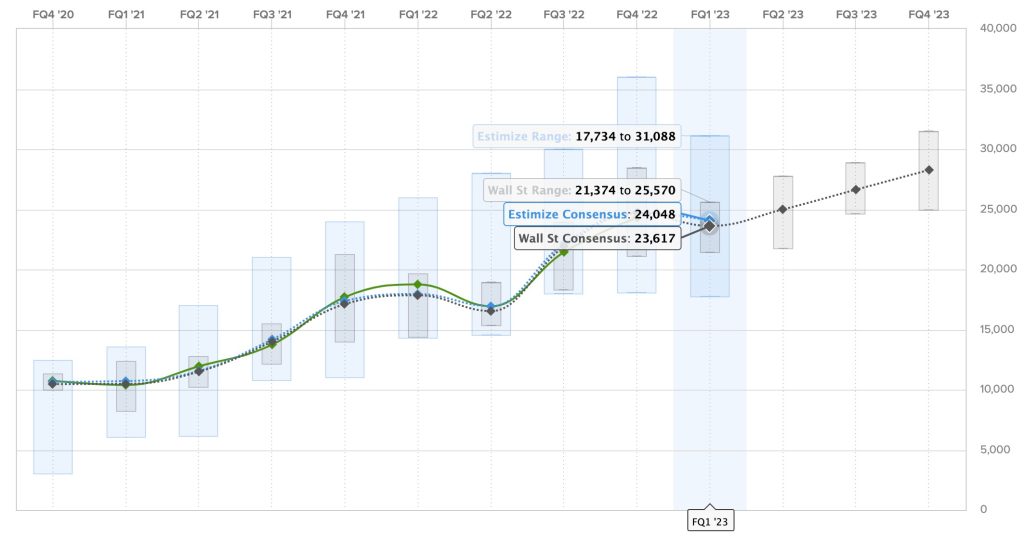

Tesla Q1 2023 revenue

For revenue, analysts generally have a pretty good idea of what to expect, thanks to the delivery numbers.

The Wall Street consensus for this quarter is $23.617 billion, and Estimize, the financial estimate crowdsourcing website, predicts a higher revenue of $24.048 billion.

Despite the new record number of deliveries, these estimates would represent a quarter-to-quarter decrease in revenue due to Tesla’s implementing large price cuts during the first quarter.

Nonetheless, it would be a massive year-over-year increase from $18 billion in revenue in Q1 2022.

Here are the predictions for Tesla’s revenue over the past two years, where Estimize predictions are in blue, Wall Street consensus is in gray, and actual results are in green:

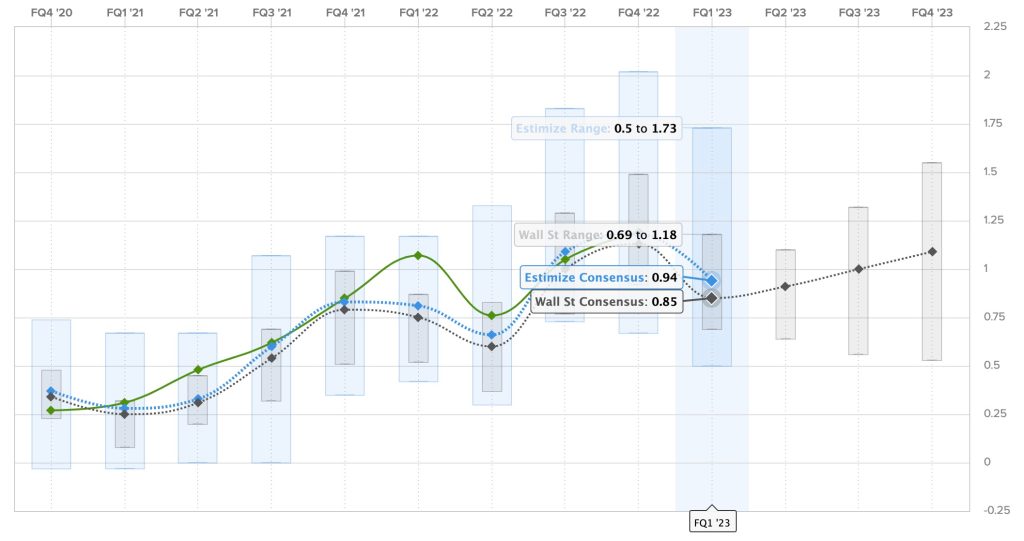

Tesla Q1 2023 earnings

Tesla always attempts to be marginally profitable every quarter as it invests most of its money into growth, and it has been successful in doing so over the last two years now.

For Q1 2023, the Wall Street consensus is a gain of $0.85 per share, while Estimize’s prediction is higher with a profit of $0.94 per share.

The estimates have a wide range this quarter because of the price cuts Tesla implemented during the quarter. Analysts and investors are looking to see how badly it is going to affect Tesla’s margins and, ultimately, its profits.

Unsurprisingly, Tesla achieving the Wall Street consensus would be a big drop in earnings quarter-to-quarter, and the automaker would be flat on earnings year-over-year.

Here are the earnings per share over the last two years, where Estimize predictions are in blue, Wall Street consensus is in gray, and actual results are in green:

Other expectations for the TSLA shareholder’s letter and analyst call

The obvious thing is the gross margin. Investors are going to be looking for that number first. They want to know by how much it dropped and how much room there is since Tesla continued to drop prices after the end of the quarter.

If Tesla can stay in the mid to high teens, I think investors will be happy, but if it dips lower than that, they might have a problem.

Investors will also be looking at insights from management about the pricing strategy, which seems to be changing fast.

Tesla shareholders will also be looking on an update on Cybertruck production as the start of production gets closer, but knowing Tesla management, I wouldn’t expect much more than it being on track for a start of production this summer and volume production next year.

Cybertruck should not have a material impact on Tesla’s revenue in 2023.

I assume that amid margins going down, Tesla investors are going to want to have an update on Tesla’s self-driving program, which has helped margins in the past, but the program has been stalling for a while now.

According to the Say website, where investors can ask and upvote questions for the meeting, shareholders are particularly interested in Tesla Energy this quarter and its potential future impact on Tesla’s financials.

It has been a growing business for Tesla and with a ramp-up in Megapack production, it should be bigger in Q1, but I wouldn’t expect a massive jump in deployment until the second half of the year.

We will see what Tesla has to say about that.

You can join us live on Electrek this evening for intensive coverage of Tesla’s Q1 2023 financial results starting at around 4 p.m. ET for the results and through the evening for news coming out of the conference call and results.

FTC: We use income earning auto affiliate links. More.

Kempower just cut the ribbon on downtown Durham, North Carolina’s first public DC fast-charging station. The new charger is operated in partnership with National Car Charging.

The new station at 111 W. Chapel Hill Street has two plugs (CCS1 and CHAdeMO) and is near restaurants and shops. The Durham area has plenty of Level 2 chargers, but this is its first DC fast charger downtown. Until now, the closest fast charger was three miles away from downtown.

Kempower, a Finnish company with its US office and factory in Durham, doesn’t mention the number of kilowatts its DC fast charger can deliver. However, PlugShare reports that a Ford F-150 Lightning managed 171 kW yesterday.

I asked the City of Durham’s spokesperson why it’s taken this long to install a DC fast charger downtown, and they replied that the “downtown core in Durham is densely developed and there are not many locations for chargers that have the right conditions and available power infrastructure for commercially viable fast chargers.”

Durham Mayor Leonardo Williams said the charger represents another step forward for the city’s clean energy goals: “With this locally built EV fast charger in the heart of downtown, we’re not only reducing our community’s carbon footprint – we’re supporting local jobs, clean energy, and a more connected future for everyone who calls Durham home.”

As of 2025, North Carolina had more than 306 DC fast-charging stations and 1,385 ports.

Electrek’s Take

The City of Durham’s explanation of why it’s taken this long to get a fast charger downtown is a bit of a head-scratcher for me. It must be more of an infrastructure issue, or perhaps a matter of politics or funding, because density hasn’t stopped other cities from installing fast chargers in urban areas. Kempower provided 10 fast chargers at Pier 36 in Lower Manhattan, in collaboration with Revel, in September 2024. At any rate, it’s progress for Durham worth celebrating.

Read more: PowerUp America is adding 100 new fast chargers in the Southeast

If you’re looking to replace your old HVAC equipment, it’s always a good idea to get quotes from a few installers. To make sure you’re finding a trusted, reliable HVAC installer near you that offers competitive pricing on heat pumps, check out EnergySage. EnergySage is a free service that makes it easy for you to get a heat pump. They have pre-vetted heat pump installers competing for your business, ensuring you get high quality solutions. Plus, it’s free to use!

Your personalized heat pump quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here. – *ad

FTC: We use income earning auto affiliate links. More.

Porsche unveiled its new Cayenne EV today, and it comes with an option for something we haven’t seen out of a factory-equipped car before: inductive charging.

Over the years, we’ve heard plenty of attempts by companies to trick consumers into thinking that it’s possible to make an electric car that doesn’t need to charge.

From Toyota’s dumb “self-charging hybrid” claim, to the new fad of “range extenders”/EREVs (aka plug-in hybrids with a bigger battery), to all manner of solar vehicles, people seem to think that convincing customers that they don’t need to plug in will get them to buy an EV (or, will help them greenwash their gas-guzzling hybrids).

And now the next entry into that group has arrived: the Porsche Cayenne electric, which can indeed be driven without ever plugging in, or gassing up, or even parking in the sun.

It does have to be parked somewhere specific though: over a pad in your garage. Because this car can be equipped to use inductive charging, right out of the factory.

Inductive charging uses magnetic fields to transfer electrical power, as opposed to conductive charging, which uses a plug. Inductive charging is how phone charging mats work, but in this case, it’s scaled up significantly in size and power.

We’ve seen a few inductive charging projects before, but they’ve always been aftermarket or experimental so far. Or, they’ve been targeted more at commercial or fleet buyers (buses, for example).

There is one mass-produced EV which is rumored to have inductive charging capability, the Tesla Cybertruck, and we know that Tesla is working on a charging pad, which will be helpful if autonomous vehicles ever roll out properly. But nothing has been announced as available yet.

Porsche, however, is ready to announce that the capability is coming to its upcoming Cayenne EV. Porsche has shown off its inductive tech before, but now we got to see it ourselves when we checked out the Cayenne in a studio preview.

Porsche says that its inductive charging system can push 11kW of power, which is plenty for overnight home charging (on the car’s 113kWh battery). It does this at 90% efficiency – not as much as the ~95% of conductive charging, but still quite good. It also requires an extra ~33lbs of coils and wiring onboard the car, which is a significant if not massive weight gain.

To activate the system, the charging pad makes contact with the car via wide-band wireless communication to determine location, then activates when you park in just the perfect spot. The car’s screen shows guide lines to help you find the way to where you need to be – or there’s always the tennis-ball-on-a-string trick if you want to go low tech.

When we tried it out in LA, once we got the system up and running (hot tip: don’t daisy chain two extension cords if you want your inductive charging pad to work), it quickly charged at 11kW, at least according to the in-car system.

The inductive charger includes a lot of safety features to ensure nothing weird happens. Even though it only uses magnetic fields, the mat includes sensors to detect any living or metal objects nearby, it will stop (yes, this includes your cat that likes to sleep under the car, and yes, Porsche gets asked this question often). We saw this happen once in the studio demo, but it quickly turned back on after deciding everything was okay.

The Cayenne will still have its regular conductive charging ports, capable of 11kW AC or 400kW DC charge. But for those who want to forgo the plug, at least at home, the mat is an available option.

That said – pricing and availability are still TBD. The system costs €7k in Europe, plus an electrician, but we don’t know what it will cost in the US yet.

So, there’s still a chance that someone else beats Porsche to the “first” moniker – possibly Tesla, given that it seems to be close to offering an inductive charging system. But there are a lot of hurdles to ensure that the system is reliable in every type of weather and real world situation, and lots of electrical codes to follow. So, it looks like the race is on.

Electrek’s Take

I was quite interested in talking to the engineers about this system, because I hadn’t actually experienced inductive charging in an EV before.

People have been talking about this for a long time, and I used to be excited about the concept of electrified roads where cars could just drive on them and get a charge and never have to plug in.

However, after conversations over the years and experience with how easy driving and charging an EV is, I came to think that inductive charging is mostly a gimmick, and that we will likely rely on conductive charging in the long term (and especially that in-highway charging is a boondoggle that’s never going to be a good option, especially when catenary/pantograph systems exist).

That said, there are still niches and benefits to be had. In a potential fully autonomous future, we’ll need to figure out autonomous charging, and inductive charging could be a good answer for that.

In addition, some drivers do have difficulty with cables. While the NACS cable is much easier to handle than the old CCS cable, an older driver or one with mobility issues might have a hard time plugging in a car. Inductive charging could be good for them.

Or, heck, maybe someone is just lazy. Or doesn’t like cords. And doesn’t mind spending money for these marginal improvements. We can imagine there are Porsche buyers who could fit that description.

I still think the take rate will be relatively low, but it will be interesting to see real world tests of this, how buyers get along with it, and what sort of problems they manage to solve. As much as I’m a skeptic of inductive charging’s usefulness and acknowledger of its limitations, it’s nice to see new things get tried sometimes.

What do you think about Porsche’s inductive charging system? Would you prefer it to conductive charging? How much would you pay to add this option to your EV? Let us know in the comments.

The 30% federal solar tax credit is ending this year. If you’ve ever considered going solar, now’s the time to act. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

The Inster, Hyundai’s most affordable EV, is Germany’s best-selling small electric car and top overall vehicle priced under €25,000.

The Hyundai Inster is Germany’s best-selling small EV

After launching the Inster in Europe in late 2024, Hyundai’s smallest and most affordable EV quickly became one of the most popular electric cars in the region.

According to JATO Dynamics, the Hyundai Inster was the 19th most popular EV across Europe in June, outselling the Dacia Spring, Hyundai Kona, and Toyota bZ4X.

In Germany, the heart of Europe, Hyundai’s most affordable EV is making an even bigger impression. Since this summer, the Hyundai Inster is Germany’s best-selling small EV so far in 2025 and just won the Golden Steering Wheel award for best car under €25,000 ($28,900) by AUTO BILD & BILD am SONNTAG.

Hyundai said the recognition is proof that its vehicles are resonating with buyers across Europe. The Korean automaker will continue expanding its EV lineup, from the small Inster to the three-row IONIQ 9.

The award comes after the Inster was crowned the 2025 World Electric Vehicle at the World Car Awards ceremony in the spring, held during the New York International Auto Show.

Hyundai’s electric city car starts at just €25,000 ($28,900) in Germany. Despite its small size, the Inster delivers up to 370 km (230 miles) WLTP driving range, fast charging (10% to 80%) in 30 minutes, and a surprisingly spacious and feature-rich interior.

The Inster features dual 10.3″ driver display and infotainment screens with wireless Android Auto and Apple CarPlay as part of Hyundai’s digital cockpit.

By 2027, Hyundai plans to electrify all vehicles sold in Europe. The Inster and IONIQ 9 are now rolling out across the region, and Hyundai plans to build momentum with new EVs, including the IONIQ 3, which will go into production in Hungary in the first half of 2026.

In South Korea, Hyundai’s home market, the Inster is sold as the Casper Electric. The compact EV is sold in Japan, Europe, the Middle East, and parts of Asia.

Although those in the US won’t get to see the Inster or IONIQ 3, Hyundai still has one of the most affordable EVs you can get your hands on. With leases starting at just $189 per month, the Hyundai IONIQ 5 is still America’s best deal for an electric vehicle.

Interested in a test drive? We can help you get started. You can use our link to find available Hyundai IONIQ 5 models near you.

FTC: We use income earning auto affiliate links. More.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024