‘Risky’ for government to intervene as mortgage costs surge, ex-Bank of England deputy warns

It would be “risky” for the government to protect mortgage holders against rising interest rates, according to a former Bank of England deputy governor.

Speaking to Sophy Ridge on Sky News, Sir Charlie Bean said trying to help those paying off home loans could force the bank to raise the base rate even further.

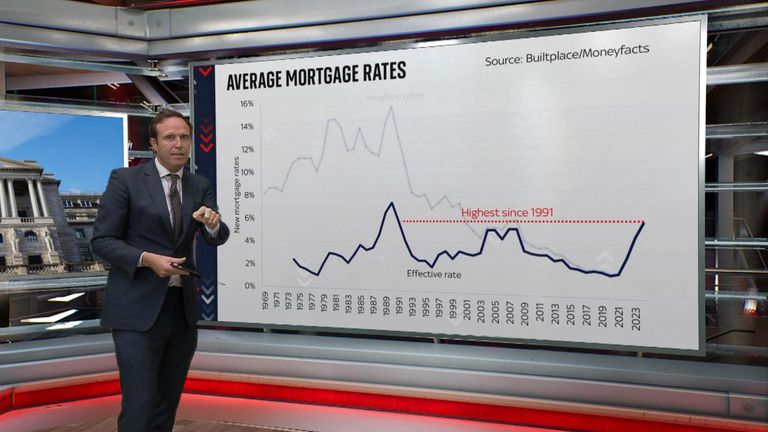

His warning follows a report from the Resolution Foundation think tank that says average annual mortgage repayments are set to rise by £2,900 for those renewing next year.

Total annual mortgage repayments could rise by £15.8bn by 2026, the report added.

Politics live: Cabinet minister reacts to ‘indefensible’ lockdown party video

Sir Charlie said: “There’s not a lot [government] can do to influence the overall macro environment in a favourable way.

“There may be things it wants to do to alleviate pain on particular parts of the population, poor households or whatever.

“There obviously have been some calls for protecting those with mortgages.

“I think that’s risky territory to get into because of course, if you do that and reduce the pressures on those with mortgages, that reduces the extent to which the economy slows and just means the bank has to raise interest rates even more.”

An extended period of inflation led the Bank of England to raise interest rates, pushing up the cost of borrowing.

These increases are now expected to continue until the middle of next year, with the base rate forecast to peak at nearly 6%.

Read more:

Explained: What is causing the mortgage crunch

Ed Conway: Mortgage payers face largest home loan squeeze since early 90s

Sunak insists he won’t pass the buck if he misses key inflation pledge

Homeowners warned of mortgage pain

With an election expected in 2024, interest rates continuing to rise ahead of the vote would cause headaches for Rishi Sunak and campaigners for the Conservative Party.

The uncertainty has led to TSB pulling all its 10-year fixed-rate deals from the market – and Santander withdrew its offers for new borrowers this week.

Michael Gove, the housing secretary, was asked by Sophy Ridge whether he was “frightened” by the situation.

He said he was “concerned of course”, saying the government’s target of getting inflation down would allow the bank to reduce interest rates.

The cabinet minister revealed he does not have a mortgage, but acknowledged the situation is “very difficult for hundreds of thousands of people”.

He added: “As a minister who is responsible for housing, I do take a close interest in what’s happening in the mortgage market.

“It only reinforces the importance of doing everything else that we can to support homeowners and indeed, specifically, to help those in the rental sector as well who have faced the prospect of increasing rents and that’s why we are bringing forward legislation, the Private Rented Sector Reform Bill, in order to help them.”

The bill is aimed at removing no-fault evictions and holding landlords to higher standards, while also allowing homeowners to have an easier time recovering properties from disruptive tenants.

‘No alternative’ to interest rate rise

Criticisms have been made of the Bank of England for not raising interest rates fast enough, allowing inflation to rise.

Sir Charlie admitted that his old employer was “a little behind the curve” in its actions – but added most of the inflationary pressure was coming from external factors like “the war in Ukraine, rising gas prices, global food prices, also supply chain pressures as economies reopened after the pandemic”.

The Bank of England has cut the interest rate for the fifth time in a year to 4% but warned that climbing food prices will cause inflation to jump higher in 2025.

In a tight decision that saw members of the rate-setting committee vote twice to break a deadlock, the Bank cut the rate to the lowest level in more than two-and-a-half years. Households on a variable mortgage of about £140,000 will save about £30 a month.

Andrew Bailey, governor of the Bank of England, said: “We’ve cut interest rates today, but it was a finely balanced decision. Interest rates are still on a downward path, but any future cuts will need to be made gradually and carefully.”

Money latest: What interest rate cut means for savers and borrowers

The Monetary Policy Committee (MPC), the nine-member panel that sets the base interest rate, voted in favour of lowering borrowing costs by 0.25 percentage points.

However, rate-setters failed to reach a unanimous decision, with four members of the committee voting to keep it on hold and another four voting for a 0.25 percentage point cut.

Alan Taylor, an external member of the committee, initially called for a larger 0.5 percentage point cut but after a second vote reduced that to 0.25% to break the deadlock. Had they failed to reach a decision, Mr Bailey, the governor, would have had the decisive vote.

It is the first time the committee has gone to a second vote and highlights the difficulty policymakers face in navigating the current economic climate, in which economic growth is stagnating, with at least one rate-setter fearing a recession, but inflation remains persistent.

Although the central bank voted to cut borrowing costs, it also raised its inflation forecasts on the back of higher food prices.

‘We’ve got to get the balance right on tax’

The bank predicted that the headline rate of inflation would hit 4% in September, up from a previous estimate of 3.75%.

The September inflation rate is used to uprate a range of benefits, including pensions.

The increase was driven by food, where the inflation rate could hit 5.5% this year. About a tenth of household spending is devoted to food shopping, which means it can have an outsized impact on inflation.

The Bank said this risked creating “second round effects”, whereby a sense of higher inflation forces people to push for pay rises, which could push inflation even higher.

Economists at the Bank blamed poor harvests, weather conditions, and changes to packaging regulations but also, in a blow to the chancellor, higher labour costs.

It pointed out that a higher proportion of workers in the food retail sector are paid the national living wage, which Rachel Reeves increased by 6.7% in April.

Economists at the Bank also blamed higher employment taxes announced in the autumn budget. “Furthermore, overall labour costs of supermarkets are likely to have been disproportionately affected by the lower threshold at which employers start paying NICs… these material increases in labour costs are likely to have pushed up food prices.”

There is also evidence that employers’ national insurance increases are causing businesses to curtail hiring, the Bank said. It comes as unemployment in the UK rose unexpectedly to a fresh four-year high of 4.7% in May. Separate data shows the number of employees on payroll has contracted for the fifth month in a row,

The Bank said the unemployment rate could hit 5% next year and warned of “subdued” economic growth, with one member – Alan Taylor – warning of an “increased risk of recession” in the coming years.

Donald Trump has announced 100% tariffs on computer chips and semiconductors made outside the US.

The move threatens to increase the cost of electronics made outside the US, which covers everything from TVs and video game consoles to kitchen appliances and cars.

The announcement came as Apple chief executive Tim Cook said his company would invest an extra $100bn (£74.9bn) in US manufacturing.

Soon, all smartwatch and iPhone glass around the world will be made in Kentucky, according to Mr Cook, speaking from the Oval Office.

“This is a significant step toward the ultimate goal of ensuring that iPhones sold in the United States of America are also made in America,” said Mr Trump.

“Today’s announcement is one of the largest commitments in what has become among the greatest investment booms in our nation’s history.”

Mr Cook also presented the president with a one-of-a-kind trophy made by Apple in the US.

Trump seen through the trophy given to him by Tim Cook. Pic: AP

Trump’s tariffs hit India hard

Mr Trump has previously criticised Mr Cook and Apple after the company attempted to avoid his tariffs by shifting iPhone production from China to India.

The president said he had a “little problem” with Apple and said he’d told Mr Cook: “I don’t want you building in India.”

India itself felt Mr Trump’s wrath on Wednesday, as he issued an executive order hitting the country with an additional 25% tariff for its continued purchasing of Russian oil.

Indian imports into the US will face a 50% tariff from 27 August as a result of the move, as the president seeks to increase the pressure on Russia to end the war in Ukraine.

Mr Trump told reporters at the White House he “could” also hit China with more tariffs.

Read more:

Trump could meet Putin as early as next week

‘Good chance’ Trump will meet Putin soon

Apple’s ‘olive branch’

Apple, meanwhile, plans to hire 20,000 people in the US to support its extra manufacturing in the country, which will total $600bn (around £449bn) worth of investment over four years.

The “vast majority” of those jobs will be focused on a new end-to-end US silicon production line, research and development, software development, and artificial intelligence, according to the company.

Apple’s investment in the US caused the company’s stock price to hike by nearly 6% in Wednesday’s midday trading.

The rise may reflect relief by investors that Mr Cook “is extending an olive branch” to Mr Trump, said Nancy Tengler, chief executive of money manager Laffer Tengler Investments, which owns Apple stock.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike