Q2 2023 earnings preview: What to expect today")

Tesla (TSLA) Q2 2023 earnings preview: What to expect today

Tesla (TSLA) is about to release Q2 2023 financial results today, Wednesday, July 19, after the markets close. As usual, a conference call and Q&A with Tesla’s management are scheduled after the results.

Here we’ll take a look at what both the street and retail investors are expecting for the quarterly results.

Tesla Q2 2023 deliveries

As usual, Tesla already disclosed its Q2 vehicle delivery and production numbers, which drive the vast majority of the company’s revenue.

Earlier this month, Tesla confirmed that it delivered a new record of over 422,000 electric vehicles during the first quarter of the year.

Tesla also confirmed that it was able to produce a new record of nearly 480,000 vehicles during the quarter.

Delivery and production numbers are always slightly adjusted during earning results.

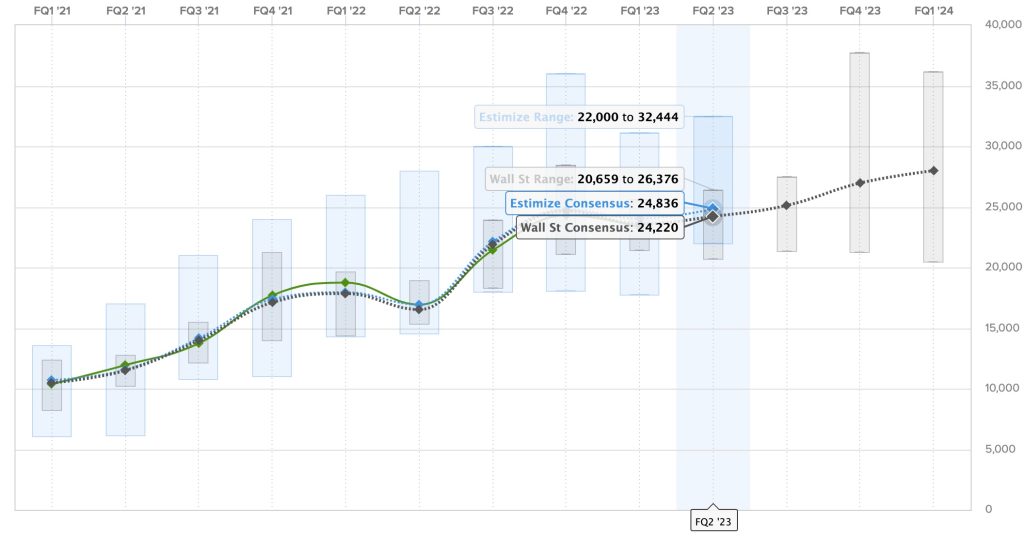

Tesla Q2 2023 revenue

For revenue, analysts generally have a pretty good idea of what to expect, thanks to the delivery numbers.

The Wall Street consensus for this quarter is $24.220 billion, and Estimize, the financial estimate crowdsourcing website, predicts a higher revenue of $24.836 billion.

This would represent a marginal increase over the previous quarter since even though Tesla achieved record deliveries, it had to slash prices to achieve it.

It would be a massive increase in revenue over the same period last year, but that wouldn’t be a great comparison since Tesla had to shut down Giga Shanghai during that time in 2022 temporarily.

Here are the predictions for Tesla’s revenue over the past two years, with Estimize predictions in blue, Wall Street consensus in gray, and actual results are in green:

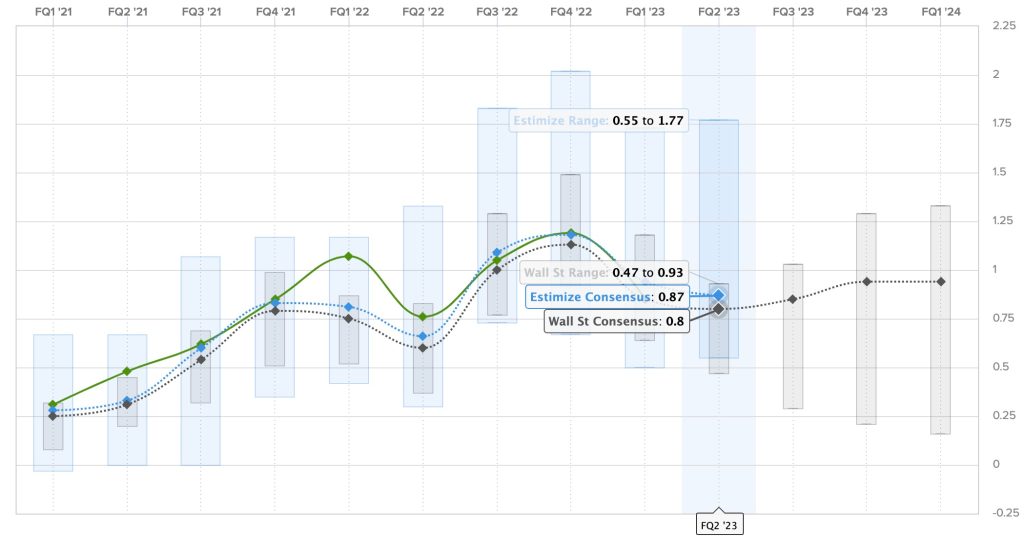

Tesla Q2 2023 earnings

Tesla always attempts to be marginally profitable every quarter as it invests most of its money into growth, and it has been successful in doing so over the last two years now.

For Q2 2023, the Wall Street consensus is a gain of $0.80 per share, while Estimize’s prediction is higher with a profit of $0.87 per share.

Despite anticipating record revenue, Wall Street expects earnings to be down from last quarter because of the previously mentioned price cuts,

Here are the earnings per share over the last two years, where Estimize predictions are in blue, Wall Street consensus is in gray, and actual results are in green:

Other expectations for the TSLA shareholder’s letter and analyst call

Much of the shareholder focus is likely going to be around gross margin and operational profitability at the current price level, which has dropped significantly throughout the year.

With Tesla Energy achieving record quarters that are slowly starting to have a small impact on Tesla’s broader performance, it might be a point of interest again this quarter.

But looking at top-voted shareholders’ questions, it looks like the Tesla shareholder community is more interested in looking into the future.

Here are the top five questions that Tesla is likely going to answer during the conference call:

- Has any automaker approached Tesla to license FSD?

- When will you get more information about our Cybertruck orders? Estimated delivery schedules, pricing, and specifications?

- Have you considered allowing FSD transferability as a lever to allow existing customers to upgrade to a new Tesla instead of being locked in to existing cars due to price of FSD?

- What is the status of the 4680 Cell? How far are you from the specs you laid out on battery day? When do you expect to achieve what you laid out on Battery Day?

- As you open the supercharger network in North America to other EVs, do you plan to accelerate anticipatory investments in supercharger expansion to avoid congestion, and how will you deal with long lead times to upgrade electric T&D services to these areas for multi-megawatt loads?

You can join us live on Electrek this evening for intensive coverage of Tesla’s Q2 2023 financial results starting at around 4 p.m. ET for the results and through the evening for news coming out of the conference call and results.

FTC: We use income earning auto affiliate links. More.

Iconic British brand Moke International is officially landing in California, bringing a splash of retro style and electric fun to the West Coast with the launch of its California Collection. The medium-speed, open-air electric vehicles – reminiscent of classic beach buggies – are now street-legal in the state, with reservation deposits now open.

It’s a move that’s been years in the making, and we’re finally ready to see these fun-looking rides roll out on US streets thanks to a retail partnership with Shaver Automotive.

The California Collection marks the first time MOKE’s EVs are being sold in the US as fully compliant, street-legal vehicles, following a multi-year process to obtain certification under California’s tough emissions and safety regulations. The vehicles have now gone beyond the 25 MPH limitations of Low Speed Vehicles, doubling that figure to offer rides at up to 50 MPH (80 km/h).

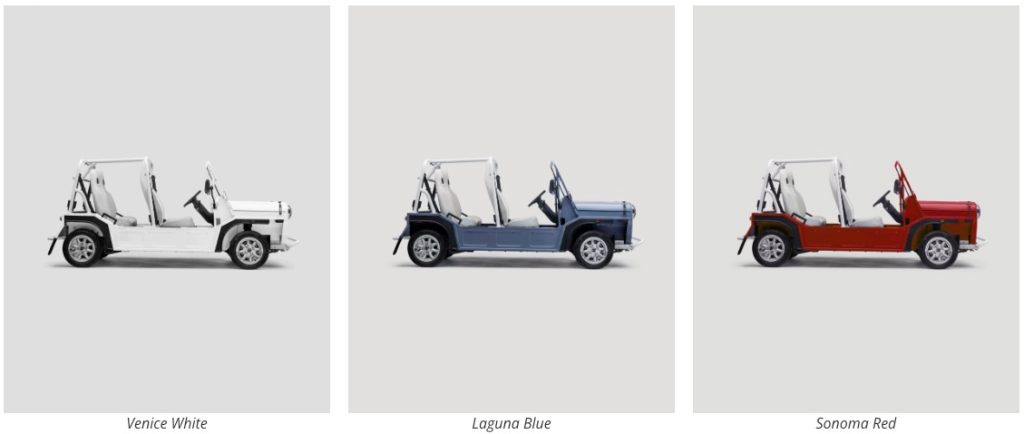

The collection also includes three new colorways inspired by the nostalgic hues of the Golden State: ‘Sonoma Red’, ‘Laguna Blue’ and ‘Venice White.’

As the company explained, “This foray into the state follows MOKE’s groundbreaking achievement as the first low-volume EV manufacturer to secure California Air Resources Board (CARB) approval. With unmatched quality, all genuine MOKEs are handcrafted in the UK, with over 70% of parts sourced from Europe. A limited quantity of 325 MOKEs will be available to purchase throughout the US in 2026.”

Originally based on a British military vehicle from the 1960s, the Moke evolved into a cult-favorite beach car beloved in tropical destinations from the Caribbean to the French Riviera.

Now, it’s gone all-electric, with a 54-mile (87 km) range and a top speed of 50 mph (80 km/h) from a 33 kW motor that prioritizes fun over freeway.

“Launching in California feels like a true homecoming for us at MOKE,” said Lorne Vary, CEO of MOKE International. “California’s love of sunshine, freedom, and outdoor adventure reflects everything our brand stands for. Partnering with Shaver Automotive means we can finally share that feeling with Californians who have been waiting for their MOKE moment.”

The Electric MOKE is available for order now in California, via Shaver Automotive, with prices starting from $49,500. That puts it well into premium territory, meaning it likely won’t replace the family car, but could be a fun plaything to park at your beach house… for those who own a beach house.

While the MOKE won’t be replacing your daily commuter or long-range EV, it could be the perfect picturesque ride along a coastal road, in a resort rental fleet, or for anyone who values open-air, zero-emission fun over raw performance.

Electrek’s Take

We’ve seen a number of street-legal Low Speed Vehicles (LSVs) make their way into beach towns and gated communities in recent years, but few bring the retro flair and lifestyle appeal of the MOKE. And by going the low-volume manufacturer route, they get to offer speeds of twice that allowed by LSVs without needing to meet as many of the complicated Federal Motor Vehicle Safety Standards (for better or for worse).

At nearly $50k, it’s a luxury toy, sure. But for the right buyer, it looks like an awesome time on four wheels. California might just be the perfect place for this beach cruiser comeback.

Oh, and I’d be remiss if I didn’t share the image below of Electrek’s founder Seth Weintraub from his youth when he used to ride old school Mokes around Macau, and with a left-hand manual 4-speed gearbox, no less!

FTC: We use income earning auto affiliate links. More.

bp pulse is continuing to roll out public DC fast charging across the US, and the company has opened its first-ever site in Arizona, along with new fast-charging locations in Texas, Florida, and Ohio.

In Arizona, bp pulse’s first site is now online at the Petro Travel Center in Eloy, just off Interstate 10 at Exit 200 (pictured). The location features 16 charging bays delivering up to 400 kilowatts, with both CCS and NACS connectors available. While charging, drivers can take advantage of the travel center’s onsite diner, convenience store, ATM, barber shop, and restrooms.

In South Florida, bp pulse’s new fast-charging site is at 2400 Miami Road in Fort Lauderdale, about three miles from Fort Lauderdale–Hollywood International Airport. The site features 16 charging bays, offering a mix of 150 kW and 400 kW speeds, with both CCS and NACS connectors. Its proximity to the airport makes it a handy stop for ride-hail drivers, EV rental returns, and airport pickups and drop-offs, with hotels, restaurants, and convenience stores nearby.

Texas is also getting more high-power charging, with a new bp pulse site at the Petro Travel Center in El Paso, located off Interstate 10 at Exit 37. This location offers 12 charging bays capable of delivering up to 400 kW, again with both CCS and NACS connectors. Drivers can take advantage of the diner, convenience store, barber shop, and restrooms while they charge.

In Ohio, bp pulse has opened a smaller but still high-powered site at a TravelCenters of America location in Hebron, just off Interstate 70 at Exit 126. The site includes six 400 kW charging bays with CCS and NACS connectors, along with access to a convenience store, fast-food options, and restrooms.

These openings are part of bp pulse’s broader plan to build out EV charging across bp’s retail footprint, including bp, Amoco, ampm, Thorntons, and TravelCenters of America locations. Many of those sites are designed to combine fast charging with food, restrooms, and other travel amenities. bp has also said it plans to begin adding EV chargers at Waffle House locations starting in 2026.

Read more: bp pulse opens a huge airport EV fast charging hub in Houston

If you’re looking to replace your old HVAC equipment, it’s always a good idea to get quotes from a few installers. To make sure you’re finding a trusted, reliable HVAC installer near you that offers competitive pricing on heat pumps, check out EnergySage. EnergySage is a free service that makes it easy for you to get a heat pump. They have pre-vetted heat pump installers competing for your business, ensuring you get high quality solutions. Plus, it’s free to use!

Your personalized heat pump quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here. – *ad

FTC: We use income earning auto affiliate links. More.

The Cadillac Lyriq and Chevy Blazer EV were among the vehicles that saw the biggest lease price drops in December.

Cadillac and Chevy EV lease prices drop in December

With the $7,500 federal EV tax credit now gone, automakers are filling the gap with their own incentives. Some are passing on the savings as bonus cash, conquest cash, lease discounts, and more.

Two General Motors electric SUVs, the Chevy Blazer EV and the Cadillac Lyriq, had some of the largest lease price drops of any vehicle in December.

The 2026 Cadillac Lyriq AWD Luxury model is now listed at $439 per month for 24 months. With $4,979 due at signing, the effective rate is $646, or $28 less per month than in November.

That’s after the Lyriq already saw prices drop by $115 a month from October. However, the December deal includes a $2,000 competitive bonus for owners and lessees of a 2011 model year or newer non-GM vehicle.

The 2026 Chevy Blazer EV FWD LT is now available to lease for as low as $319 a month for 24 months. With $6,039 due at signing, the effective rate is $571 per month, about $60 less than in November. The deal includes a $750 competitive bonus and $1,000 customer cash allowance.

Chevy and Cadillac are offering discounts across their entire EV lineup. All 2025 Chevy electric vehicles, including the Blazer EV, Equinox EV, and Silverado EV, are available with 0% APR financing for 60 months.

Intestingly, the 2026 Chevy Equinox EV is also available with 0% APR financing, while the 2026 Blazer EV is listed with 1.9% APR for 36 months.

Cadillac is offering a $2,000 conquest or loyalty bonus for the 2026 Cadillac Vistiq and select 2025/2026 Optiq and Lyriq models, plus 2.9% APR for 60 months.

The 2026 Cadillac Optiq is available to lease for as low as $319 per month for 24 months, while the 2026 Vistiq is available to lease for $619 per month for 24 months.

Want to try one out? We’ve got you covered. Check out the links below to see what Cadillac and Chevy EVs are nearby.

FTC: We use income earning auto affiliate links. More.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024